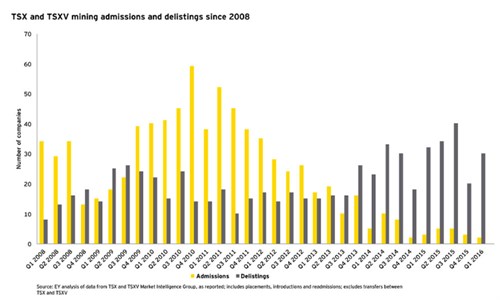

The answers for both are intertwined. For every new company entering the public markets, 15 are leaving. The last few years have helped to wash away the junior exploration companies, many of which shouldn’t have been publicly traded in the first place. Ernst and Young mapped the delistings and new admissions since 2008.

Intuitively, companies will come to market when capital is available. During the last bull cycle, particularly in 2010 and 2011, more than 40 new companies were admitted to the TSX or TSX-V per quarter. Interestingly, delisting stayed relatively high during this period as well, attributable in some degree to takeovers. Starting in the third quarter of 2013, the ratio reversed, and for the last three years far more companies have delisted than have been admitted. In the first quarter of 2016, only two companies were admitted (Nickel One Resources and Candelaria)—while approximately 30 delisted. As long as capital remains scarce and cautious, this trend does not appear set to reverse any time soon.

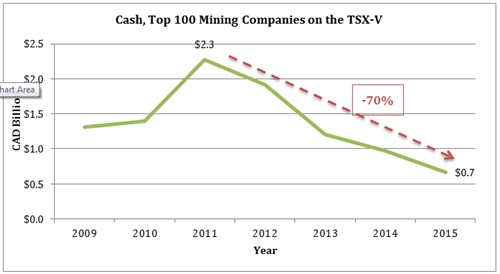

There is correlation between the available capital in the space and delistings. PriceWaterhouseCoopers (PwC) observed the top 100 mining companies on the TSX-V since 2009, (note, this excludes the TSX-listed companies, which are featured in the charts above). According to PwC, “The top 100 junior miners on the TSX-V raised CAD$515 million in equity financing in 2015, 25% less than last year, and almost all of it (86%) was raised by just 15 companies.”

The result has been a collapse in cash held by the top 100 junior mining companies. From the peak in 2011 with $2.3 billion in aggregate cash, these companies collective balance sheet contain a total of just $700 million in cash at the end of 2015. Additionally, values have fallen five-fold; the combined market capitalization of the top 100 companies now adds up to a mere $4.8 billion, down from $20.6 billion in 2011.

For reference, two Sprott Physical Gold Trusts (PHYS), with a current market capitalization of $2.4 billion, would be worth more than the top 100 miners on the TSX-V combined.

So, to answer our original two questions: Despite the record-breaking pace we saw in the first half of 2016, in terms of financings, we remain very near the bottom in the juniors market. This same cohort is still clamoring for capital, placing equity and debt providers in an enviable position. Capital providers like Sprott are currently able to exercise considerable power and extract strong terms. With regard to new companies, even after the gangbuster year for the TSX, more companies go extinct each quarter, which is a painful but healthy rebalancing. Sprott remains committed to bringing you only the best of them.

And keep those questions coming!

This information is for information purposes only and is not intended to be an offer or solicitation for the sale of any financial product or service or a recommendation or determination by Sprott Global Resource Investments Ltd. that any investment strategy is suitable for a specific investor. Investors should seek financial advice regarding the suitability of any investment strategy based on the objectives of the investor, financial situation, investment horizon, and their particular needs. This information is not intended to provide financial, tax, legal, accounting or other professional advice since such advice always requires consideration of individual circumstances. The products discussed herein are not insured by the FDIC or any other governmental agency, are subject to risks, including a possible loss of the principal amount invested.

Generally, natural resources investments are more volatile on a daily basis and have higher headline risk than other sectors as they tend to be more sensitive to economic data, political and regulatory events as well as underlying commodity prices. Natural resource investments are influenced by the price of underlying commodities like oil, gas, metals, coal, etc.; several of which trade on various exchanges and have price fluctuations based on short-term dynamics partly driven by demand/supply and nowadays also by investment flows. Natural resource investments tend to react more sensitively to global events and economic data than other sectors, whether it is a natural disaster like an earthquake, political upheaval in the Middle East or release of employment data in the U.S. Low priced securities can be very risky and may result in the loss of part or all of your investment. Because of significant volatility, large dealer spreads and very limited market liquidity, typically you will not be able to sell a low priced security immediately back to the dealer at the same price it sold the stock to you. In some cases, the stock may fall quickly in value. Investing in foreign markets may entail greater risks than those normally associated with domestic markets, such as political, currency, economic and market risks. You should carefully consider whether trading in low priced and international securities is suitable for you in light of your circumstances and financial resources. Past performance is no guarantee of future returns. Sprott Global, entities that it controls, family, friends, employees, associates, and others may hold positions in the securities it recommends to clients, and may sell the same at any time.