Haul truck at De Beers’ Jwaneng mine in Botswana, the most valuable diamond mine in the world. Source: De Beers Group.

De Beers

Industry leader De Beers, representing >30% of global marketshare, strategically reduced production at multiple mines in 2015 and completely suspended production at others, cutting total production by approximately 7% in 2015 to 29M carats.

Tailings operations offer the greatest operating flexibility, and De Beers strategically reduced tailings production at Orapa in Botswana last year before subsequently reducing production at Venetia in South Africa, off-shore operations in Namibia, and putting Snap Lake in Canada and Damtshaa in Botswana on care and maintenance, in an effort to balance global diamond supply/demand.

De Beers also sold its South African Kimberly tailings mine and related operations in December for $7.2M to a joint venture between Ekapa mining (private) and Petra diamonds.

De Beers is targeting 26-28M carats in 2016, compared to 29M in 2015, and 33M in 2014, -6.9% and -18.2%, respectively.

Underground at ALROSA’s International mine, Russia. Source: ALROSA.

ALROSA/LUKoil

While De Beers cut production, ALROSA (RTS: ALRS), which has a similar marketshare, actually increased production in 2015 to 38M carats, +6% YoY. Instead of reducing production, ALROSA instead held back supply by only selling 78% of 2015 production.

Incremental production from ALROSA primarily came from new mine Botuobinskaya and ramping-up sophomore mine Karpinskogo-1 to full-production.

In addition, production at the company’s largest mine, Jubilee, which represents ~25% of the company’s output, increased 3.1% as higher grade was achieved at the ore body’s central lobe. Production decreased at the company’s second largest mine Nyurbinskaya as the mine’s processing plant was shared with ore from the Botuobinskaya mine and the Nyurbinskaya placer operations.

ALROSA has indicated that they do not plan to reduce production unless market conditions get substantially worse. The company is targeting production growth going forward, with average production of ~40M carats annually over the next 10 years.

Also in Russia, LUKoil (RTS: LKOH) sold 2.3M carats in 2015 from its Grib mine, which commenced production in June 2014. With a reserve of 75M carats and full production ramping up to 4.5M carats annually, starting in 2016, the life of mine is 15-17 years.

It seemed likely that the Grib mine would have been sold by now, as the “oil major” indicated interest in selling the non-core asset during development, however, the company has since indicated that the most likely suitor, ALROSA, has not been willing to pay what they perceive as fair value for the mine.

Rough diamonds from LUKoil’s Grib Mine, Russia. Source: Grib Diamonds.

Rio Tinto

Rio’s Argyle mine in Australia, the world’s largest diamond mine by production volume, realized a >45% YoY production increase in 2015 after completion of a multi-year underground mine development project. This was despite strategically halting processing in December in an effort to “manage inventory levels” amidst a softer global diamond market. Argyle produced 13.5M carats in 2015 versus 9.2M carats in 2014.

In June 2015, Rio sold its 78% stake in the Murowa mine in Zimbabwe to partner RioZim (private), which now owns 100% of the mine. A new diamond mining tax structure in Zimbabwe and concerns of forced government consolidation of the country’s diamond miners most likely influenced the company’s decision to leave the country.

Rio now only holds two operating diamond mines, 100% of Argyle and 60% of Diavik in Canada. The company is targeting 21M carats in 2016.

Lockhart Lake ice road, Diavik mine, North West Territories, Canada. Source: Rio Tinto.

Dominion Diamond

Dominion Diamond is Rio’s 40/60 partner in the Diavik mine which has 4 pipes, 3 of which are in operation. The 4th pipe, A-21, has 10M carat reserve and is being developed for $400M, with first production slated for late 2018. In 2015, Diavik produced 6.4M carats, which was down 11.5% YoY due to processing plant pauses in the fourth quarter and the absence of stockpiled ore relative to 2014.

Dominion’s second asset, its ~89% owned Ekati mine, produced an estimated 3.0 million carats in 2015, a 6.3% decrease over 2014, as the company transitioned the mine plan to focus on the Misery Main pipe. Misery Main is a 14M carat reserve with first production expected in 1H 2016, estimated to contribute 4M carats this year, which would substantially increase the mine’s production by 70% to an estimated 5.1M carats in 2016.

Looking further ahead, Ekati’s Jay pipe, which is an 85M carat reserve, currently in feasibility study stage, would come online in 2020. The Pigeon pipe, a 3M carat reserve (10M carat resource) which began production in 2015, would fill the mine’s production gap between Misery Main and Jay in 2018 and 2019.

The Cullinan mine in South Africa. Source: Petra Diamonds.

Petra Diamonds

In calendar 2015, Petra produced 3.2M carats, a 5.3% increase YoY. The Finsch mine which currently represents >60% of Petra’s production by volume, and >40% by value, realized improved production efficiency and higher grades in 2015.

Petra plans to ramp-up company-wide production to 5 million carats by FY 2019 (which ends calendar 2H 2018), led by the Cullinan plant expansion project, which will overtake Finsch as the company’s primary producing asset over the next 3 years, as well as expansion plans to double production at both Kofflefontein and Williamson by 2017.

Marange and Artisanal Production

The Marange fields in Zimbabwe were at one point one of the largest commercial alluvial diamond mining operations in the world, peaking with production of approximately 12 million carats in 2012. However, production has rapidly fallen since as most of the easily minable gravel has been depleted, leaving harder conglomerate rock which requires substantial capital investment to produce. Production in 2015 was an estimated 4.5 to 5 million carats, with production estimated to further contract in 2016 as the operators have yet to commit the capital necessary maintain output levels of previous years.

