Mining’s old guard needs strong medicine

A new report details subpar investor returns in the mining industry over the last decade, particularly big cap diversified companies which have not adapted to new realities.

I started last week by flying across the country to visit Integra Gold’s Lamaque project, and so this week’s Maven Letter snippet is the report I wrote after that experience. I hope you enjoy the writeup even a shred as much as I enjoyed the trip!

Site Visit: Integra Gold’s Lamaque Project

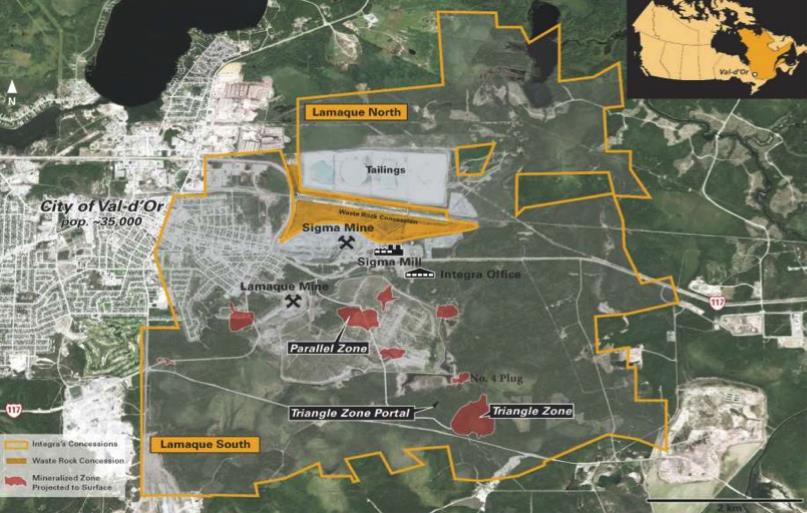

I spent Tuesday at Integra Gold’s Lamaque project, which is right beside the city of Val d’Or, Quebec. For those unfamiliar with french, Val d’Or translates as Valley of Gold. And it’s an appropriate name: the city grew up around two gold mines and mining remains the only significant game in town.

That doesn’t mean every attempt to mine gold near Val d’Or has worked out. Looking just at the Lamaque property: two mines were highly successful, producing a joint 9 million ounces of gold over 60 years, while two subsequent attempts ended in bankruptcy.

Now Integra is taking a turn. I bought into ICG in December because the story at that point made good sense:

That was the story then. Before I get into how it has changed, it’s time for a bit of backstory.

The Lamaque project covers the historic Sigma and Lamaque mines. Both started operations in the 1930s and ran for over 50 years. Sigma reached a depth of 1.8km while Lamaque went 1.1 km down.

The mines were only 500 metres apart but the deposits had their differences. Both were focused on intrusive plugs pushed up through mafic country rock. At Sigma the plug was cut with a series of steeply dipping shears that carried most of the gold and that penetrated into the mafics, carrying mineralization outside of the plug. At Lamaque such shears are still present, but they do not carry the gold. Instead, Lamaque’s gold is hosted in thin tension veins that clustered with enough density to give grade to the bulk of the rock.

(These two deposits, sitting 500 metres apart and showing those geologic differences, are strikingly similar to the two main deposits now under study at Lamaque: Triangle is like Sigma and No. 4 Plug is like Lamaque.)

Sigma and Lamaque closed down in the mid-1980s because of a weak gold price and labour struggles (striking miners) that were exacerbated by an anti-mining provincial government.

Such successful mines, shut for labour and gold price reasons – it’s no surprise the potential for more mineralization has since drawn others to the area. First came McWatters, which put an open pit on top of the Sigma mine between 1997 and 2001. The effort failed – open pit mining meant too much dilution – but the process left behind a nicely refurbished mill.

After that Century Mining tried. It re-opened the Sigma underground mine in 2002, but did so before having figured out where and how to access enough ore. The mill was hungry and Century couldn’t mine fast enough. Enter bankruptcy number two, in 2012.

In 2003 Integra arrived on scene. The company started with just Lamaque South, which did not include the old mines or the mill but offered good exploration potential. And so that’s what Integra did: explore. Over the next ten years the company discovered Triangle, now the focus of the mine plan, and five other gold zones.

By this time, the mining bear market was in full effect and exploration capital was hard to come by. Integra knew it was onto something with Triangle and managed to raise enough funds to keep slowly advancing its discovery despite the terrible market.

But that terrible market also created opportunity. In 2014 Integra was able to strike a deal that changed everything: it bought the neighbouring Lamaque property, home to the mill, the old Sigma and Lamaque mines, and a host more targets.

