Cameco suspends uranium production at Inkai JV in Kazakhstan over bureaucratic holdup

The in-situ recovery JV with Kazatomprom didn’t get an extension to submit its project paperwork.

[Editor’s note: adapted from Hallgarten & Co.’s note on Western Uranium]

In what was a bad four years for the mining space, special punishment was reserved for the uranium sub-space where every time it tried to stagger to its feet it was dealt a new, low-blow that sent it reeling. Even as mining markets have picked up in 2016, uranium has been, relatively, left behind as the spot price wallows and that acts as an anchor holding the sub-space from moving forward. Only the Rare Earth space gets to share in this “cruel and unusual” punishment.

However, the persistence of those that believe in the long term attractiveness of nuclear power has kept the space afloat and allowed even a few hardy near-producers or those holding past-producing properties, like Western Uranium, to soldier on through the tough times.

Hard core Uranium bulls know how Moses felt when he was doomed to wander forty years in the desert and never get to see the Promised Land. The great hope had been that the Japanese reopening would help matters and yet it hasn’t (at least not yet). The second hope (quite a vain one) was that the Germans would see the light on their unilateral closure actions (and they have not). The one consolation being that everyone else in Europe regards the Germans as crazy for taking the action they did while still mouthing platitudes to low carbon emissions and ramping up coal-fired power at the same time!

To the dismay of many that see nuclear as a “green” solution to rising global energy demand, some have pitched nuclear as competing against wind and solar, with Germany being a particularly egregious example of “kooky” thinking on this front. Ironically though the German decision has prompted the country to buy nuclear-sourced electricity from France, the paragon of nuclear users with around 80% generated from this source.

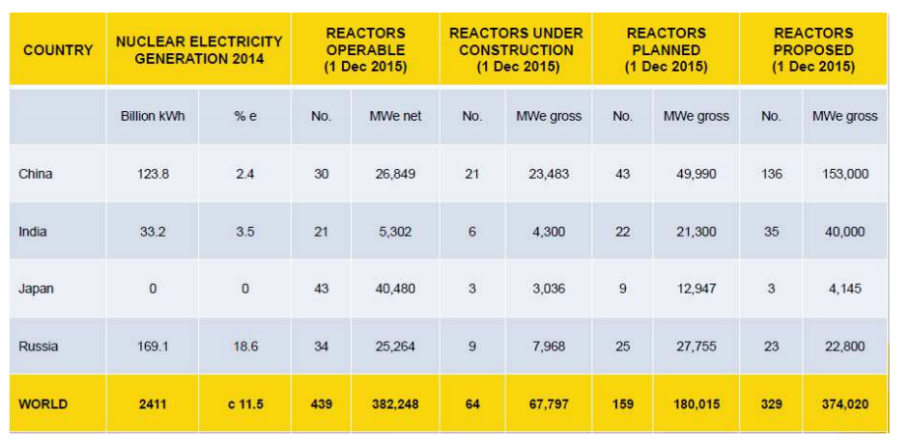

This chart shows the countries with the strongest potential capacity additions in nuclear generation.

Source: Western Uranium

Probably all one needs to know is encompassed in the preceding table, which says more than any number of price charts. There is massive future demand baked into construction schedules that, with the amounts of money expended, will not be derailed. The advocates of nuclear are looking past the mere showmanship of the German chancellor and the temporary shutdown of the Japanese generating capacity towards an uplands where this rising fleet of nuclear plants in emerging economies will be creating the added demand for yellowcake, rather than static or declining markets like those of Germany.

Current production (and even planned production) is not even vaguely able to meet this demand as the graph below demonstrates.

In the wake of this process we see the survivors divided into the following groups:

Normally we would put advanced exploration with near producers but the problem is that many of this category are merely wanting to be sold rather than getting into production. There will be a moment for them, a “day in the sun”, but it is not now. There are quite a number of those companies out there with sizeable reserves proved up but no real plan to move forward. When the turn in the U price comes they will be hoping to be bought by one of the producers, but there are more advanced explorers than producers so inevitably some attendees at the ball will be without partners for the dance.

Junior “juniors”, the moose pasture merchants, are basically not needed or wanted for probably the rest of this decade. If there is no resource, or a puny one, then it’s a case of “don’t call us, we’ll call you”.

The ideal place to be positioned now is in either producers or the near/former producers. Producers will obviously be first movers, but near- and ex-producers should swiftly follow with the added advantage that they do not come freighted with long term contracts at low prices. That said, companies needing funds to go the final mile to production may be tempted to commit to contracts at revived, though still low, prices with offtakers/traders to grab that all-important final funding to make it across the production line.

Creative Commons image by Marcin Wichary