Mining’s old guard needs strong medicine

A new report details subpar investor returns in the mining industry over the last decade, particularly big cap diversified companies which have not adapted to new realities.

Citigroup Inc. has been buying large volumes of physical aluminum and zinc on the London Metal Exchange, in a bold metal-financing trade that’s made it one of the biggest players in the market in recent months.

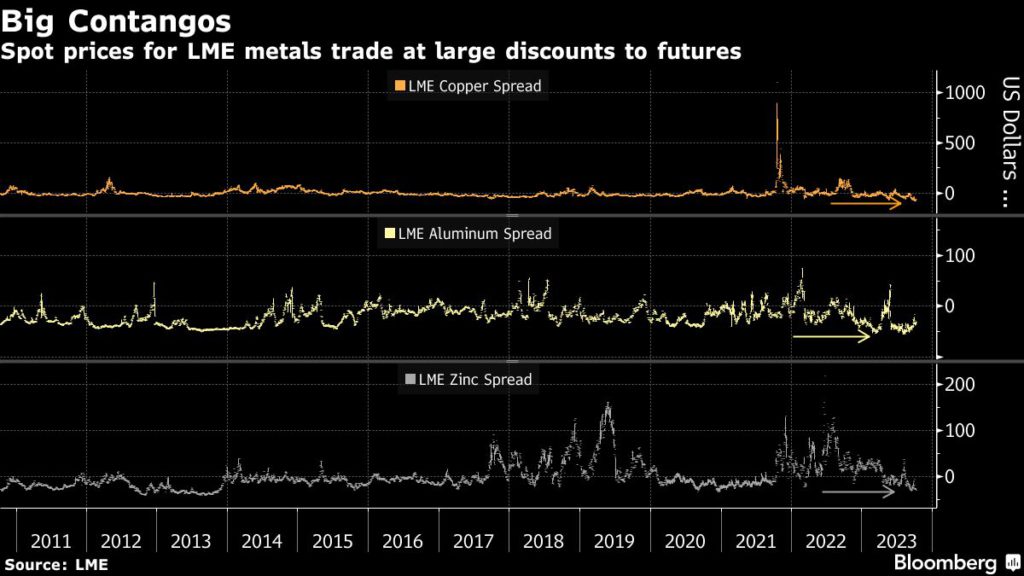

The purchases mark a return of a major driver in metals from the post-financial-crisis years: too much supply in the market drives spot prices much lower than contracts for later delivery, creating opportunities for companies that can buy up metal cheaply and hold it while selling forward at a profit.

In the last few months, Citi requested delivery of about 100,000 tons of aluminum and 40,000 tons of zinc — worth over $300 million, according to people familiar with the matter. The purchases are for Citi’s own trading book and are part of a metal financing play, said the people, who asked not to be identified discussing private information.

The trade has made Citi and other financial players something of a buyer of last resort for Russian aluminum — which now makes up the bulk of LME inventories — keeping it flowing through the LME system at a time when some feared it might become unsellable.

While other banks and traders have also put on financing trades, the scale of Citi’s move has captured the attention of metals markets — for a comparison, its aluminum purchases are equal to more than half of the readily available metal left registered on the LME, and nearly all of the remaining zinc inventories. While the US lender has a large commodities business, it has traditionally been overshadowed by the likes of JPMorgan Chase & Co. and Goldman Sachs Group Inc.

As the era of cheap money comes to an end, Citi, as one of the largest US banks, has a competitive advantage as its cost of dollar financing is significantly lower than most rival banks and trading companies.

Citi has struck a rent agreement with at least one warehousing company to store metal in Taiwan’s coastal city of Kaohsiung, and intends to ship metal there from LME warehouses in Korea and Singapore, the people said, although they cautioned that its plans could still change. Citi may ultimately decide to deliver the metal back on to the LME, one of the people said.

Citi declined to comment.

The size of Citi’s metal play provides the latest evidence that markets are shifting into a period of glut, where spot prices trade at a big enough discount to futures — known as a contango — to make metal-financing trades profitable.

Aluminum prices in August traded at the widest contango in 15 years, copper has in recent days slid to the widest contango in over two decades, while the zinc market is close to its widest contango in a decade.

LME inventories of the exchange’s six main metals fell to the lowest in more than three decades at the start of this year, but since then they have risen 65% to a 16-month high, as China’s slow economic recovery from Covid lockdowns and a downturn in manufacturing elsewhere weighed on demand.

Warehouse executives are anticipating further inflows, registering 14 new facilities on the LME system in the past three months. Most of those are in South Korea, which has become a key delivery hub for Russian aluminum that is being shunned by some buyers in the US and Europe.

The dynamic around Russian material has created an element of jeopardy for the aluminum market since the invasion of Ukraine. There are no blanket sanctions on Russian aluminum, but western producers including Alcoa Corp. and Norsk Hydro ASA have warned that the exchange’s refusal to ban supplies from the country will lead to unwanted metal piling up on the LME and causing the world’s benchmark price to trade out of step with the rest of the market.

However, the fact that Citi is willing to buy large quantities of aluminum out of LME warehouses — much of it of Russian origin — suggests that the worst-case scenario for the LME has been averted.

Financing plays were a dominant theme of the LME’s market in the years after the global financial crisis, when banks and traders bought up warehousing companies and engaged in battles to control and profit from a critical mass of inventory in a period known as the “warehouse wars.”

Citi’s current team includes some people who worked at that time at Deutsche Bank AG, which was one of the largest players in metals financing back then.

The trade has thrust Citi into the spotlight at a time of upheaval for some of its biggest rivals in metals trading. JPMorgan has pulled back from parts of its metals business after playing a central role in the nickel crisis on the LME last year, Bloomberg has reported, while Goldman’s top base metals trader recently left to join trading house Javelin Commodities.

Meanwhile, Citi has also seen changes the top of its metals team, with longtime head Rick McIntire retiring this year, while Lorcan Cleary, who worked in the old Deutsche Bank team and is now at Citi, was promoted to a managing director role.

(By Alfred Cang, Archie Hunter and Jack Farchy, with assistance from Mark Burton)

Comments