Integra inked a heck of a deal: it bought the property for $1.8 million in cash and $5.75 million worth of ICG shares. It then turned around and sold the old waste rock pile to a local aggregate company for $1 million.

The mill changed Integra completely. Before, the company had a 570,000-ounce deposit, which would have had to grow dramatically before being of economic interest. Now it had a mill, with a replacement value of over $100 million and almost all of the permits to operate, located less than 3km from its deposit, as well as two historic mines with unknown remaining potential and six decades of historic mining and exploration data.

Parts of the regrind circuit at the Sigma mill.

Suddenly Integra’s asset started to look economic.

Through 2015, while the bear mining market continued to not care, Integra marched ahead. It grew the resource count beyond 1 million ounces, hired a team of metallurgists and engineers who used to work at Sigma and Lamaque to assess the mill and plan for a restart, digitized the huge historic database, and put together a PEA for a mine at Lamaque.

The study was robust. It estimated an investment of just $62 million to turn Lamaque into a mine producing 105,000 oz. gold annually and generating a 77% IRR. It helps that by early 2015 Integra had outlined a very nice resource: 1.5 million indicated tonnes grading 10.2 g/t gold and 488,500 inferred tonnes averaging 15.1 g/t gold. High grades for sure.

Core from Triangle, showing some of the deposit’s high grades.

All the while, drilling at Triangle continued. In March of this year, the exploration work produced its most significant result yet: a new Triangle estimate that was larger but more importantly that remodeled the deposit.

In the old model most of the gold sat in thin veins that were nearly flat. To mine those ounces would have required bulk mining methods, where you take all the little veins and the surrounding unmineralized rock. It would have worked, but bulk methods are prone to dilution struggles and to mine flat-lying veins is costly because you get no help from gravity.

As Integra punched hole after hole into Triangle, however, a new model emerged wherein most of the gold actually sits in thick structures that dip steeply. That is way better – it means mining can primarily be done using long-hole stoping, a more efficient method less prone to dilution challenges. And since the structures dip steeply, gravity helps rather than hindering.

We are yet to see exactly how this new resource model will impact the financial model for Triangle. For that we have to wait until Integra updates its preliminary economic assessment.

That updated PEA – due out before the end of the year – is Integra’s main focus right now. The new study will do a few key things.

A hand-drawn section of the No. 4 Plug. The green blobs are where the veins cluster

The reason points 2 and 3 matter is this: Triangle is a very good deposit, but it would be very difficult to produce more than perhaps 120,000 oz. annually from that deposit alone. It is just hard to develop enough working faces and move enough trucks along a single ramp to pull more ore than 1,500 to 2,000 tpd from a single underground operation.

It would still be a good mine. But Integra wants to be more than good. As president and CEO Stephen de Jong said in his presentation yesterday, “We are trying to turn this into the unicorn of the industry – that near impossible asset that is inexpensive to build, very economic to operate, and can produce 200,000 to 250,000 oz. a year in Canada, with permits beside the mining city of Val d’Or.”

De Jong includes the point about size in order to say (without saying) that Integra wants to make Lamaque matter to a major. A 100,000-oz.-per-year Lamaque might be of interest to a small or mid-tier miner but a major is not going to bite unless Integra shows that Lamaque has the potential to produce twice that much annually. Incorporating an updated No. 4 Plug and another area, called the No. 6 Vein, into the new PEA is a start. But more is needed. Specifically, Integra needs to outline another deposit or two that could also feed the mill.

The mill can handle it. The old PEA assumed 1,300-tpd throughput. The updated study might use a large number, but not dramatically. The mill could churn through that as is – its current capacity is 2,500 tpd.

But the facility has churned through as much as 5,000 tpd and could do so again if one component – a 25-foot SAG mill that Century Mining sold in its efforts to stave off bankruptcy – were replaced. In other words, for something like $10 million Integra could double the mill’s throughput.

That’s a big mill. If the company can outline a series of deposits that could each feed ore to the mill, Lamaque could be a major gold mine. And a major gold mine is what a major miner wants to buy.

To that end, Integra has shifted its drilling focus of late. Last year all eyes were focused on Triangle, as the team worked to understand that geology. Now there is a team at Triangle, working to drive an exploration decline into the zone (more on that in a moment). Meanwhile, the exploration team is testing other targets.

There’s Sigma Extension, which is a discreet magnetic target just east of Sigma. It has long been known that mag anomalies are worth exploring around Lamaque because mineralization always comes in tonalite or diorite intrusives, which are magnetic. Sigma Extension was never tested in the past, though, because the old property boundary ran right across the target.

There’s Southwest, another discreet magnetic target near the old Lamaque mine.

There’s Donald, which is right beside Triangle.

