{kind=link}

{kind=link}

{kind=link}

{kind=link}

Mining’s old guard needs strong medicine

A new report details subpar investor returns in the mining industry over the last decade, particularly big cap diversified companies which have not adapted to new realities.

The rising USDX and more interest rate hikes prospect don’t seem to bother investors. Meanwhile, gold’s outlook for 2022 has worsened significantly.

With the bond market unhinged and equities pretending that all is well, the PMs look like the cleanest shirts in the basket of dirty laundry. For example, bond prices often move inversely to stock prices. When stocks fall, bonds are bid, and the latter serves as a hedge against uncertainty and volatility.

However, with inflation raging and the Fed hawked up, bond prices have been falling, yields have been rising, and risk-on/risk-off sentiment has done little to reassert the historical relationship. However, keep in mind, the bond market is pricing in the implications of the Fed’s war on inflation, while the general stock market and the PMs are not. As such, U.S. Treasuries’ safe-haven bid has evaporated, and in this upside-down world, stocks and commodities are incurring much less volatility.

Thus, please remember that short-term moves in the financial markets are not based on fundamentals. Instead, algorithms analyze sentiment indicators, and as long as momentum is bullish, why worry about medium-term fundamentals?

Think of it like this: we could present a quantitative trader with data that supports medium-term caution. However, he would respond with… who cares? In reality, momentum investors are so short-term-oriented that their strategy is to ride the wave higher and bolt at the first sign of trouble. As a result, with the PMs exhibiting less volatility, momentum investors haven’t seen the red flags that would cause them to exit their positions.

Furthermore, a subscriber asked me if “gold is now the only risk-off asset left standing” and if “this would explain why gold has been so resilient.” To answer, the conclusion is spot on.

With investors hiding out in gold despite its domestic fundamentals falling off a cliff, the Russia-Ukraine crisis has provided cover for overzealous investors. However, while gold permabulls use the elevated price to justify their narrative, the reality is that “those who cannot remember the past are condemned to repeat it.”

For context, we expect the PMs to soar over the long term. However, with the Fed hawked up and its rate hike cycle just beginning, we should witness sharp drawdowns before their secular bull markets continue.

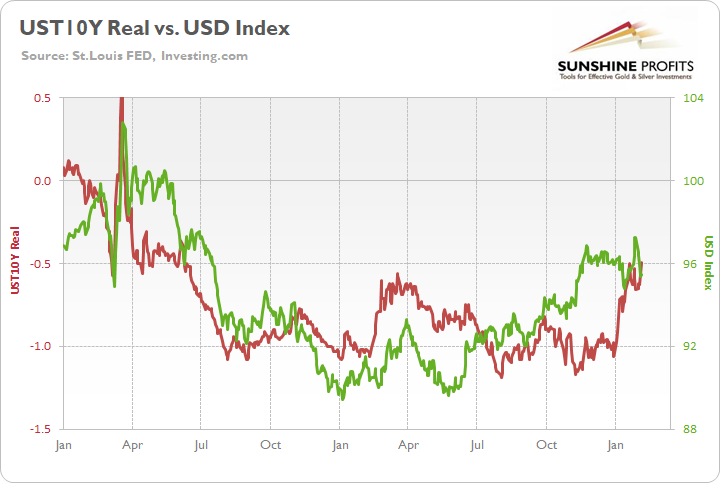

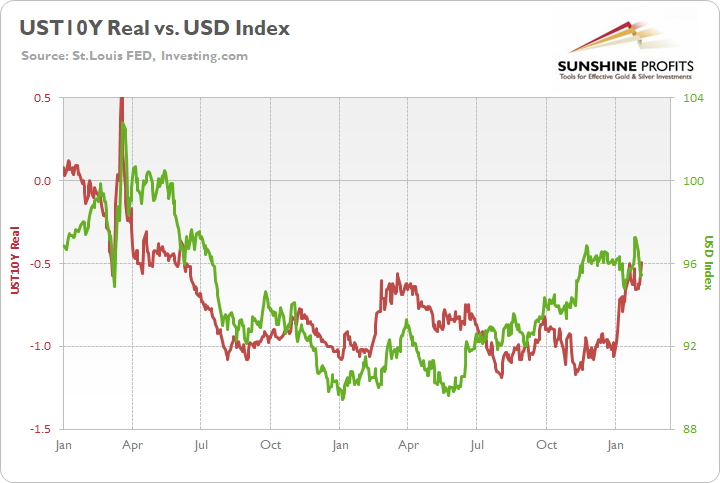

To that point, I’ve written a lot about U.S. real yields over the last several months. With the metric bullish for the USD Index and bearish for the PMs, I warned on Feb. 7 that the former’s short-term pullback contrasted with fundamental reality. I wrote:

To explain, the green line above tracks the USD Index since January 2020, while the red line above tracks the U.S. 10-Year real yield. While the latter didn’t bottom in January 2021 like the USD Index and the FCI (though it was close), all three surged in late 2021 and hit new highs in 2022. Moreover, the U.S. 10-Year Treasury nominal and real yields hit new 2022 highs on Feb. 4.

