Iron ore weakness to continue into 2025 and beyond, says Fitch Solutions’ BMI

Looking beyond 2024-2025, BMI analysts maintained their view that iron ore prices will likely follow a multi-year downtrend.

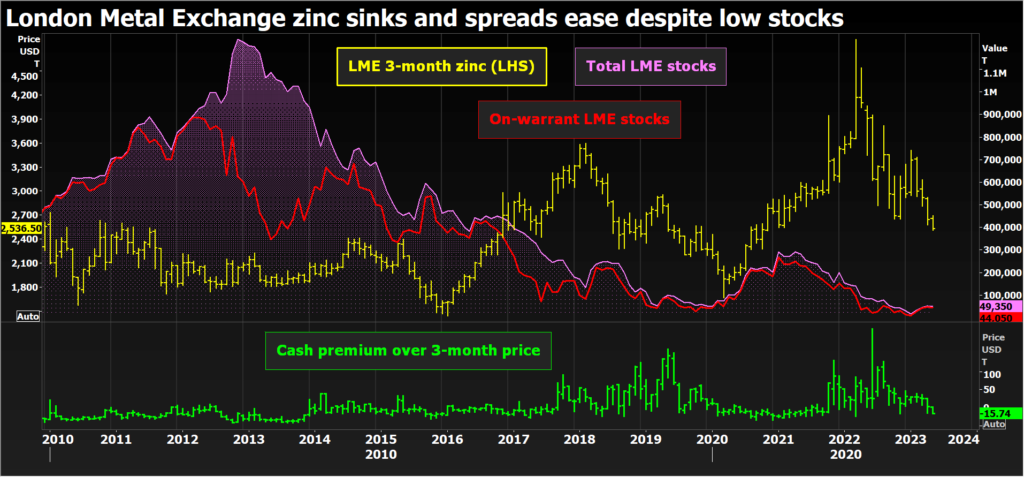

Zinc prices are on the slide, with London Metal Exchange (LME) three-month metal hitting a two-and-a-half year low of $2,517.50 per tonne on Friday morning.

Zinc’s slump is part of a broader price retreat across the base metals complex as China’s post-lockdown bounce-back continues to disappoint.

But zinc is also being weighed down by expectations for a strong rebound in supply this year after a protracted smelter bottleneck in 2022.

The International Lead and Zinc Study Group (ILZSG) still thinks the global refined zinc market will be in supply shortfall this year but it’s slashed its deficit forecast to a modest 45,000 tonnes from 150,000 tonnes at the time of its last statistical update in October.

It’s a fine margin in a 14-million-tonne global market but the shift captures the current bear narrative in zinc, which is down by 15% so far this year, the second-weakest price performance after nickel among the LME-traded metals.

Last year was characterized by a contraction in both zinc usage and refined metal production.

Global demand fell by 3.9% in 2022, led by an estimated 4.9%fall in China, the world’s largest user of zinc, according to ILZSG’s April forecasts.

Around 60% of zinc usage is in the form of galvanized steel, which is widely used in the construction and automotive sectors, both of which were hit hard by China’s rolling lockdowns last year.

The country’s demand is expected to recover by 2.1% this year, matching that in the rest of the world, ILZSG said.

Refined zinc production also fell last year to the tune of 3.8% but it will bounce back by a robust 3.1% this year, an upward revision from the 2.6% growth rate anticipated back in October.

ILZSG expects China’s refined production to rise by “a significant 4% this year” as the country’s smelters capitalize on high treatment and refining charges.

Europe was the weakest link in the supply chain last year with several smelters fully curtailing operations and others reducing run-rates in the face of record high power prices.

The region’s output slumped by 11.4% but will recover by 2.3% in 2023, “influenced by a retraction in energy prices and the resumption of activities at most of the smelters that were idled in 2022,” ILZSG said.

The mismatch in pace between anticipated demand and supply recoveries explains the sharp reduction in the Group’s deficit estimate this year.

Many analysts don’t think there will be a deficit at all. The most recent Reuters poll of analysts generated a median expectation for a 45,000-tonne supply surplus among the 16 analysts that offered a market balance forecast.

Analysts have tempered their price forecasts to reflect zinc’s price slide from a late-January high of $3,512.

The median 2023 price forecast in the May poll was $3,008 per tonne, compared with $3,140 at the time of the January poll.

More downgrades will likely come as China’s huge construction sector struggles to regain lost momentum and the country’s zinc smelters ramp up production. Chinese output of refined metal surged by 7.2% in the first fourth months of this year, according to local data supplier Shanghai Metal Market.

Expectations of supply surplus are growing, which is why the LME zinc price has been locked in a downtrend for the past three months.

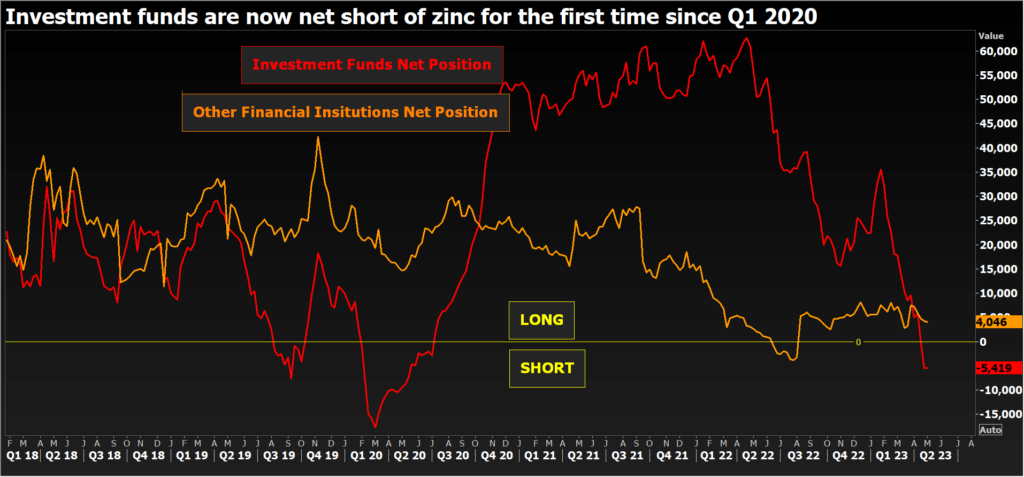

Investment funds are now net short of the LME zinc contract for the first time since early 2020 and LME broker Marex thinks the collective short on the Shanghai contract is at similar historical levels.

However, the much-anticipated surplus hasn’t yet shown up on either the London Metal Exchange or the Shanghai Futures Exchange.

Both have seen stocks rebuild this year but only marginally and from very low levels.

LME registered inventory is up by 18,575 tonnes since the start of January but at 49,050 tonnes is still equivalent to less than two days’ worth of global consumption.

ShFE stocks stand at 59,166 tonnes, up from a depleted 20,453 tonnes at the end of December but already a long way off the Lunar New Year holiday peak of almost 124,000 tonnes.

LME time-spreads are moving into deeper contango, suggesting more metal deliveries are expected. The benchmark cash-to-three-months period closed Thursday valued at a contango of $15.74 per tonne, its widest this year.

The combination of loose spread structure and weak outright price, last trading at $2,530 per tonne, is likely to spur funds to increase their bear bets on a balanced to over-supplied market in 2023.

But confirmation of the bear narrative will only come in the form of a sustained recovery in exchange inventory. Until that happens, low visible stocks are a potential source of tension with the falling price and the build in investor short positions.

(The opinions expressed here are those of the author, Andy Home, a columnist for Reuters.)

(Editing by Sharon Singleton)

Comments