Australia to propose tax incentives for critical minerals

The proposed law will set up a tax incentive worth 10% of relevant processing and refining costs for 31 critical minerals.

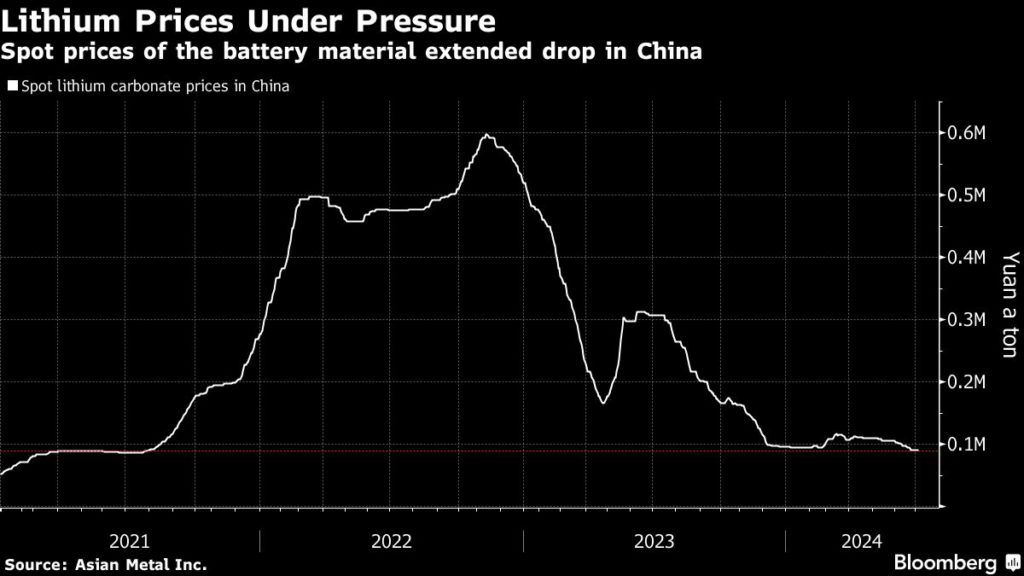

With lithium prices languishing near three-year lows and showing no signs a recovery is coming, attention is now turning to whether miners will be forced to rein in supply of the battery metal.

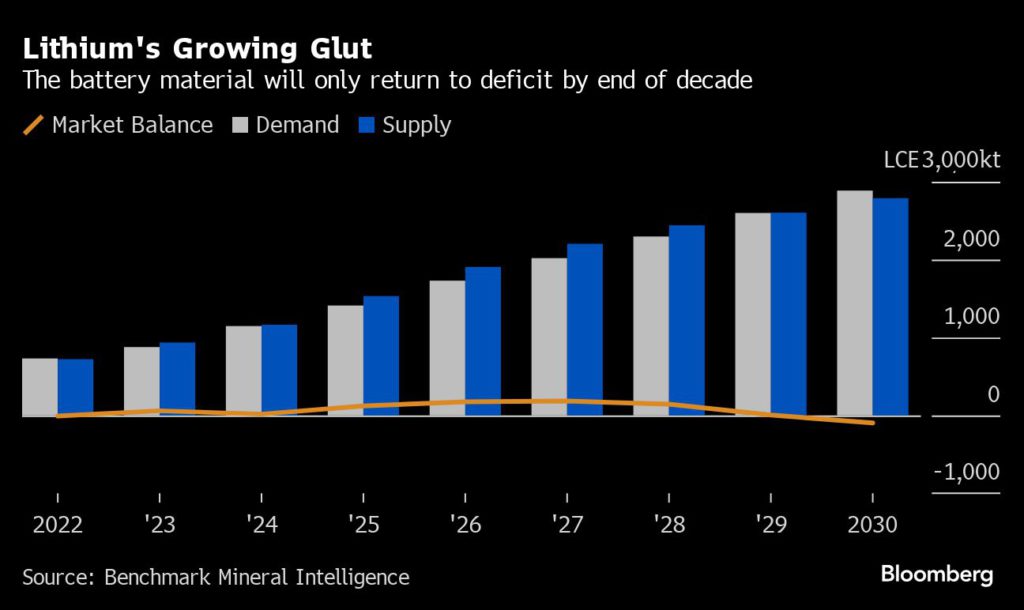

The price of the material that’s vital to the energy transition has plunged by around 80% since late 2022, and Benchmark Mineral Intelligence sees the current glut deepening through 2027. While some smaller producers have already cut output, the question now is whether the bigger firms will choose to shutter mines and delay projects from Australia to Chile.

