Iron ore weakness to continue into 2025 and beyond, says Fitch Solutions’ BMI

Looking beyond 2024-2025, BMI analysts maintained their view that iron ore prices will likely follow a multi-year downtrend.

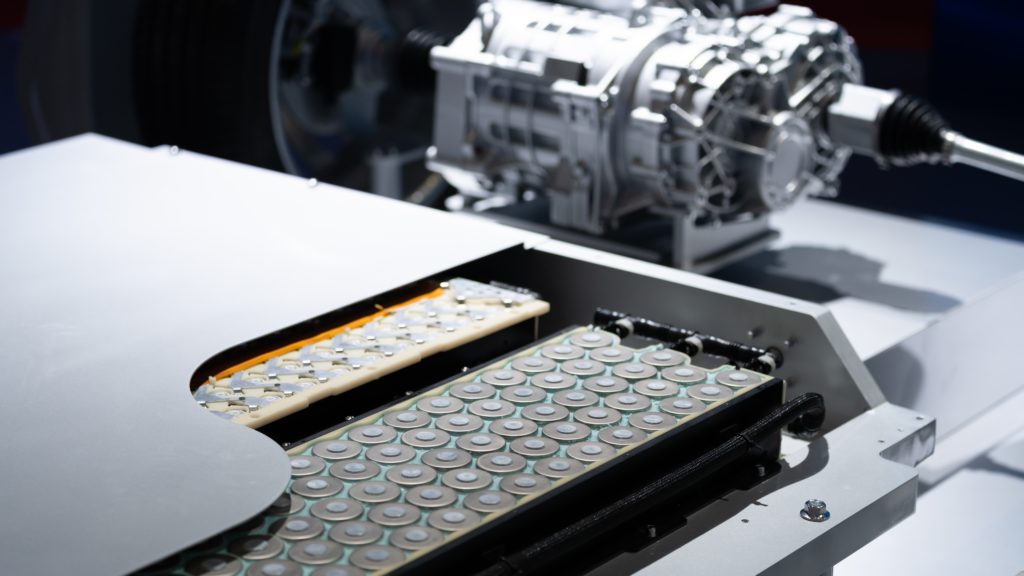

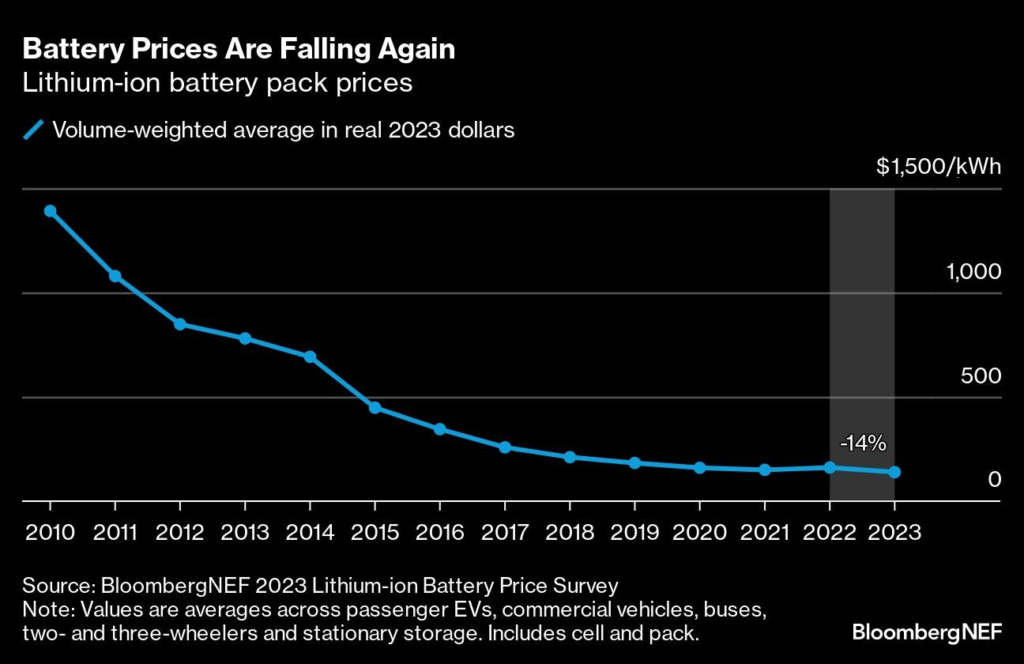

As the auto industry grapples with how to make affordable EVs, the task may get easier by one key metric. Battery prices are resuming a long-term trend of decline, following an unprecedented increase last year.