And there’s Lamaque Deeps. Remember: the Sigma mine went to 1.8 km depth while Lamaque only reached 1.1 km. And mining ended in mineralization. That begs the question: what remains beneath Lamaque?

McWatters, the company that mined the Sigma open pit, punched several holes into Lamaque Deeps, coming over laterally from the Sigma mine. Those holes returned intercepts ranging from 20 to 90 metres grading 2 to 4 g/t gold.

I realize that doesn’t sound exciting compared to the grades at Triangle, but Lamaque was a different beast. The best years at Lamaque were when the mine reached big zones of rock littered with tension veins that could be bulk mined – and the average grade in those good years was 3 g/t gold.

Now Integra is drilling deep to test McWatter’s results and figure out just what’s down there. It collared a Lamaque Deeps pilot hole yesterday, while we were on site. The pilot hole will be over 1,000 metres long and will take about three months to complete. Then Integra will complete a series of wedge holes off this pilot hole, to get numerous results from one deep effort.

Success would start with hitting the kind of wide zones of clustered veining that McWatters hit in its holes in the 1990s. If there is enough volume of mineralized rock, that alone would make Lamaque Deeps worth mining. There is potential for more. In particular: the No. 6 Vein dips towards Lamaque and could intersect the intrusive plug at depth, which might create a blowout gold zone.

The other big effort underway at Lamaque is driving the exploration ramp into the Triangle deposit. It’s called an exploration drive, but really it’s the mining ramp – it’s just labeled ‘exploration’ until permitting catches up.

Maven at the Triangle ramp portal. The ramp is currently 50 metres long.

The drive will be 2.5 km long. It’s sized for production – 5.1 m wide and 5 metres high – and will take 15 months to complete. Once complete, Integra will use the ramp to take a bulk sample of Triangle ore, which is essential to confirm that the resource model is accurate before using the model as a guide to mining.

Integra will also use the drive to drill Triangle from underground. In the last year drilling at Triangle has tested the deposit at depth, but the real focus has been on delineating the top 200 metres with high accuracy in preparation for mining. It also just made sense – those were shorter, cheaper holes to drill compared to deep holes. With the decline in place, Integra will be able to test the deposit at depth more efficiently.

Driving the ramp shows two things:

Summing up…

Integra recently updated the cover photo on its investor presentation:

This is the new plan: define a series of deposits that could be mined simultaneously to send 4,000 tonnes of ore a day or more to the Sigma mill, making Lamaque a major gold mine. Integra doesn’t have to develop all the deposits; all it needs to do is prove the path for how Lamaque can reach 200,000 oz. of annual production.

Combine that with the location – in Canada and beside a mining-based community full of experienced labour – and Lamaque’s other attributes – permitted, high grade, the Canadian forex advantage, low capital cost, high rate of return – and I think a major will buy Integra within 12 months.

I went to Lamaque to get a feel for a project that I already believed in on paper. I came away with a changed understanding of what the company is working to achieve with its updated PEA – and the new version is a big improvement.

The fact is, Integra is a takeout target. There are very few gold projects in the world that could be put into production this cycle. Lamaque could. Midtier miners looking to expand their portfolios in the near term are undoubtedly eyeing the company up.

But Integra’s aim is to maximize value for shareholders and the way to do that is to catch the attention of as many suitors as possible.

The bigger the asset the bigger the bid, so Integra is trying to build the size of its asset – in terms of resource ounces and potential annual production ounces – as quickly as possible, specifically before someone makes an offer. The new plan for the PEA, including No. 4 Plug, the No. 6 Vein, and the possibility of a shaft at Triangle to show how the project could scale up, makes a lot of sense.

The knock against Integra is its share count. I hear it all the time and I understand. Yes, I would prefer if the company had 100 million shares out instead of 475 million. Why? Because whether Integra is bought or puts Lamaque into production itself, this is a single asset company. Its value stems from that one asset and its share price is that value divided by the number of shares. In the case of a bid, the value is a tangible per-share amount; in the case of Integra evolving into a miner, the share price is limited to the asset value divided by the number of shares.

However, the count is what it is. It’s a result of advancing a project despite a bear market. And it hasn’t prevented ICG from enjoying a sustained share price climb.

Integra has enough money in the bank to fund its activities to the end of 2017, including finishing the underground ramp, and still have $5 million in the bank. This team would not let its bank account get that low, but the odds of ICG still existing in 16 months are slim. I do not expect the company to raise any more funds for a year. In other words, the count will likely be 475 million, its current level, when someone takes the company out.

After seeing the asset firsthand and getting up to speed on what Integra wants to accomplish in the next 12 months and why, I plan to stick around until that bid appears.