{kind=link}

Column: Trump 2.0 won’t reverse Biden’s critical minerals push

Donald Trump has described the Inflation Reduction Act (IRA) as a "green scam" and vowed to repeal it after he returns to the White House in January.

US home prices are surging, increasingly raising worries about inflation. Could gold follow houses? If so, why?

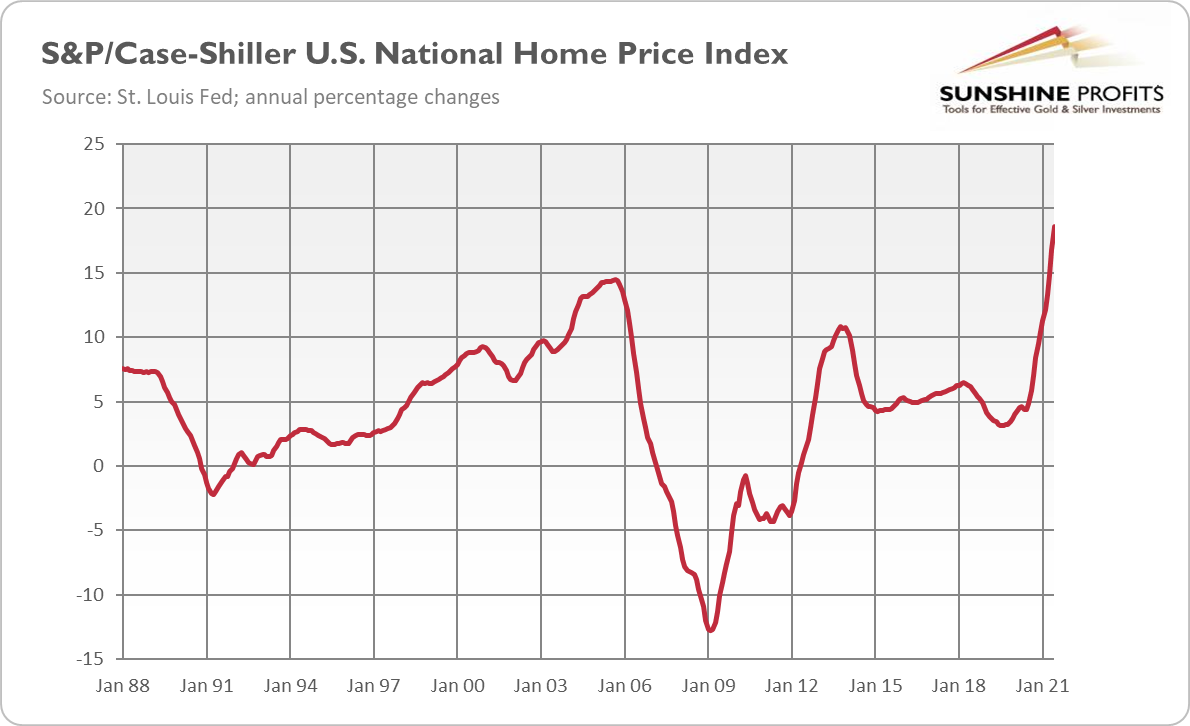

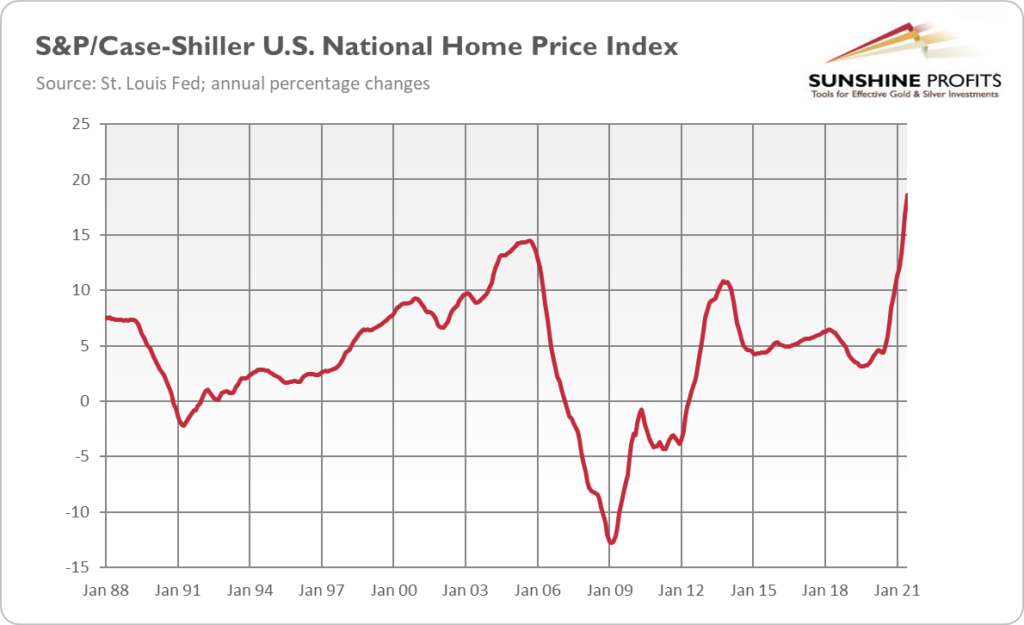

Home price growth in the US has accelerated even further, reaching a new record. The S&P/Case-Shiller U.S. National Home Price Index rose from 255.3 in May to 260.9 in June, boosting the annual percentage gain from 16.8% to 18.1%, as the chart below shows. That’s the largest jump since 1988 when the series began.

Why is it so important? Well, for two reasons. First, such quick growth in home prices increases the risk of a housing bubble and all related economic problems. Please note that home prices are surging now even faster than in the 2000s, which ended in a financial crisis and the Great Recession.

Second, rallying home prices add to the inflationary pressure. What’s important, this year’s impressive home inflation hasn’t shown up in the CPI yet. It will though, as increases in house prices translate into housing inflation, which lifts consumer price measures. This effect may be substantial, given that shelter represents one-third of the overall CPI and about 40% of the core CPI.

Indeed, the recent research from the Dallas Fed, entitled “Surging House Price Expected to Propel Rent Increases, Push Up Inflation”, finds that rising housing prices are usually a leading indicator for rents that are included in the CPI. According to the authors, the correlation between house price growth and rent inflation is the strongest with about an 18-month lag. It means that rent inflation is likely to increase substantially over the next two years, contributing materially to consumer price indexes:

Our forecasting model shows that rent inflation and OER inflation are expected to increase materially in 2022 and 2023. Given their weights in the core PCE price index (which excludes food and energy), rent and OER together are expected to contribute about 0.6 percentage points to 12-month core PCE inflation for 2022 and about 1.2 percentage points for 2023. These forecasts also suggest that rising inflation for rent and OER could push the overall and core PCE inflation rates above 2 percent in 2023, when current supply bottlenecks and labor shortages may have subsided.

