Gold after trump wins

Gold’s earlier big down days helped fuel fears another Trump administration is bearish for gold.

Image by: The Javorac

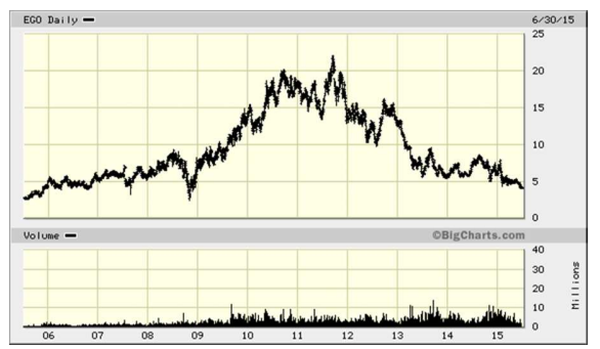

Much opprobrium has been heaped upon Kinross for “dumb deals” but little has been said about Eldorado Gold. Despite this Eldorado has been a very poor share price performer in recent years and much of that has to do with its own deal history. While it did a clever deal in acquiring its Chinese assets at the point it did, they are not a drag on the share price rather than a help.

One does not have to be a genius to know that splitting off the Chinese assets from the rest of Eldorado has the potential to electrify the stock price of both halves of this business. There are three truisms:

These sound like good enough reasons alone to create a spinco of the Asian business and send it on its merry way. It is more than likely that this entity (listed in Hong Kong?) would quickly attract a bidder and be taken out giving long-suffering shareholders a premium. A goodly chunk of the group debt could be pushed out into the Chinese spinco.

This would leave the rump of Eldorado. This is composed of the Turkish assets (two producing mines), $500mn in cash (at March quarter end), the Greek assets and the Brazilian activities. In Brazil, it owns the Vila Nova iron ore mine and is advancing the Tocantinzinho gold project (2P Reserves of 1.9 Moz Au @1.43 g/t). The Vila Nova mine is currently on care and maintenance pending a recovery in iron ore prices. In Mexico there are no interests these days. Quite clearly having one operating asset (in the future) does not make EGO into a Latin American mining company. But then again, it doesn’t have to be.

Other sorts of combos could be pondered. For instance it could combine its Turkish assets with Alacer Gold (TSX: ASR and ASX: AQG) and list the merged entity on the Istanbul Stock Exchange, here there is only one listed miner worth mentioning (Koza Altin).

It could take a run at some beaten down gold-producing assets or advanced projects in Latin America. Mexico is an obvious place to go hunting. Chesapeake Gold could be a good fit to bulk up in Mexico via an all-stock bid.

It could venture a merger-of-equals type arrangement with Iamgold.

Alternatively, it could spin out China and Turkey (in the aforementioned merger with Alacer) and retain some stock to sell/place into strength thus bringing cash in to fund an acquisitions war chest. It already has a mighty war chest but one can never have too much money in the current bargain basement market for mining assets. Really daring would be going after Patagonia Gold (PGD.L) or Everton (EVR.v).

Orosur, the Uruguayan/Chilean gold miner could be snatched up. More daring would be going after Mandalay, the gold/antimony/silver miner which straddles Australia, Chile and Sweden. The opportunities and configurations are virtually endless for a cashed-up (ex-China) Eldorado as it would also have stock that it could use as currency.

The problem of “what might have been” in the mid-tier Canadian players is a constant. The mid-tier gold group on the TSX has shown themselves to be more than exceptionally unimaginative, even by the low standards of the mining industry. The ”rescue” of Osisko by Yamana/Agnico just about took the cake for uninspired deals and summed up the level of deal-doing skills in the mid-tier.

It doesn’t take a genius to work out what ails Eldorado and the cure thereto. The question now becomes whether the company will self-medicate or the “corporate doctor” will come from outside the company.

Important disclosures

I, Christopher Ecclestone, hereby certify that the views expressed in this research report accurately reflect my personal views about the subject securities and issuers. I also certify that no part of my compensation was, is, or will be, directly or indirectly, related to the specific recommendations or view expressed in this research report. Hallgarten’s Equity Research rating system consists of LONG, SHORT and NEUTRAL recommendations. LONG suggests capital appreciation to our target price during the next twelve months, while SHORT suggests capital depreciation to our target price during the next twelve months. NEUTRAL denotes a stock that is not likely to provide outstanding performance in either direction during the next twelve months, or it is a stock that we do not wish to place a rating on at the present time. Information contained herein is based on sources that we believe to be reliable, but we do not guarantee their accuracy. Prices and opinions concerning the composition of market sectors included in this report reflect the judgments of this date and are subject to change without notice. This report is for information purposes only and is not intended as an offer to sell or as a solicitation to buy securities. Hallgarten & Company or persons associated do not own securities of the securities described herein and may not make purchases or sales within one month, before or after, the publication of this report. Hallgarten policy does not permit any analyst to own shares in any company that he/she covers. Additional information is available upon request.