According to BloombergNEF’s annual lithium-ion battery price survey, average pack prices fell to $139 per kilowatt hour this year, a 14% drop from $161/kWh in 2022.

This is the largest decline observed in our survey since 2018. However, the story behind this price decline is somewhat different than past years.

The main contributor to falling battery prices historically has been technological innovation. This hasn’t been the case in 2023. This year, the drop in battery prices is primarily attributed to lower raw material costs.

Prices of key battery metals — especially lithium — have fallen dramatically since January, due to significant growth in production capacity across all parts of the battery value chain, from raw materials and components to battery cells and packs.

Demand expectations also played a role. Battery demand continued increasing year-on-year, but the second half of the year saw the rate of growth slow in certain EV markets, primarily due to rising borrowing costs and economic uncertainty.

China’s battery production alone exceeded global demand, an indicator of global oversupply. The utilization rate of battery cell manufacturing plants for major manufacturers was also lower this year than in 2022. Plants were not producing at their maximum theoretical capacity, in concert with a trend of some automakers scaling back their targets.

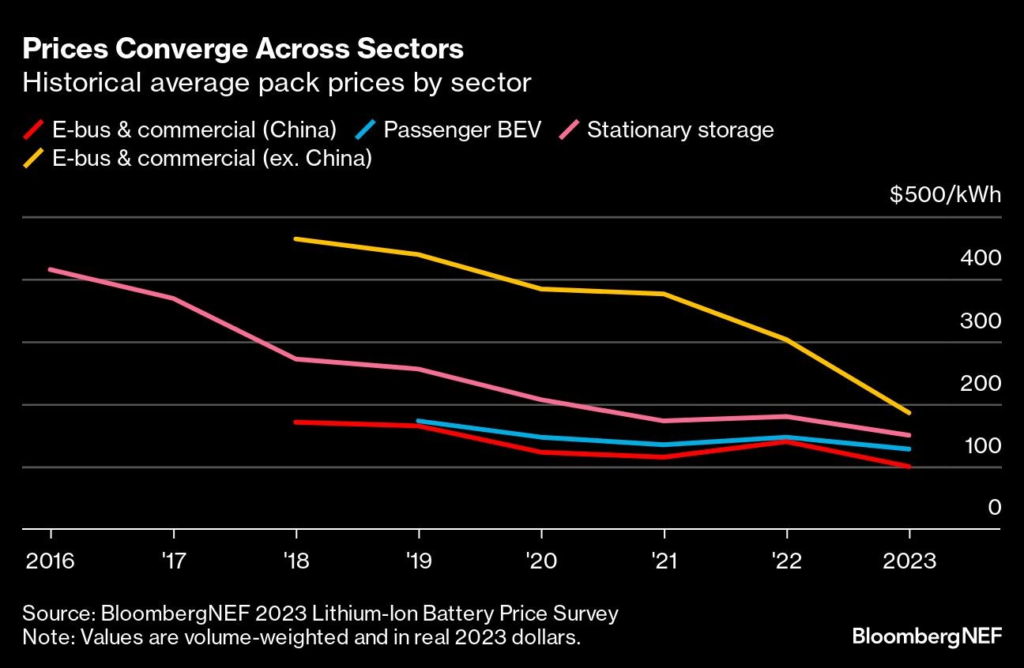

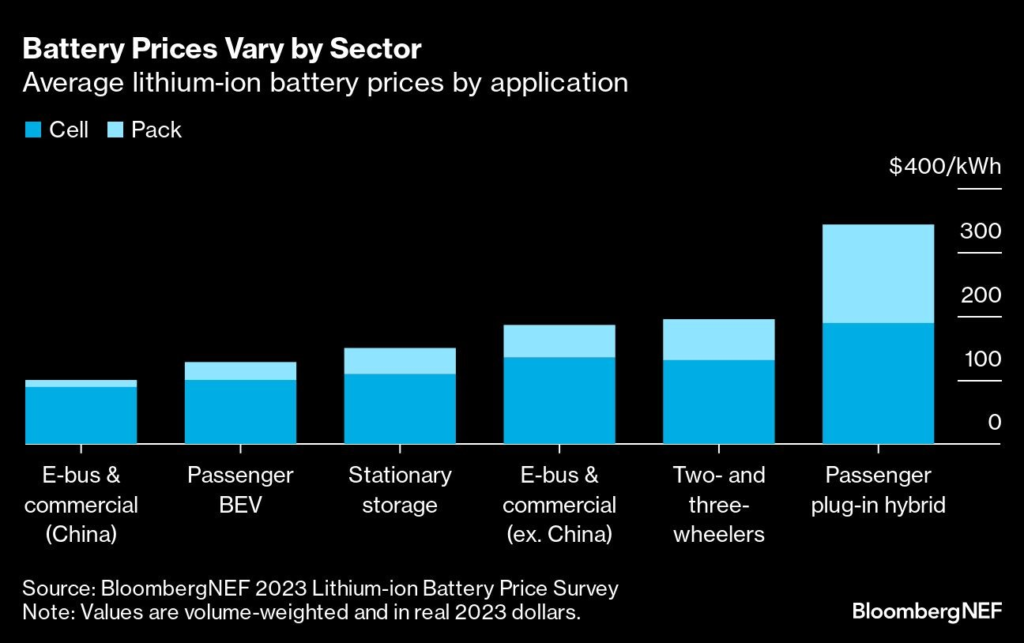

The average battery pack price number is a result of more than 300 survey data points that BNEF collected from buyers and sellers of lithium-ion batteries going into passenger EVs, commercial vehicles, buses, two- and three-wheelers and stationary storage applications. Prices vary by sector, with electric buses and commercial vehicles in China having the lowest prices at $100/kWh. Average pack prices for fully electric passenger vehicles were $128/kWh.

Battery prices across sectors have converged in recent years, which is an indication of the industry’s maturation and growth. Price differences across sectors can be attributed to differences in maturity and order volumes, but also cell and pack design requirements. While different applications will continue to require different specifications, BNEF expects them to follow a similar trend in the future.