So, this research suggests that inflation could stay significantly above the Fed’s target in the coming years and that it might be more persistent than it’s widely believed by the central bankers and Wall Street. In other words, the Fed’s own research suggests that the US central bank might be wrong in claiming that inflation will prove to be temporary – after all, the core inflation is expected to stay above 2%, even when supply-side disruptions resolve.

Importantly, soaring home prices are not the only factor adding to inflation worries. Another one is the fall in consumer confidence in August, partly because of stronger expectations of inflation. According to the Conference Board, consumers’ inflation expectations over the next year increased from 6.6% in July to 6.8% in August.

Last but not least, inflation in the Eurozone has also surged recently. It soared from 2.2% in July to 3% in August, far above expectations and the ECB’s target. The global character of inflation (although it’s stronger in the US) suggests that it’s not caused merely by idiosyncratic factors (as Powell claims), but rather by the combination of supply-side disturbances and demand factors, such as an increase in the money supply entering the economy through consumer spending.

What does it all mean for the gold market? Well, rising home prices imply that inflation will be higher in the future than widely expected. Higher inflation could increase the demand for gold as an inflation hedge. It’s also the best guarantee that real interest rates will stay low, which should support gold. More persistent inflation increases the odds of stagflation, gold’s favorite macroeconomic environment.

However, higher inflation could force the Fed to adopt a more hawkish stance and, for example, accelerate its tapering of quantitative easing, which could exert some downward pressure on gold. Actually, this is what is happening right now. Given high inflation, low bond yields and the US dollar in a sideways trend, gold seems undervalued to many analysts. On the other hand, the narrative about transitory inflation combined with the prospects of the Fed’s tightening cycle could make gold struggle.

Having said that, gold has recently managed to return above $1,800 again, while September is historically a good month for gold. So, we will see – this month’s FOMC meeting could be crucial in determining the yellow metal’s path.

(By Arkadiusz Sieron)

Comments