Home: Battery metals buzz is back as Europe reboots EV sector

(The opinions expressed here are those of the author, Andy Home, a columnist for Reuters.)

The battery metals are back.

Both lithium and cobalt markets spent the last two years absorbing the glut of supply that followed the price boom of 2017-2018. Low prices and turgid trading conditions caused producers collectively to slam the breaks on expansion plans.

Both metals, however, have jumped back to life in 2021, with prices rallying hard in January and February.

The booster has come from a resurgent electric vehicle (EV) sector, which has defied the broader global downturn in automotive sales.

The EV baton has been picked up by Europe, which last year for the first time sold more battery-electric-vehicles (BEV) and plug-in-hybrid electric vehicles (PHEV) than China.

This geographical shift in the green revolution was widely expected but has been given a covid-19 accelerator.

Europe in the driving seat

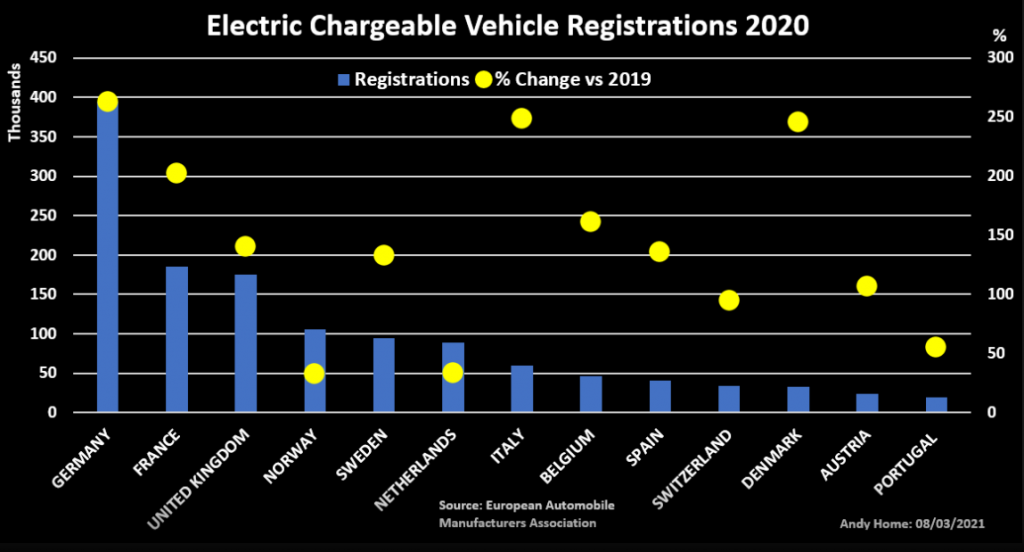

EV registrations in Europe (EU, EFTA and UK) surged to 1.36 million in 2020, from 560,000 in 2019, according to the European Automobile Manufacturers Association (ACEA).

That’s in the context of a 20.6% slump in regional passenger vehicle sales, the second-quarter shutdown of European production lines, including EV lines, and the continuing semiconductor shortage.

EV momentum was already building in Europe as carmarkers rushed to beat this year’s deadline for much tougher emissions targets which come with much higher penalties.

But it’s clear that the pandemic has accelerated demand in the form of generous government subsidies for EVs.

Fastmarkets’ assessment of the lithium carbonate price in China has jumped by 70% since the start of January

Germany is Europe’s largest EV market and one of the fastest-growing with new registrations mushrooming to 395,000 last year from 109,000 in 2019. Much of the acceleration came in the fourth quarter, when registrations jumped by 455% year-on-year to 190,000.

It’s no coincidence that Germany now has one of the most generous EV subsidy schemes in Europe after the government doubled down on the sector as a way of powering back the economy after coronavirus. Government largesse can be as high as 9,000 euros ($10,711.80) for vehicles up to a sales price of 40,000.

The scheme was originally intended to end this year but has been extended to 2025.

Nor is it a coincidence that France, which has an almost equally generous EV programme, is the second-largest market after Germany with registrations more than tripling year-on-year to 75,000 in the last three months of 2020.

The jump in EV registrations is now generating an accelerated roll-out of charging infrastructure.

German charging points have increased by more than 10% in the last three months, spreading the metallic good news to non-battery metals such as copper.

Battery demand

Europe’s EV charge is galvanising demand for battery metals.

The jump in registrations in the second half of 2020 represented a 174% increase in watt-hours of battery capacity deployed, according to analysts at Adamas Intelligence (“State of Charge” Biannual H2 2020).

That in turn translated into a 205% increase in battery cobalt deployed, a 192% increase in battery lithium deployed and a 135% increase in battery nickel deployed versus the second half of 2019, Adamas said.

Globally the amount of lithium deployed in batteries in newly-sold vehicles jumped 96% to 57,300 tonnes of carbonate equivalent over the same period.

China may have been overtaken by Europe last year but its EV sales have also defied broader weakness, rising by 12% in 2020, according to EV-volumes.com.

Chinese demand for lithium is rising particularly fast as more passenger vehicle production switches to lithium-iron-phosphate chemistry, which use more lithium but no nickel or cobalt.

That didn’t stop the amount of nickel and cobalt deployed in global battery production from rising by 69% and 85% respectively in the second half of 2020, according to Adamas.

These massive jumps in deployment don’t include the extra layer of demand that is coming from the build-out of new battery manufacturing plants, all of which need to accumulate processing stocks.

Supply challenge

The strength of the EV sector since the first covid-19 wave has caught out metals producers, who have spent much of the last two years deferring expansions and protecting their bottom lines.

Prices are rising accordingly.

Fastmarkets’ assessment of the lithium carbonate price in China has jumped by 70% since the start of January with signs spot market strength is starting to feed through to lagging-price term contracts.

Standard-grade cobalt metal in Rotterdam, meanwhile, has risen by 30%, which is remarkable given much of the demand for cobalt in this form comes from the currently bombed-out air and aerospace sectors.

Nickel, the third player in this battery trio, was also in full party swing, hitting a seven-year high of $20,110 per tonne last month before Chinese steel giant Tsingshan’s announcement it is pursuing a new processing path to battery-grade nickel.

Nickel’s investment case is based both on the expected boom in demand from batteries and on what form of the metal is needed for precursor materials. Tsingshan’s plans change the latter chemical calculations but not the underlying need for more nickel.

These early-year price rallies may herald the start of the next major battery metals boom.

The lithium supply chain doesn’t like being described in commodity market terms, but price-wise the market has conformed to a classic commodity boom-bust cycle over the last five years.

High prices incentivised too much supply to come onstream too soon, causing a glut of excess material and a price crash.

The next turn of the wheel is normally characterised by producers rushing but failing to turn on the taps sufficiently to meet a new step-change in usage.

Battery metal bulls have long argued that producers were failing to appreciate the scale of the coming demand wave for their products. Two years of low prices have only compounded the supply chain challenges.

We’re about to find out if they are right because, with Europe now joining China in the EV revolution, demand is only going to go one way.

($1 = 0.8402 euros)

(Editing by Susan Fenton)

More News

Column: Europe’s future metals strategy hindered by current crisis

Chinese over-capacity and high energy prices have accelerated the long-term decline of European steel and aluminum production.

March 29, 2025 | 02:25 pm

Anglo starts talks with banks on possible De Beers IPO

Anglo is pursuing a dual-track process in its effort to exit De Beers by trying to find a buyer for the struggling business.

March 28, 2025 | 12:19 pm

{{ commodity.name }}

{{ post.title }}

{{ post.excerpt }}

{{ post.date }}

Comments