The big question, as always, is what happens next. BNEF’s energy storage team expects prices to closely follow the trajectory of raw material prices. We’re projecting pack costs will fall to $133/kWh next year in real 2023 terms. In the long-term, based on the same learning rate as the previous year, battery pack prices are expected to fall below $100/kWh in 2027.

The $100/kWh figure has often been cited as a benchmark for where EVs reach price parity with internal combustion engine vehicles. While it’s a useful reference, the reality around price parity is more complicated. It’s better to think of price-parity points as a range that varies by region and vehicle segment.

Some segments are arguably already at price parity, while others will require much lower prices still. City cars in China, for example, have already crossed the threshold, while pickup trucks in the US are proving more difficult because they rely on large batteries. It’s also worth noting that the $100/kWh is a nominal figure that’s been used for over a decade. Over that period, the price of making an internal combustion vehicle has risen dramatically.

Regional battery price dynamics will play an important role in the coming years as countries look to localize the battery supply chain. Packs are cheapest in China at $126/kWh, and cost 11% and 20% more in the US and Europe, respectively. Higher prices reflect the relative immaturity of these markets, higher production costs, lower volumes, the diverse range of applications and battery imports.

Localization of battery manufacturing in regions such as the US and Europe may push the prices of locally produced battery prices up in the near term. As the industry matures, these costs could eventually come down. Prices are higher due to how much energy, equipment, land and labor costs in these regions compared to Asia, where most batteries are currently produced. Local policies such as the $45/kWh production tax credit for cells and packs under the Inflation Reduction Act in the US could offset part of the cost, though the effect on pricing is not yet clear.

These past couple years have shown that battery prices don’t always follow a simple downward trajectory. There may be bumps along the way, due to input costs or supply-and-demand dynamics. At the end of the day, there’s still a long way to go to make batteries and EVs more affordable, and this endeavor will require continued investment in capacity expansion, research and development, and manufacturing process improvements.

(By Evelina Stoikou)

Comments