Iron ore weakness to continue into 2025 and beyond, says Fitch Solutions’ BMI

Looking beyond 2024-2025, BMI analysts maintained their view that iron ore prices will likely follow a multi-year downtrend.

Amid the worries about the coronavirus and its impact on the global economy, the US yield curve has briefly inverted again. Recession, anyone? And what exactly does the inversion imply for the gold market?

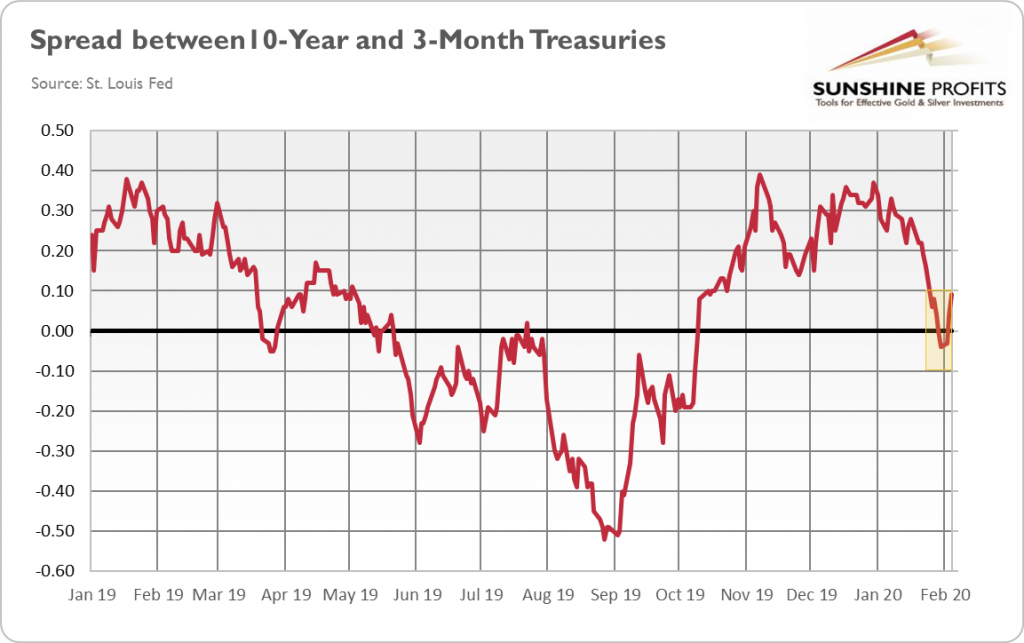

Ooops, it happened again – the yield curve has inverted! Please take a look at the chart below. It shows that at the turn of January and February, the spread between 10-year and 3-month Treasuries has dived below zero once again. It stayed below zero only for a couple of days before moving back into the positive territory. The inversion was shallow as the level of the spread did not plunge below minus 0.4.

However, the fact that the yield curve has inverted again after the October 2019 normalization, is of great importance. It shows that the underlying forces behind all the 2019 inversions are still in force. It shows that the Fed’s easing of monetary policy did not heal the economy.

It should be clear that the Fed just postponed the inevitable. We mean here, of course, recession

The US central bank cut interest rates three times in 2019, partially because of the worries about the inversion of the yield curve. Initially, it seemed that these cuts helped, as the yield curve reinverted in October and stabilized in the positive territory for a few months. But now it should be clear that the Fed just postponed the inevitable. We mean here, of course, recession.

We still do not know when exactly the next economic crisis comes – other indicators suggest the US economy remains strong – but the latest inversion of the yield curve shows that the recessionary fears are still justified, despite the temporary calming down. But, as we all know, it’s always calm before the storm.

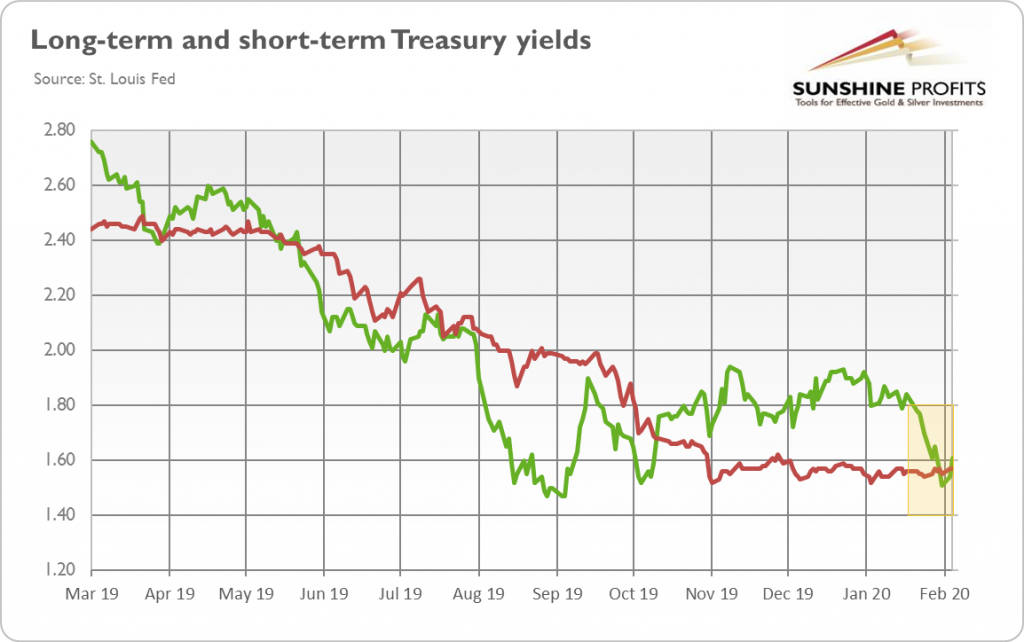

Now, let’s dig deeper into the cause behind the recent inversion of the yield curve. Please take a look at the chart below. As you can see, the yield curve has inverted this time not because of the rise in the short-term interest rates, but because of the drop in the long-term bond yields.

It show that investors worry about the prospects of the global growth amid the coronavirus outbreak. These concerns about the negative impact of the virus on the world’s trade and pace of economic growth pushed investors from the stock market into safe-haven assets such as the long-term government bonds.

After all, the impact on the global economy from the SARS epidemic reached up to $40 billion, according to this research, but as coronavirus is more contagious, its economic costs may be higher.

So, although the short-term interest rates did not spike, which could tighten financial conditions and trigger recession, the inversion of the yield curve is still positive for the gold prices. Investors expect that the growth will slow down or/and that the Fed will cut the federal funds rate again later this year. Indeed, traders bet that the US central bank will deliver one cut in July, but they have also increased their bets on two cuts.

When the spread between 10-year and 3-month Treasuries bottomed out, the price of gold jumped above $1,580. And the current fears about coronavirus may support it in the short-term. However, as we wrote on Monday, fears about previous virus outbreaks were overblown in hindsight. Therefore, the current anxiety may be only temporary.

The yield curve has already reinverted (but another inversion is probable) while the stock market shook off the fears and rebounded. Hence, don’t necessarily expect gold prices skyrocketing. However, the yellow metal performed greatly in 2019 due to the recessionary fears. So, if they settle in again on a more permanent basis, gold bulls would get an ally.

(By Arkadiusz Sieroń)

Comments