Troilus Gold brings potential funding from ECAs to $1.3 billion

The company has signed an additional LOI with Export Development Canada worth $300 million.

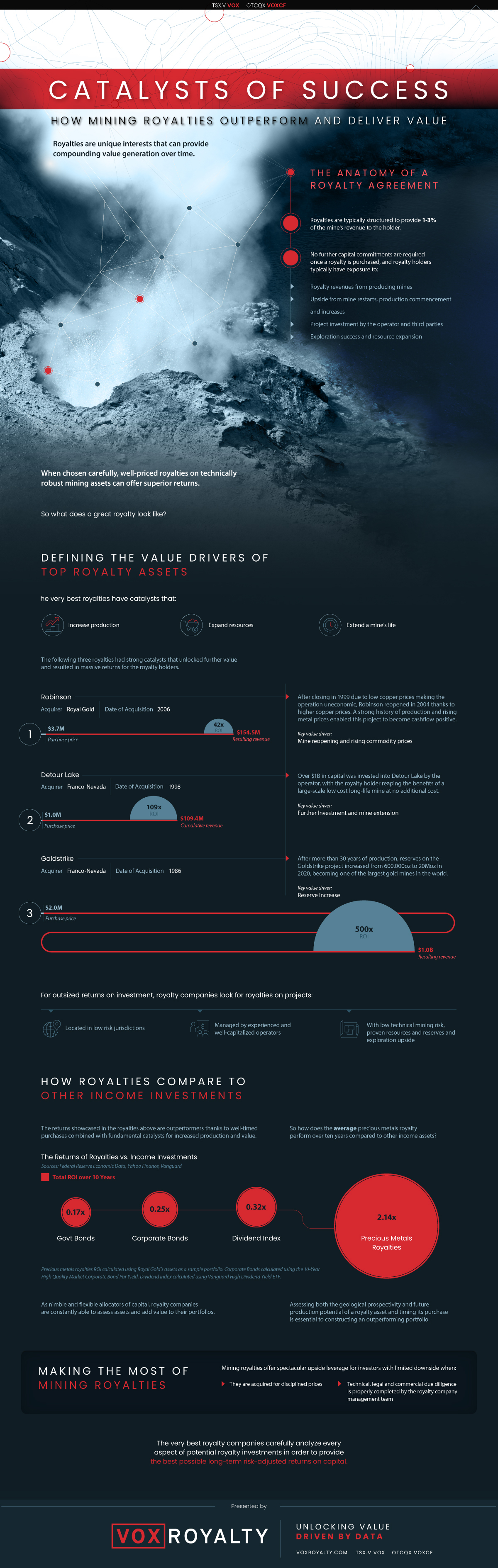

The mining sector is known for its high potential returns, but it hides a unique investment with long-term revenues and high upside potential: precious metals royalties.

Royalties provide holders with a percentage of a mine’s revenue for the life of the project, while also offering exposure to the mine’s increases in production and resource expansion.

This graphic by Visual Capitalist breaks down the catalysts that unlock compounding value for royalty holders, and how precious metals royalties outperform other income investments.

Royalties are interest-bearing agreements that were first created between prospectors and mining companies, so prospectors could receive long-term revenue from the development of their discoveries. Over time, royalty agreements became a funding mechanism allowing mining operators to take up-front funding to develop a mine in exchange for 1-3% of the mine’s lifetime revenue.

Once created, royalties can be bought and sold as income assets, enabling royalty companies to purchase and build a diverse portfolio of income-generating royalties.

It’s worth noting that royalties are calculated from the mine’s top line revenue, meaning royalty holders are not impacted by the mine’s operational or administrative expenses.

Along with the interest on a mine’s revenues, royalties also provide holders with upside exposure to further investment and expansion of the mine, resource expansion of the project, along with mine restarts and life extensions.

Since royalties give holders all the upside of further development, certain catalysts can greatly amplify a royalty’s returns:

Commodity Price Increases: Rising commodity prices can make certain mines more profitable, or profitable enough to resume operations, providing royalty holders with more significant dollar returns.

Mine Extensions: Further investment into a mining project can extend the operating life of a mine, providing royalty holders longer than expected returns.

Reserve Increases: Further discoveries that increase a mine’s reserves and/or resources can extend the life and value of a mining project, compounding returns for royalty holders.

Franco-Nevada’s royalty on the Goldstrike operation is one of the best examples of a value-driving catalyst significantly increasing the ROI of a precious metals royalty.

In 1986, Franco-Nevada purchased a royalty on Goldstrike for $2 million, the same year the project was purchased by Barrick Gold. Goldstrike initially had gold reserves of 600,000 ounces, but in 1989, a discovery increased Goldstrike’s reserves to 20 million ounces, making it one of the world’s largest gold mines.

Today, Goldstrike has produced more than 44.4 million ounces of gold, more than anyone ever expected in 1986, and Franco-Nevada’s royalty has provided exceptional returns on the $2 million purchase price. The royalty has paid Franco-Nevada more than $1 billion in revenue, returning 500x on the initial investment.

When paired with well-timed purchases and catalysts that increase production and revenue, royalties can return double-digit multiples of the initial investments.

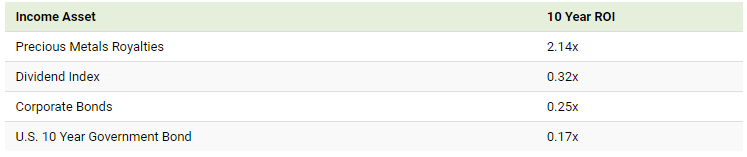

While not every precious metals royalty will provide the outsized returns seen from Goldstrike, an average sample of royalties has generally outperformed other income investments over a 10-year time period.

Although royalties carry larger risks compared to other income assets like bonds and dividend indexes, carefully chosen royalties managed by experienced operators in low-risk jurisdictions can offer long-term returns for investors.

(This article first appeared in the Visual Capitalist)

Comments