Furthermore, with the Fed likely to raise interest rates at its March monetary policy meeting, a realization supports a higher U.S. 10-Year real yield, and a higher FCI. As a result, the fundamentals underpinning the USD Index remain robust, and short-term sentiment is likely responsible for the recent weakness.

Therefore, while the algorithms won the short-term battle, the fundamentals won the medium-term war. Moreover, with the U.S. 10-Year real yield surging in recent weeks, the USD Index has responded as expected.

Please see below:

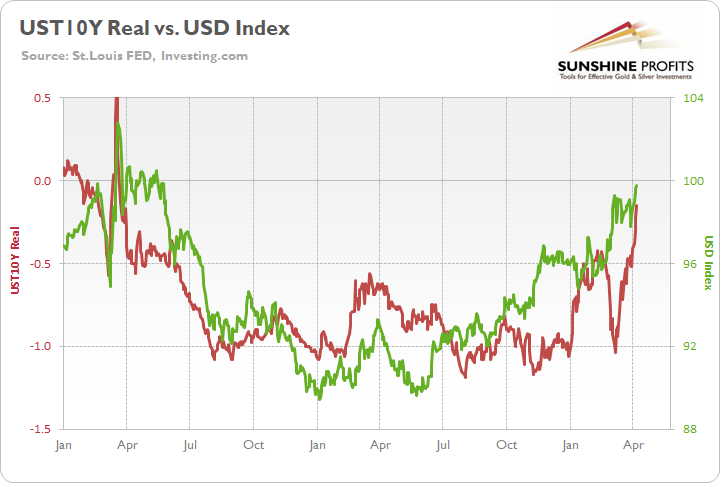

However, gold prices’ persistent optimism is similar to the USD Index’s pullback in February. For example, the algorithms pushed the USD Index lower when momentum turned. However, reality re-emerged as time passed. Likewise, the algorithms are pushing the PMs higher now, but reality should also re-emerge over the next few months.

