Ivanhoe’s Kipushi zinc mine in DRC officially reopens

The restart marked exactly a century since the mine first went into production.

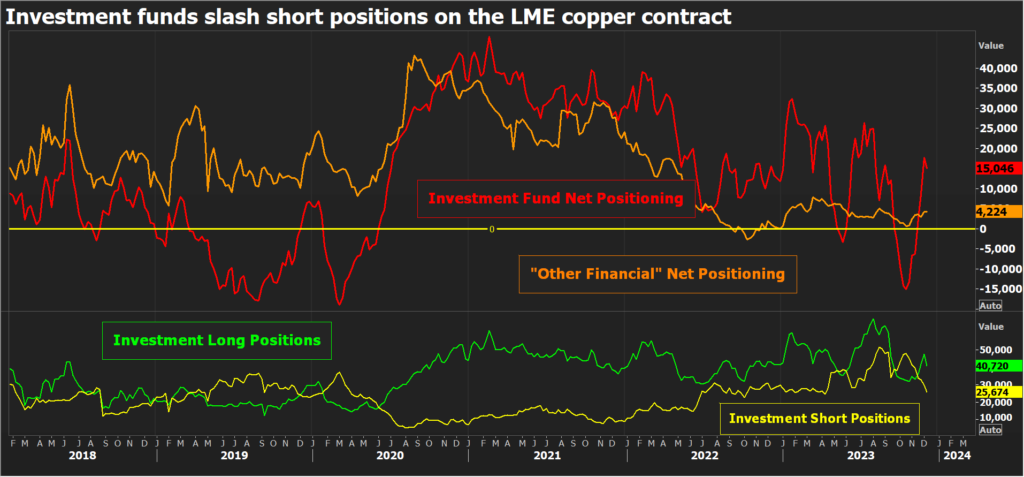

Funds have been reducing their bets on lower copper prices as macroeconomic headwinds abate and the market collectively reassesses copper’s supply dynamics.

Money managers are now marginally net long of copper on both the London Metal Exchange (LME) and CME contracts.

The shift in positioning has been playing out since the end of October, when LME three-month copper was threatening to break down through key technical support at May lows between $7,867 and $7,871 per metric ton.

The anticipated collapse never happened and London copper has since recovered to $8,530.

The price rebound has triggered a change of stance among short-term momentum funds. But the effect has been amplified by expectations that the US rate tightening cycle has passed its peak and by signs that copper supply is not as robust as previously thought.

Fund managers were collectively net short of CME copper to the tune of 21,553 contracts at the end of October, when the price looked likely to break out of its 2023 range on the downside.

They have since shifted to a collective net long of 6,866 contracts, according to the most recent Commitments of Traders Report.

The turnaround reflects a sharp reduction in outright short positions from 76,717 contracts to 46,558 contracts while outright long positions are little changed.

Investor positioning in London has closely mirrored that on the other side of the Atlantic.

Investment funds have collectively flipped from a net LME short position of 15,116 contracts in October to a net long position of 15,046 contracts, with bear bets falling from 47,714 contracts to 25,674.

As with the CME copper contract, there is little enthusiasm for going outright long, particularly among the heavier-weight investment players captured in the LME’s “other financial” category, but the collective short play is over for now.

Federal Reserve Chair Jerome Powell last week said that the US central bank was likely to be done with raising interest rates, which has lifted some of the pressure weighing on copper in recent months.

That change in macro mood music has coincided with a string of bullish developments within copper’s micro dynamics.

Copper supply, once again, is turning out to be a lot less resilient than expected.

Although most analysts are almost universally bullish on copper’s medium-term prospects thanks to the metal’s core role in the energy transition story, the shorter-term outlook was significantly different owing to an expected surge in mine supply this year and next.

However, the prospect of near-term surplus is fading fast.

The first warning sign was the low treatment charges negotiated between Chinese smelters and miners for next year’s deliveries.

Chinese smelters were hoping at the very least to roll over this year’s terms of $88 a ton and 8.8 cents per pound for converting concentrates to refined metal, but they have accepted a reduction to $80 and 8.0 cents respectively for 2024.

The first such drop in three years signalled a mutual admission that the raw materials market wasn’t going to be as well supplied as expected.

It seems to have been a good call. Within days of the benchmark smelter terms being agreed, one major mine has been forced to close while two big producers have downgraded their production guidance.

The Panama government ordered the closure of First Quantum’s Cobre Panama mine this month after the country’s top court ruled that the company’s mining licence was unconstitutional.

The mine entered production in 2019 and generated 350,000 tons of contained copper last year, meaning its loss is a big hit to global supply.

Both Anglo American and Brazil’s Vale, meanwhile, have lowered production guidance for 2024 and 2025.

Anglo has reduced its guidance by 180,000-210,000 tons next year and by 150,000-180,000 tons in 2025, citing geological problems at its Quellaveco mine in Peru and a planned temporary closure of a processing plant at Los Bronces in Chile.

Vale’s updated guidance was less dramatic but sufficient for analysts at Macquarie Bank to take a cumulative 100,000 tons off their mine supply forecasts through 2026.

They are not alone in going back to their supply calculations.

A pretty hard consensus that copper was heading for a period of supply-demand surplus both in 2024 and in 2025 is rapidly unravelling.

The newly emerging consensus is that the concentrates market will at best be balanced and possibly in deficit next year with flow-through implications for the refined market.

Investors are not yet persuaded to go long on copper. LME spreads, currently in wide contango, suggest there is no immediate shortage of copper.

But copper’s shifting statistical landscape has persuaded many financial players there’s little point in expecting copper to break lower any time soon.

(The opinions expressed here are those of the author, Andy Home, a columnist for Reuters.)

(Editing by David Goodman)

Read More: Friedland says $15,000/t copper price needed to spur new mines

Comments