Mining’s old guard needs strong medicine

A new report details subpar investor returns in the mining industry over the last decade, particularly big cap diversified companies which have not adapted to new realities.

(The opinions expressed here are those of the author, Andy Home, a columnist for Reuters.)

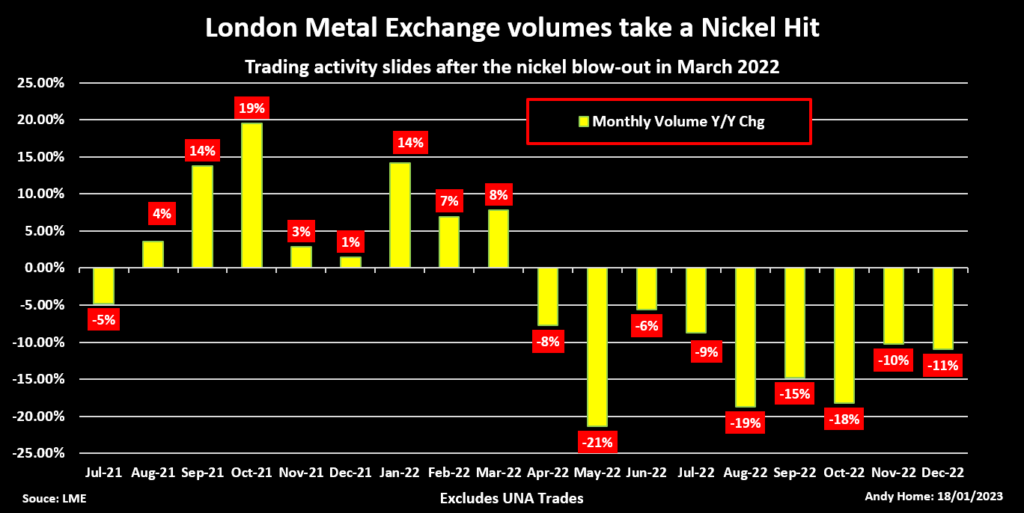

The London Metal Exchange’s (LME) nickel meltdown in March has cast a long shadow over trading activity on what claims to be the world centre for industrial metals pricing.

Volumes have fallen every month year-on-year since the suspension of nickel trading and the decision to cancel trades. Core activity on the LME, which is owned by Hong Kong Exchanges and Clearing, contracted by 8.3% over the full year. The 127 million lots traded was the lowest turnover since 2010.

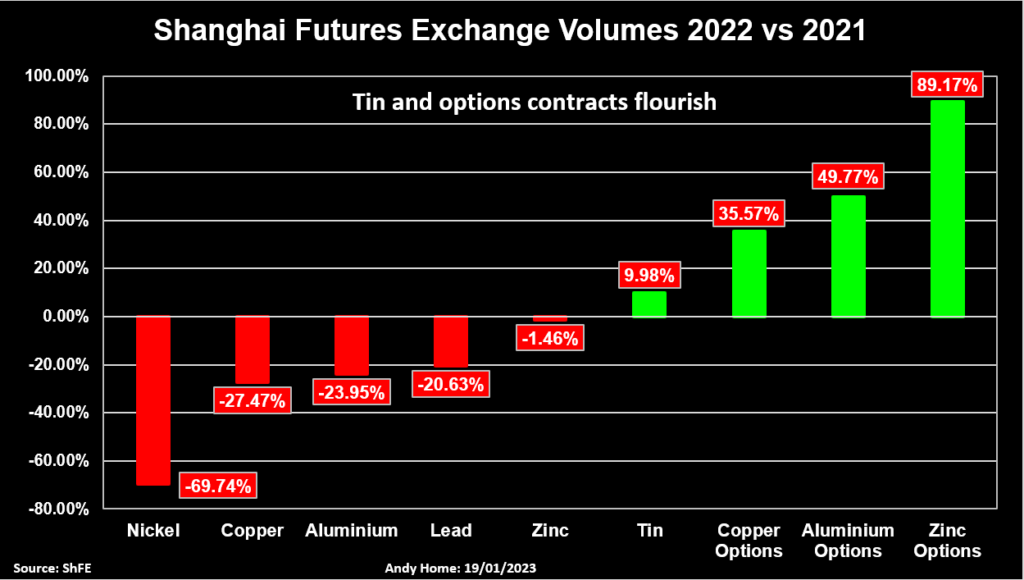

The Shanghai Futures Exchange (ShFE) also suffered significant collateral damage. Its nickel volumes shrank even more dramatically but here too it was just part of a broader retreat across base metals contracts.

While trading of traditional base metals products floundered in 2022, newer contracts fared better. It was a good year for the LME’s widening array of steel contracts and the ShFE saw volumes surge on its new options suite.

The CME is leading the diversification charge with a host of new copper products aimed at investors and a foray into the world of battery metals pricing.

LME nickel volumes slumped by 28% last year, attesting to the loss of confidence in the market after the price melt-up and near exchange meltdown in March.

However, all the LME’s main deliverable contracts registered falls in activity last year. Aluminum volumes slid by 9%, lead volumes by 4% and zinc by 3%. Copper was the most resilient with a year-on-year volume decline of under 2% thanks to a pick-up in action over the fourth quarter.

Nickel was also the worst performer on the Shanghai market, volumes collapsing by 70% year-on-year in 2022. But it was equally part of a broader downturn in activity during what was a year of rolling lockdowns in China. Only tin bucked the trend with a 10% increase in activity.