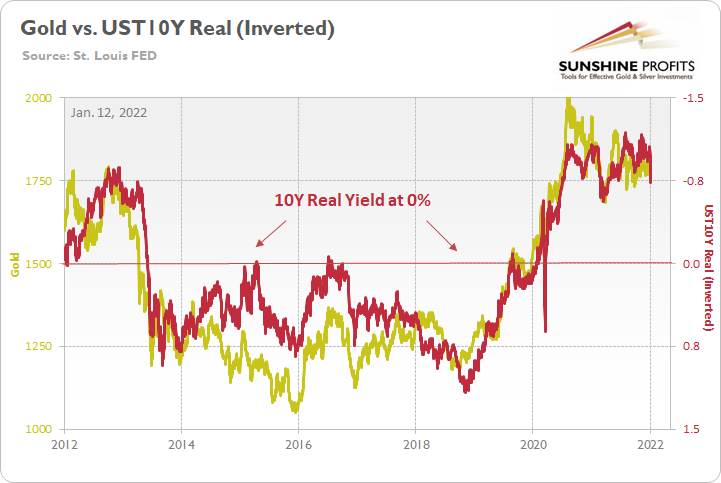

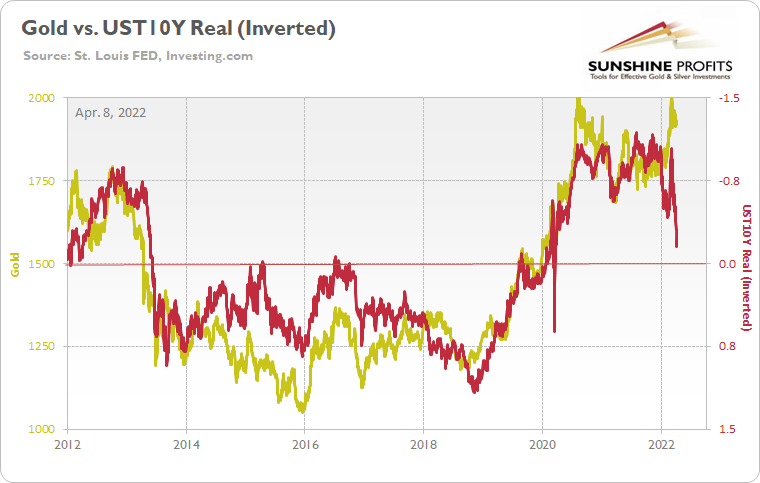

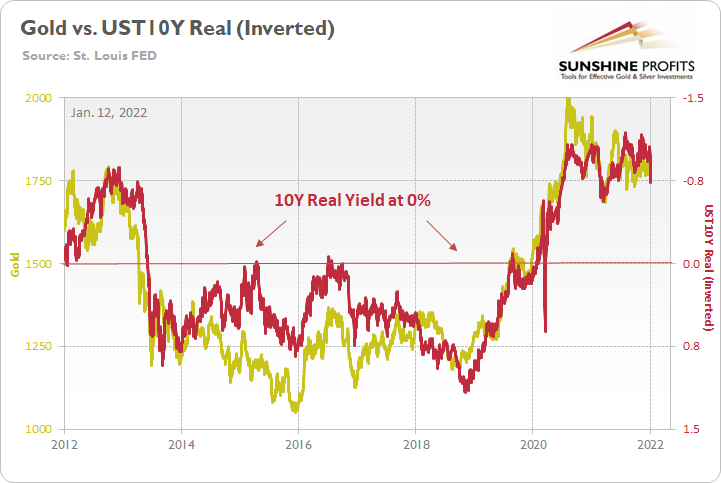

To explain, I wrote on Jan. 12:

The PMs are less volatile than speculative assets. However, it’s important to remember that gold, silver, and mining stocks peaked amid the liquidity-fueled surge in the summer of 2020. Likewise, their uprisings coincided with real interest rates that were at all-time lows at the time.

Conversely, with the Fed’s liquidity drain already unfolding and real interest rates poised to rise in the coming months, the PMs should suffer from the likely re-pricings. For example, when the U.S. 10-Year real yield was at 0% or higher from June 2013 until October 2018, gold was stuck below $1,400 during that timeframe and actually fell below $1,100. As a result, if the Fed pushes its hawkish chips into the middle, don’t be surprised if the PMs fold in 2022.

Please see below:

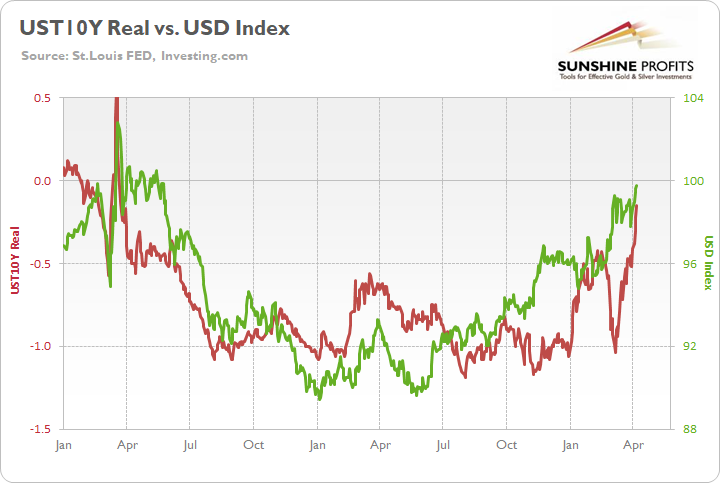

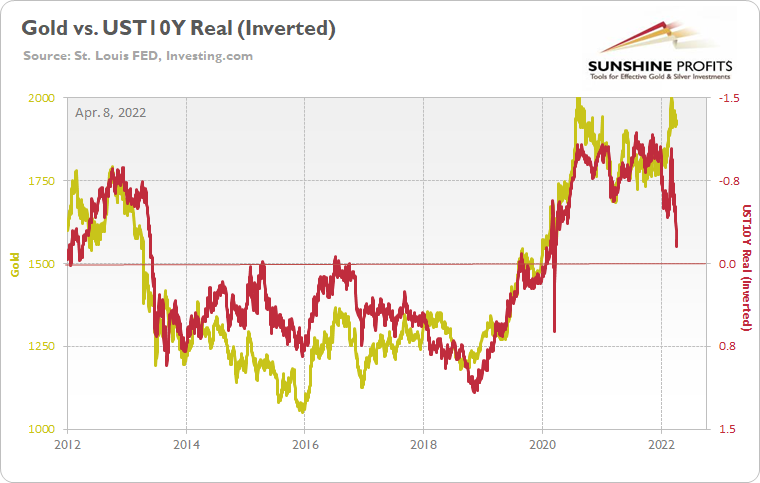

To that point, the U.S. 10-Year real yield has surged in 2022, and hawkish remarks from the Fed lifted the metric to -0.16% on Apr. 7.

