Copper output from Codelco jumps 17% in November

Cochilco data showed that Codelco production totaled 133,600 metric tons in November.

(The opinions expressed here are those of the author, Clara Ferreira Marques, a columnist for Bloomberg)

Copper has touched $7,000 per metric tonne on the London Metal Exchange, having climbed roughly 60% from a late-March nadir. The industrial metal is trading at levels unseen since 2018 despite a surge in coronavirus infections in Europe and beyond, stockpiles rising off recent lows, and expectations of a surplus in 2021. The reason is China, which is dominating the 24-million-tonnes per year market like never before thanks to a recovery that is outpacing other economies.

The metal’s rebound from four-year lows in March mirrors the rally in that other gravity-defying asset class, the FANG-powered U.S. stock market. Copper’s rally has exceeded expectations, given that the most pessimistic forecasts for pandemic-related supply disruptions haven’t been borne out. Peru’s production fell in August from a month earlier, hit by worker shortages, but output in Chile, the world’s top exporter, increased. BHP Group-operated Escondida, the Chilean copper mine that’s the world’s largest, avoided a strike last week, even if workers at Lundin Mining Corp.’s far smaller Candelaria downed tools in the country.

A price consistently above $6,000 is also more likely to encourage companies to approve new projects

China’s industrial production gained momentum to rise a forecast-beating 6.9% in September from a year earlier; excavator demand has jumped, along with car sales. Fiscal stimulus, an imminent five-year plan that will boost clean energy investments, and an expansionary monetary policy are all supporting the recovery. Meanwhile, an appreciating yuan has increased consumers’ purchasing power.

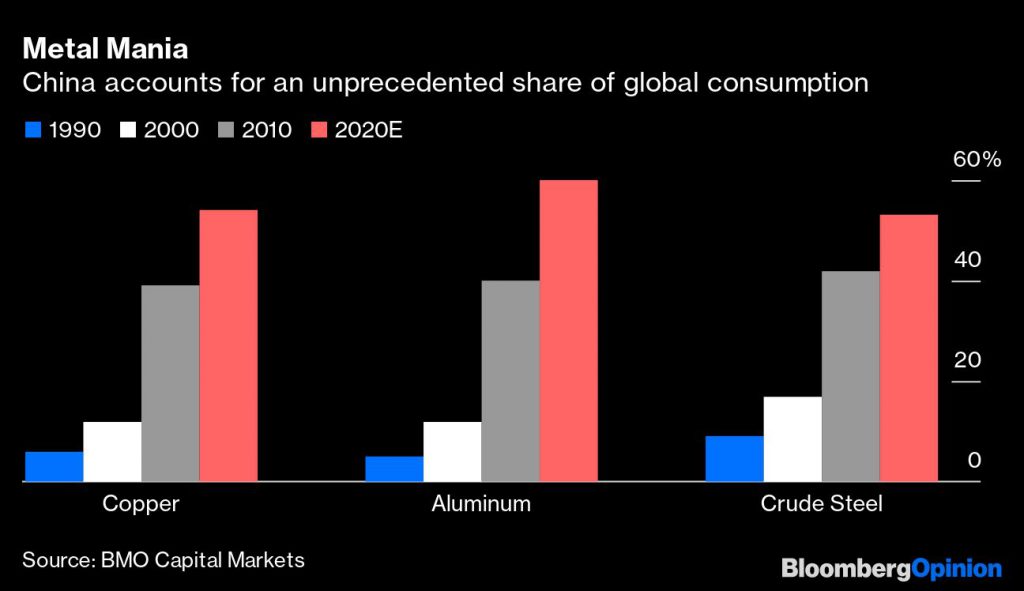

China’s influence is hardly new — or surprising, given it’s the only major economy the International Monetary Fund expects to see expand in 2020. In industrial metals, though, this year has marked a significant increase in its clout. The country now accounts for more than 50% of demand in nickel, steel, copper and aluminum, analysts at BMO Capital Markets say — a level that only Japan has ever come near, and China’s North Asian neighbor peaked at less than 15% of global volumes.

Indeed, China’s dynamics have been enough to put copper back on a rising path after a short-lived drop earlier this month, when U.S. President Donald Trump was diagnosed with coronavirus. That’s partly because inventories are still close to historic lows, making the price more likely to swing on supply hiccups, like Lundin’s disruption. But it also hints at a market watching the macroeconomic signals rather than output specifics, and expecting China, which has already imported more copper than it did in 2019, to keep on spending its way through post-pandemic convalescence.

The five-year plan is set to include ample sums for electrification, clean energy and electric cars, which use four times as much of the metal as a standard vehicle. They are already forecast to make up the bulk of copper growth over the next decade or so, along with charging infrastructure. Then there are the aggressive decarbonization ambitions. All of that, and hopes of a spending spike in the fourth quarter from the likes of State Grid Corp. of China, explains the persistent net long positions among money managers in CME copper, up again, according to the latest Commitments of Traders Report. There are fewer bears out there, too, compared to much of early 2020 and 2019.

The bigger question is whether that is enough to hold the metal at or close to current levels, especially if China’s rush begins to fade before the rest of the world recovers, or before Beijing’s five-year plan and its green ambitions rev up. A price consistently above $6,000 is also more likely to encourage companies to approve new projects, as they did after 2017, analysts at CRU Group pointed out in a September study. Cashed-up diversified miners and even iron ore-focused diggers may pile into copper acquisitions with greater enthusiasm, too.

Still, supply is unlikely to be the immediate cause if the rally does stumble. The reality is that even at lower prices, miners have been eyeing up deals for some time, given the metal’s gleaming green-economy prospects. Unfortunately, theory is easier than practice. Anyone needing a reminder could do worse than consider BHP’s Olympic Dam copper operation in Australia, where ambitions and scale have shrunk again this week. It’s a far cry from a vision that once included the world’s largest open pit.

Comments

Jacob Willoughby

The title of this article is one of the dumbest statements I’ve seen all year.