The base metal blues were also playing in the CME’s flagship copper contract, which saw 2022 volumes slide by 12% and market open interest touch an eight-year low at the end of November.

High pricing, high margins and heightened volatility appear to have frightened off many players from taking futures positions in base metals last year.

Action in the options market, by contrast, has been booming.

ShFE’s copper, aluminum and zinc options contracts, all launched in 2020, registered year-on-year growth of 36%, 50% and 89% respectively.

CME’s vanilla monthly copper options saw a 41% rise in trading activity with market open interest of 82,599 contracts at the end of the year a record high.

CME last year launched copper weekly options, event options and a micro futures contract, all of which have rapidly picked up trading momentum.

The exchange’s copper product suite now looks very similar to that offered in the precious metals space and seems aimed at attracting a similar profile of investor to the copper market.

The CME entered the world of steel trading in 2010 with the launch of a hot-rolled-coil (HRC) contract. Volumes last year were a record 260,885 lots, equivalent to over five million tonnes.

The steel scrap contract, dating back to 2012, has also just recorded its highest-volume year, while activity in the European HRC contract more than tripled to 45,735 contracts in what was its second full year of trading.

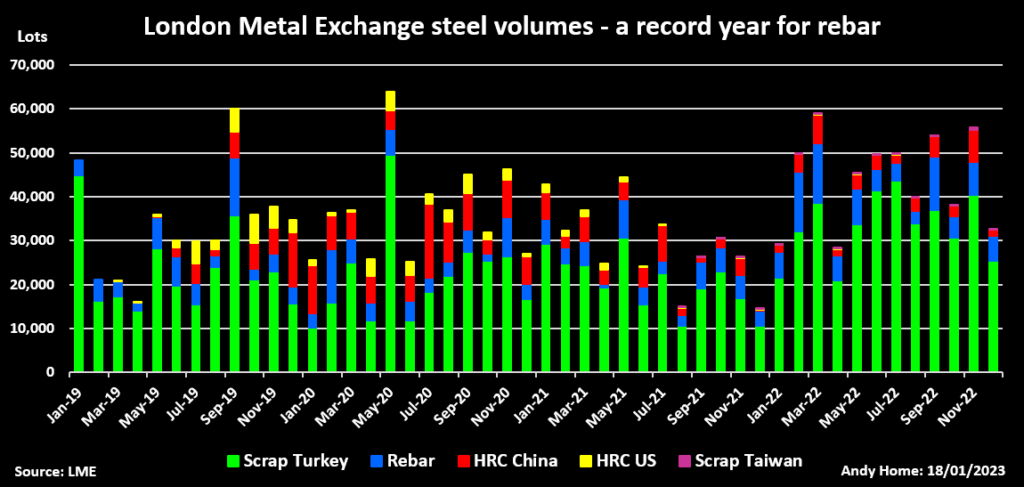

The steel sector’s long resistance to futures pricing appears to be fraying and the LME is also benefiting from increased terminal market participation.

The LME rebar and Turkish scrap contracts marked their seventh anniversary in November. Rebar activity jumped by 65% last year with volumes hitting a record high of 88,698 contracts. Scrap volumes were up by 62% with the full-year total of 399,327 contracts the highest since 2018.

The LME now also offers three HRC contracts and two more scrap contracts for the Indian and Taiwanese markets. The latter in particular seems to be picking up traction with 867 lots trading over November and December, bringing the total to 1,500 in what was the first full year of trading.

The next metallic frontier for futures exchanges is the battery metal sector.

The LME had an early-mover advantage with its cobalt contract, which started trading in 2010. However, activity has been falling sharply over recent years. Volumes last year were just 290 lots, compared with 841 in 2021 and over 14,000 at the contract’s peak in 2017.

The cobalt baton has been taken up by CME, which launched its own product in 2020. Volumes mushroomed from 3,397 contracts in 2021 to 17,119 last year. Open interest at the end of 2022 was a record 12,773 contracts.

The CME’s lithium contract dates from May 2021 and it managed to notch up a minimal 13 lots of turnover in its first 12 months of trade. However, the market burst into life in September, since when volumes have totaled 468 lots and open interest has climbed to 429 contracts.

If lithium trading takes off on the CME, it will pose an interesting challenge to an industry that has firmly rejected any attempt to commoditize or futurize what it views as a chemically unique product.

Growing appetite for cobalt and lithium futures also serves to underline the pricing vacuum around nickel, the other key electric vehicle battery metal.

LME nickel was the anchor price for a wide spectrum of products ranging from refined metal through nickel matte to the new battery streams such as mixed hydroxide and sulphate.

The market’s six-day suspension in March plunged the a global, multi-faceted supply chain into pricing black-out.

Confidence in the anchor price has been severely shaken and the LME has a long hill to climb if it is going to regain the industry’s trust.

The Shanghai market doesn’t look a viable pricing alternative, given the even starker shrinkage in volumes and ShFE’s restrictive physical delivery criteria and resulting chronically low stocks.

Global Commodities Holdings, which operates the globalCOAL trading platform, is planning to launch its own nickel price index by the end of the first quarter.

Based on trades around physical deliveries, it is both a hark-back to the LME’s own 19th-century origins and a warning that the LME’s monopoly on metals price discovery is facing a growing number of challenges.

(Editing by Jane Merriman)

Comments