Please see below:

For your reference, the gold line above tracks the gold futures price, while the red line above tracks the inverted U.S. 10-Year real yield. For context, inverted means that the latter’s scale is flipped upside down and that a rising red line represents a falling U.S. 10-Year real yield, while a falling red line represents a rising U.S. 10-Year real yield.

If you analyze the left side of the chart, you can see that when the U.S. 10-Year real yield surged during the 2013 taper tantrum (depicted by the red line moving sharply lower), gold plunged by more than $500 in less than six months.

Moreover, if you focus your attention on the right side of the chart, you can see that the U.S. 10-Year real yield is gunning for neutral, and the Fed needs to push the metric above 0% to curb inflation.

As a result, the data couldn’t be clearer, and the fundamental outlooks for the USD Index and the U.S. 10-Year real yield are more bullish now than at the end of 2021. However, because algorithms rule the day in the short term, the timing of when reality will resurface is unclear.

Despite that, if we remove the Russia-Ukraine conflict from the equation, this is one of the worst medium-term fundamental setups for gold in a long time. Therefore, while the permabulls will shout that “this time is different,” history shows that the yellow metal can only ignore rising real yields for so long.

Furthermore, I wrote on Apr. 7 that the FOMC minutes show officials plan to raise interest rates several times in the coming months. Moreover, their use of terms like “faster,” “rapid” and “expeditiously” is not bullish for the PMs or the S&P 500. In addition, the crew also pledged to start reducing the balance sheet by ~$95 billion per month “at a coming meeting.” Likewise, the Fed minutes also stated:

“Many participants noted that one or more 50 basis point increases in the target range could be appropriate at future meetings, particularly if inflation pressures remained elevated or intensified. A number of participants noted that the Committee’s previous communications had already contributed to a tightening of financial conditions, as evident in the notable increase in longer-term interest rates over recent months.”

As a result, the medium-term outlook remains unchanged: the Fed could double up its rate hikes at “one or more” meetings, and the future path depends heavily on inflation. However, with the latter still raging, the chances of a dovish pivot are slim to none.

As evidence, the Institute for Supply Management (ISM) released its U.S. Services PMI on Apr. 5. Moreover, the headline index increased from 56.5 in February to 58.3 in March. The report revealed:

“Prices paid by services organizations for materials and services increased in March for the 58th consecutive month, with the index registering 83.8 percent, 0.7 percentage point higher than the February figure of 83.1 percent. This is its second-highest reading ever, behind the seasonally adjusted figure of 83.9 percent registered in December 2021.”

In addition:

“Employment activity in the services sector grew in March after contracting in February. ISM’s Services Employment Index registered 54 percent in March, up 5.5 percentage points from the reading of 48.5 percent registered in February. Comments from respondents include: ‘Labor shortages seem to be improving as omicron has waned’ and ‘Hiring back to normal levels.’

As such, all of this is bullish for Fed policy.

Likewise, S&P Global also released its U.S. Services PMI on Apr. 5. Here, the headline index increased from 56.5 in February to 58.0 in March. The report revealed:

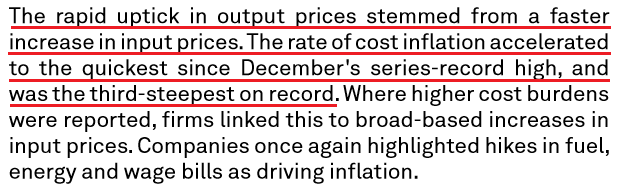

“On the price front, firms recorded a substantial increase in output charges during March. The rise in selling prices was the sharpest on record (since October 2009), as service providers reportedly passed through higher costs to clients, where possible.”

For more context:

Even more bullish for Fed policy:

The bottom line? While momentum remains gold and silver’s best friend, their domestic fundamental outlooks have deteriorated sharply in 2022. The USD Index and U.S. real yields have risen dramatically, and the Fed has turned the hawkish dial up from 60 to 100. However, the PMs have largely ignored all of these troubling developments.

Despite that, though, history shows that technicals and fundamentals win out over the medium term. Moreover, while sentiment remains uplifted for now, the pendulum can swing without warning. When this occurs, the PMs will confront one of the worst domestic fundamental environments since late 2018.

In conclusion, the PMs rallied on Apr. 7, as momentum doesn’t die easily. However, with the bearish medium-term thesis becoming clearer by the day, investors are fighting a battle they haven’t won in 10 years. As a result, while the timing remains uncertain, the PMs should suffer profound drawdowns once sentiment shifts.

(By Przemyslaw Radomski)

Comments