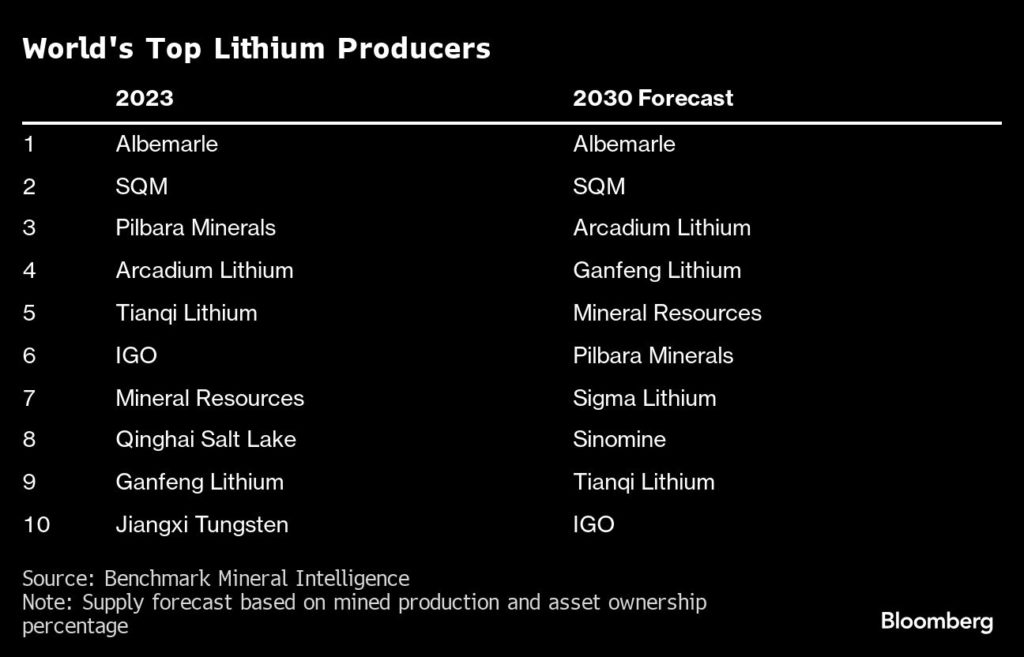

Clearer indications of the intentions of some top miners may be revealed in the coming weeks with the release of quarterly production reports or earnings. The insights from Pilbara Minerals Ltd., Mineral Resources Ltd., Albemarle Corp. and Arcadium Lithium Plc may provide clues on what the supply response might look like.

A prolonged period of low lithium prices could “trigger a renewed wave of mine supply cuts and project delays,” said Alice Yu, the lead metals and mining research analyst at S&P Global Commodity Insights. Prices for spodumene, a lithium-bearing raw material, dropped last week closer to the level when mining output cuts previously occurred between mid-January and end-February, according to data from Platts.

Lithium remains in the doldrums due to slowing growth in electric-vehicle adoption and increased supply. Spot prices of lithium carbonate in China have been hovering near the lowest since March 2021.

The market is expected to see a growth in supply of 32% in 2025, outpacing demand expansion of 23%, according to Benchmark Mineral. The surplus is set to peak in 2027 before a deficit returns at end of the decade, the consultancy said.

Some smaller players have already reacted to the prolonged price slump. Australia’s Core Lithium Ltd. said this month it would halt operations at its Finniss project. In China, two of Zhicun Lithium Group Co.’s carbonate units will be put into maintenance from this month.

The weaker demand-growth outlook for EVs has continued to put downward pressure on lithium, with China’s market maturing while European and American consumers delay purchases.

The EV tariffs imposed by the EU and US against China products “have not only weighed on sentiment but have led to a drop in real-world lithium hydroxide demand,” said Claudia Cook, an analyst at Benchmark Mineral.

Chinese industry giants Ganfeng Lithium Group Co. and Tianqi Lithium Corp. both swung to preliminary net losses in the first half. While major miners such as Pilbara Minerals are still aiming to expand output, there’s growing pressure on other miners to curtail production.

“We’ve downgraded supply forecasts for Brazil, Chile, Argentina, and Australia due to diminished profit margins,” said Linda Zhang, the battery materials lead for Asia Pacific at CRU Group.

Some producers are clinging on despite having little to no profit margin, Benchmark Mineral’s Cook added, citing reasons including maintaining a skilled workforce, avoiding restarting-production costs, and preserving relationships with their buyers.

The stronger focus on supply comes as hopes fade for a significant demand rebound this year, with the supply chain still working through inventories and carmakers rethinking their EV strategies. BloombergNEF last month slashed its EV sales estimates and warned that the auto industry is falling further off the track toward decarbonization.

The question now is how long lithium companies will be able to maintain output should prices remain stagnant, or even fall further.

Curtailments and project deferments are expected to “peak next year,” and that could tighten the market balance in the medium term, CRU’s Zhang said.

(By Annie Lee)

Comments