Iron ore weakness to continue into 2025 and beyond, says Fitch Solutions’ BMI

Looking beyond 2024-2025, BMI analysts maintained their view that iron ore prices will likely follow a multi-year downtrend.

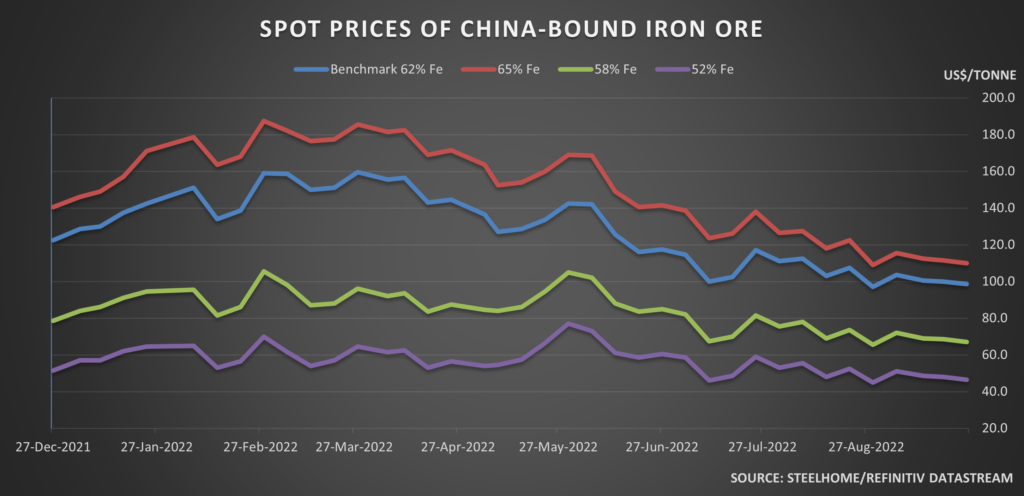

Iron ore prices are on track to end 2022 at their lowest in the last three or four years and will probably languish next year as well, with China and Europe cutting steel output, while pressure mounts from additional supply.

Price forecasts for the key steelmaking ingredient range from about $90 a tonne to a high of $115 by the end of the year, a Reuters survey of five analysts and researchers shows.

Year-end prices have not been in this territory since the 2019 figure of $93 a tonne, itself off the even lower 2018 level of $72.60, data from consultancy SteelHome shows.

“Covid-19 and property sector slowdown continue to weigh down steel demand in China,” said Malan Wu, research director at consultancy Wood Mackenzie.

“Prices in Western countries will remain subdued for the rest of the year because of weak demand, high inflation, and fears of recession.”

Spot prices of ore bound for China, maker of about half the world’s steel, have fallen roughly 40% from this year’s peak above $160 in March, as it sticks to tough Covid-19 curbs and its property sector battles a liquidity crunch and weak demand.

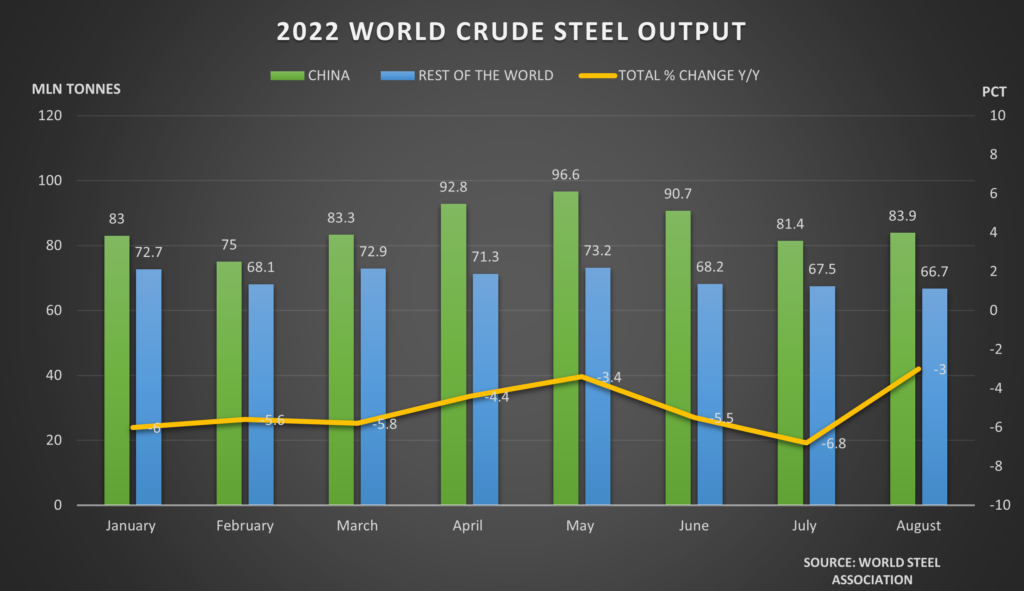

Australia, the world’s biggest exporter of the ore, has projected a drop of 0.6% in global steel output this year to 1.947 billion tonnes, factoring in drops of 2% and 7.1% in China and the European Union, respectively.

“Combined with growing global recessionary fears, new Covid-19 outbreaks and weakness in China’s housing sector have dampened world steel and iron ore demand in recent months,” its government said in a quarterly report this month.

China buys nearly 70% of seaborne iron ore and about two-thirds of that is supplied by Australia.

The fallout from the Ukraine conflict is still hobbling markets, the report added, by drying up ore supplies, while a growing energy crunch hampers Europe’s steel output.

A collapse in ore prices would hit major producers, such as BHP Group, Rio Tinto, Vale SA, and others in Australia and No. 2 supplier Brazil.

But some, such as BHP, the world’s largest listed miner, are unfazed.

“We feel confident enough to say that, at a minimum, China will be a source of stability over the coming year,” said Huw McKay, the firm’s vice president for market analysis and economics.

That confidence is bolstered by China’s resolve to shore up its economy with stimulus measures, in contrast to the global trend towards tightening, he added.

Analysts at J.P. Morgan cut their price forecasts for iron ore last month, to $103 a tonne for the second half of 2022, from $133, and for next year, to $94 from $105.

“As majors grow volumes, Chinese domestic supply will need to be curtailed to make room,” they said in a report last month, projecting an additional 50 million tonnes of supply in 2023 from big producers, including Brazil’s Vale.

Vale’s daily output has risen sufficiently to meet its 2022 volume guidance, the analysts said, after a deadly mine disaster in 2019 forced safety checks and production cuts.

However, Vale has cut its 2022 ore production forecast, partly because of lower market prices, which hurt second-quarter profits and brought a downgrade to “market perform” from analysts at Itau BBA.

Fading hopes for China to relax its zero-Covid rules, along with the usual steel production curbs during the cold months, make prospects uncertain for a price bounce towards the end of the year.

“Europe’s energy crisis and winter curbs in China leave little room for any recovery in steel production in the fourth quarter,” ANZ commodity strategists said in a note on Oct. 7.

(By Enrico Dela Cruz and Praveen Menon; Editing by Clarence Fernandez)

Comments