Mining’s old guard needs strong medicine

A new report details subpar investor returns in the mining industry over the last decade, particularly big cap diversified companies which have not adapted to new realities.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I recently wrote an article on how to best position for a potential rise in silver in 2013. The article was called A High Risk/High Reward Play For Silver In 2013. After writing the article, I started to wonder whether a similar strategy would work for gold.

If you have read my earlier articles, you know that I am not a big fan of gold. For gold to go up, I feel that a few things have to be in place:

1) Inflation expectations have to be high. This is not the case as explained in my previous article Should Investors Worry About Inflation Or Rising Rates? Probably Not.

2) The US Dollar has to weaken against other currencies. This is not likely to happen as explained in my previous article Betting On A Dollar Crash And Consequent Gold Bull In 2013? Don’t.

3) The demand for physical gold has to strengthen. This is unlikely. In fact, demand may drop as explained in my previous article Can Gold Survive Lack Of Demand In India?

Based on these triumvirate of low inflation, unlikely dollar crash, and low demand for the physical metal, I concluded in a previous article that Gold Should Go Sideways In 2013.

That said, I believe that there is still substantial money to be made from a sideways movement of gold in 2013. This emulates my strategy for silver in 2013, which is to buy puts on leveraged, inverse ETFs on gold, which will erode from the volatility of gold prices even if the trend is flat. Let’s examine some of the gold ETFs.

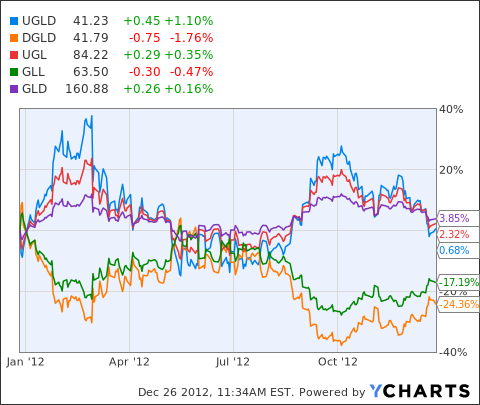

The core gold ETF is the SPDR Gold Trust ETF (GLD) which tries to reflect the price of gold bullion. As the chart above shows, the ETF is up about 4% over the past year. However, over the past 5 years the ETF has almost doubled.

Then comes the 2x leveraged ETF pair, the ProShares Ultra Gold ETF(UGL) and the ProShares Ultrashort Gold ETF (GLL). Both of these try to replicate on a daily basis 2x or -2x the performance of the gold bullion. As the chart shows, UGL is up about 2% for the year, while GLL is down about 17%.

So, while the base ETF is up slightly, the 2x leveraged bull ETF is up but less than the base ETF, and the 2x bear ETF is not only down, it is down by much higher than the 5-10% that one would have expected it to drop. To understand the rationale behind the phenomenon, interested readers should look at my article From Russia With Love: A Big Gain/High Risk Play. I explain there how when the underlying entity stays almost flat, but has a high volatility, leveraged ETFs start to erode fast.

Then comes the 3x leveraged ETF pair, the VelocityShares 3x Long Gold ETN (UGLD) and the VelocityShares 3x Inverse Gold ETN (DGLD). As the chart above shows, UGLD is flat, while DGLD is down 24% in the past year. This is to be expected as these 3x ETFs are leveraged even more than the 2x ETFs, so are expected to erode faster.

So, how can gold investors profit from this in 2013? To me, the best way is to buy puts on GLL. Over the past 5 years, as GLD has almost doubled, GLL has lost about 75%. This means investors who shorted GLL would have quadrupled their investment.

The July 2013 expiration 58 strike puts on GLL are trading at $2.80/3.40 (bid/ask). So what is the expected profit of buying these puts? A Monte Carlo simulation is handy.

I assumed that GLD stays flat in 2013 and its daily volatility remains unchanged. With that, I created a set of 140 daily returns for GLD, and 140 daily returns for GLL leveraged at -2x for GLD. At the end of the 140 daily returns, I estimated the price of GLL and that of the July 2013 strike 58 put on GLL. I assumed that the cost to buy the put is midway between bid/ask, or $3.10. Over the 5000 Trials, the 95% confidence interval for the expected return of buying this put is 53-67%. In other words, there is a 95% probability that this put returns 50%+ in 2013, if GLD were to return 0%.

If GLD returns 10% in 2013, the expected return of the put with 95% probability is 153-174%. If GLD returns 5%, about the same as in 2012 which was a rather poor year for GLD, the expected return of the put with 95% probability is 97-110%. I think it is safe to assume that 50%+ return with this put is not unreasonable, if investors believe that gold will at least stay flat in 2013.

Of course, investors are risking 100% downside as well, as the put may expire worthless. What if gold drops in price in 2013? The 95% confidence interval for returns if gold is down 5% in 2013 is 3-15% for this put. So, there is a still a 95% probability of a positive return from this put if gold is down by 5%.

If gold is down 10%, however, this put will end in a loss of 8-18% with 95% confidence. In other words, if gold is down 10% in 2013, there is statistically speaking little difference between buying this put and owing GLD outright.

What if gold is down 15/20/25%? Then this put starts to lose money fast. At a 15% erosion in price of gold, the put is down 40-50%. At a 20% erosion in price of gold, it is down 65-70%. And if gold goes down by 25% in 2013, it is down by more than 80%.

When it comes to buying puts, my rule of thumb is that unless there is an upside to buying the put compared to the underlying, I wouldn’t even buy the put. By that logic, investors who believe that there is a more than 10% downside to the price of gold in 2013 would be better served to consider strategies involving the underlying GLD ETF itself.

Disclaimer: This is not meant as investment advice. I do not have a crystal ball. I only have opinions, free at that. Before investing in any of the above-mentioned securities, investors should do their own research, consult their financial advisors, and make their own choice. I am merely stating what I personally plan to do for my own portfolio.