The Democratic Republic of Congo continues to represent the world’s largest source of artisanal diamond production by volume, representing an estimated >5% of global output, however the diamonds continue to be the lowest valued in the world at <$10/ct. Angola remains the second largest source of artisanal production representing 2-4% of global output by volume, but at a much higher average price-per-carat than the DRC at >$100/ct.

Processing plant progress at Gahcho Kué project, North West Territories, Canada. Source: Mountain Province Diamonds.

New Mines and Development Projects

In Canada, Gahcho Kué (51% De Beers/49% Mountain Province Diamonds, TSX: MPV), the world’s largest new diamond mine, is on pace to commence production in Q3 2016. As of December, construction was over 80% complete, with the focus over the next 6 months on commissioning the primary crusher and plant. Overburden mining has also begun. 100 skilled workers were hired for the project from Snap Lake after the mine was put on care and maintenance in December.

Also in Canada, Stornoway’s (TSX: SWY) wholly owned Renard project is ahead of schedule with commissioning on pace to begin in the second half of 2016, with commercial production set for Q2 2017.

Production at Firestone Diamond’s (LSE: FDI) Liqhobong mine is expected in Q4 2016, slightly behind original schedule, due to weather and overburden challenges. The project is fully financed through production ramp-up in 2017, when production is estimated to reach 1M carats a year. Liqhobong was discovered by De Beers in the 1950’s.

At Kimberley Diamonds’ (ASX: KDL) Lerala mine, tailings dam construction has commenced, and first production is scheduled for April 2016. Lerala will target production of ~400,000 carats per year. The asset was acquired by Kimberly Diamonds in February 2014 through the acquisition of Mantle Diamonds Ltd. Initial geological work at the property was done by De Beers and later DiamonEx, with trial mining done by Mantle Diamonds.

Drill core from Rio Tinto’s Bunder project, Madhya Pradesh, India. Source: Rio Tinto.

DiamondCorp’s (LSE: DCP) Lace mine is expected to ramp up to full production in the second half of 2016. The mine is estimated to produce a half-million carats annually until 2040, with peak production hitting 540,000 carats. 7,500 carats were produced through end of last year’s commissioning, with a standout 22-carat, H-color diamond that will be cut into an 8-carat emerald, selling for $110,000.

Rio Tinto’s Bunder project in India is a $500M capex project, currently pending construction permits, of which India is notoriously slow for granting. India has a very early history of diamond mining but currently is only involved in the mid-stream segment of the industry, where it represents over 80% of global market share by volume of the segment.

In 2015, Paragon Diamonds (LSE: PRG) was actively seeking financing to bring it’s Lemphane project in Lesotho into production and also to close a pending acquisition of Lucara’s (TSX: LUC) Mothae asset. However, Paragon’s failure to secure financing by the end of last year resulted in the official termination of its agreement with Lucara, and further delayed the progression of Lemphane, which has an estimated 10 year mine life based on annual production of <50,000 carats.

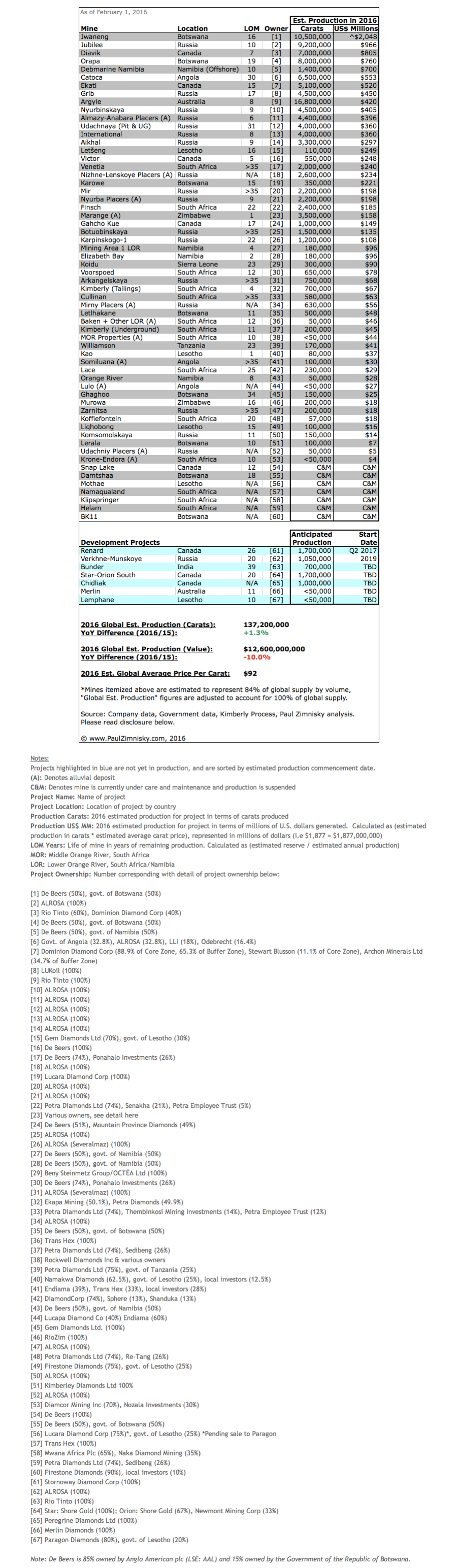

Itemized Detail of World’s 60 Largest Diamond Mines