Mining’s old guard needs strong medicine

A new report details subpar investor returns in the mining industry over the last decade, particularly big cap diversified companies which have not adapted to new realities.

After years in the shadow of the US shale boom, the Canadian oil sands are emerging from 2020’s historic market crash with a slew of upbeat outlooks from Wall Street equity analysts.

Morgan Stanley and Goldman Sachs Group are the latest firms to point out the industry’s ability to generate healthy cash flow next year as a reason to buy stocks like Suncor Energy, Canadian Natural Resources and MEG Energy. That follows similar reports from BofA Securities and BMO Capital Markets.

“With improved cost structures and increased propensity to be capital disciplined, Canadian producers are emerging from the downturn stronger, with greater ability to generate free cash flow,” Morgan Stanley analysts Benny Wong and Adam J. Gray said in a note Friday.

Among tailwinds improving the prospects for the beleaguered heavy-crude producers of northern Alberta are declining competition from Mexico and the start of construction of three pipelines, following years of insufficient shipping capacity.

Steady output from their mines means that oil sands producers are able to keep revenue coming for decades without too much investment, while the short life span of shale wells forces US explorers to constantly burn cash just to keep up production.

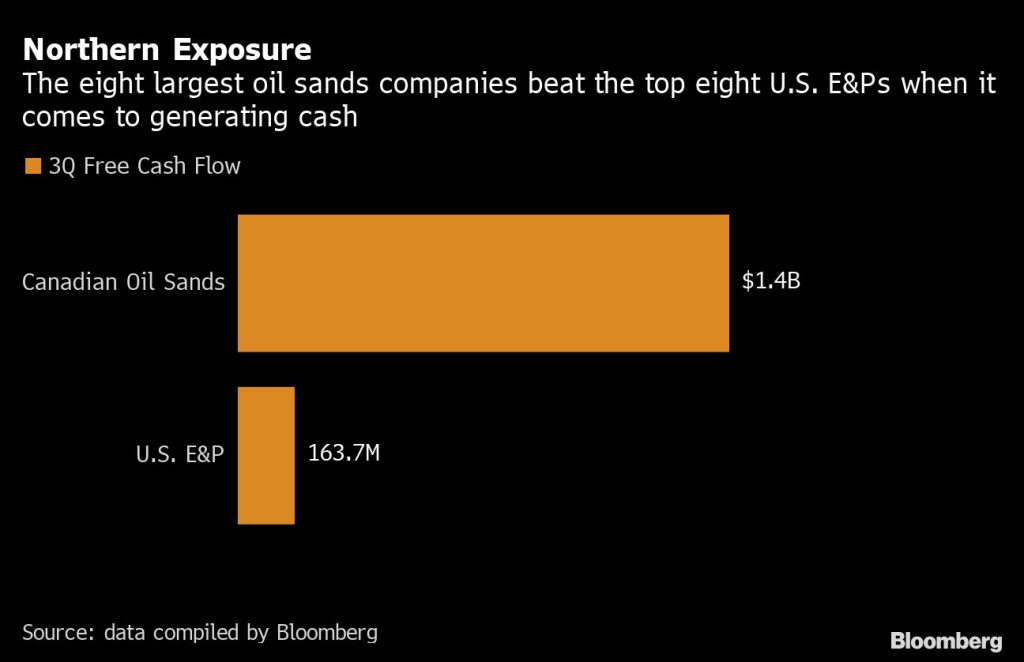

The eight largest oil-sands producers by market value posted a combined free cash flow of $1.4-billion for the third quarter, compared with $163.7-million from the top eight US exploration and production companies, according to data compiled by Bloomberg.

Among tailwinds improving the prospects for the beleaguered heavy-crude producers of northern Alberta are declining competition from Mexico and the start of construction of three pipelines

Exports of Mexico’s flagship Maya heavy crude grade are forecast to decline by 70% in the next three years, helping narrow Western Canadian Select oil’s discount to New York-traded futures to $5/bbl to $7/bbl next year, BMO Capital Markets said in October. The price gap is currently at about $12/bbl.

Demand for WCS has also risen after OPEC countries cut output of their heavier, higher-sulfur grades similar to those from the oil sands. Canadian oil will continue to be “well supported” in 2021, according to Goldman.

To be sure, oil sands companies also face potential headwinds. Increasing numbers of banks and investors have shunned the industry because concerns over high carbon emissions. The pipelines that are under construction still face potential court delays, as well as political opposition.

Adam Waterous, CEO of Calgary-based private equity firm WEF GP, is among investors expecting more profitability from the oil sands than shale. He estimates U.S. crude production will fall by about 2.5-million barrels a day in the next year as oil prices are still too low to earn attractive returns.

WEF controls two Canadian oil producers including Cona Resources, which bought Pengrowth Energy in January for about C$790-million ($620 million), including debt, and is currently embroiled in an attempted hostile takeover of Osum Oil Sands Corp.

“The best days of the US oil industry are definitely behind us,” he said. “We are very bullish on Canadian oil sands where others are not.”

(By Robert Tuttle and Michael Bellusci, with assistance from Danielle Bochove)

Comments