Column: Trump 2.0 won’t reverse Biden’s critical minerals push

Donald Trump has described the Inflation Reduction Act (IRA) as a "green scam" and vowed to repeal it after he returns to the White House in January.

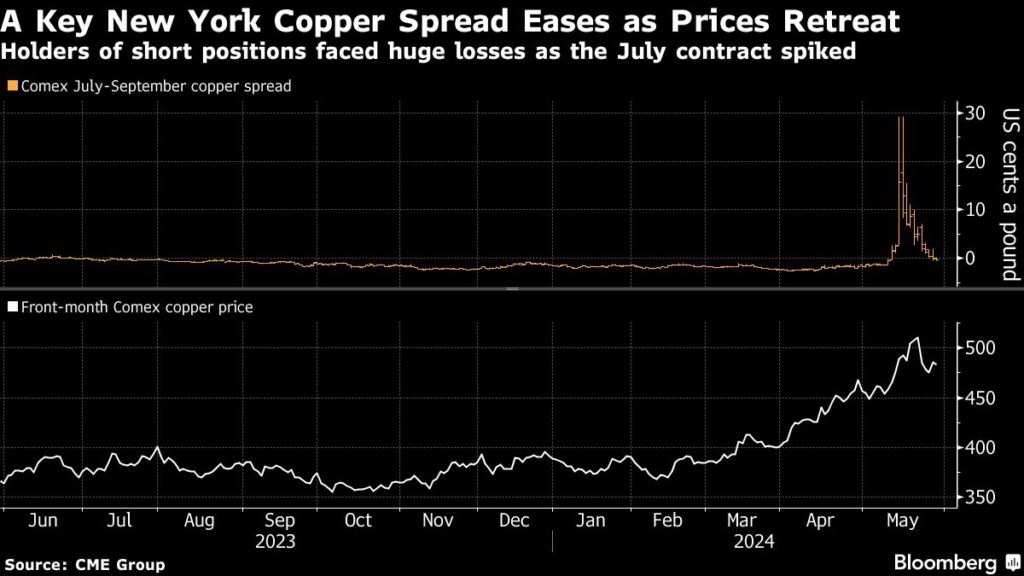

A historic squeeze in New York copper futures is drawing to a close, with the loosening of a key price spread taking the pressure off traders who faced spiraling losses on short positions earlier this month.

July-delivery contracts on CME Group’s Comex exchange traded at a narrow discount to September futures on Wednesday, returning to levels seen before the turmoil began. The spread spiked to a record premium in mid-May, imposing huge mark-to-market losses on financial investors and physical copper traders who were positioned for Comex prices to fall relative to other global price benchmarks.

The initial rally in New York opened a window for traders to profit by buying comparatively cheap contracts in London and Shanghai, and simultaneously selling copper on Comex. Normally that activity would bring prices across the exchanges back into line, but this time traders ran into trouble as bullish investors piled into the Comex contract, making the price disconnect even larger.

Physical traders could still turn a profit by shipping metal into the US to close out short positions in the July contract, and they quickly embarked on a worldwide hunt for the handful of copper brands that could be delivered on to Comex. But their efforts were hampered by constraints on supply and logistical bottlenecks.

Meanwhile, financial traders without the means to deliver metal were left at the mercy of bulls on the other side of the trade. Investors have been piling into the New York copper market in recent weeks, and the spike in prices allowed them to turn a quick profit by selling their July contracts back to holders of short positions and buying cheaper later-dated futures.

Facing huge margin calls, traders could either hang on to their short positions in the hope that prices would fall as the bulls started to cash in, or pay up early and close out the trade at a loss.

With July contracts now trading at a discount to futures, the balance of power has shifted, and shorts can roll their positions forward to later months without taking a hit. Yet even with the July-September spread easing, some analysts see the risk of further price blowouts in future as global shortages materialize.

“Going forward, with copper market surpluses unlikely to develop soon, we see more frequent and volatile price swings across regions,” Bank of America Corp. analysts led by Michael Widmer said in a note. “With physical markets still tight, further squeezes are possible, so CME may not be out of the woods yet.”

The unraveling of the spread has coincided with a broader drop in copper prices in New York, London and Shanghai. Prices on all three markets spiked to a record in the wake of the squeeze, but have been rolling back as bulls took profits and warnings intensified over the weak state of spot demand.

Copper lost 0.5% at $10,448.50 a ton on the London Metal Exchange as of 3:30 p.m. local time, down about 6% from an all-time high struck on May 20. Prices are still up about 22% this year. July Comex contracts traded at $4.7835 a pound, at a small discount to September futures.

(By Mark Burton and Jack Farchy)

Comments