Ivanhoe’s Kipushi zinc mine in the DRC officially reopens

The restart marked exactly a century since the mine first went into production.

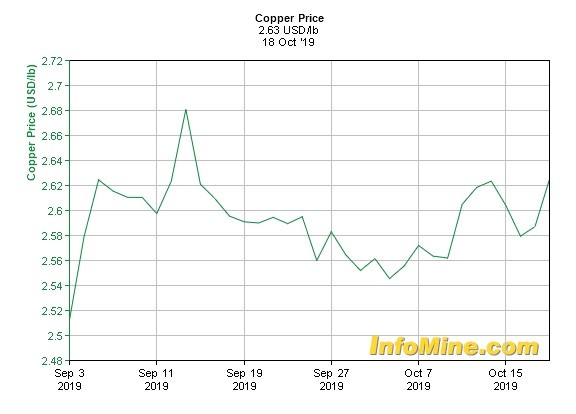

Copper prices surged to a one-month high on Monday, on potential supply disruptions owing to violent protests in Chile over a proposed law, now suspended, that would raise the prices of transit tickets.

At least 11 people have died, according to the mayor of Santiago, the capital, including eight on Sunday, when protesters set fire to supermarkets, buses and subway entrances; looting and vandalism took place on streets and in storefronts.

Benchmark copper on the London Metal Exchange was up 0.4% to $2.64 a pound ($5,828/tonne), having touched $5,868.50 earlier in the trading session.

Metal traders say optimism over the trade war between the US and China also played a role in bumping the bellwether metal to fresh highs. President Donald Trump said trade negotiations in Washington are going well, adding to his hopeful comments last week that the first phase of a trade deal, announced earlier in October, will be signed by mid-November. Possible olive branches may include dropping 15% tariffs on imports of Chinese cell phones and computers. The Trump administration has already held off raising tariffs on another $250 billion worth of Chinese goods to 30% from 25%.

Meanwhile in Chile, at least 180 people have been arrested, as thousands of people turn out to show their frustration not only with rising transportation costs, but widening inequality and what some see as the government’s attack on the poor.

“This is not a simple protest over the rise of metro fares, this is an outpouring for years of oppression that have hit mainly the poorest,” a university student protester told Reuters on Sunday. “The illusion of a model Chile is over. Low wages, lack of healthcare and bad pensions have made people tired.”

A state of emergency was declared and armed forces mobilized on the streets of Santiago for the first time in nearly 30 years. Chile is considered among the most stable and business-friendly Latin American nations. The country is the world’s largest producer of copper and has the most lithium reserves.

As for the civil unrest spreading to the mining industry, the mining minister told the press that operations have not yet been affected, however trade unions are calling for work stoppages. Employees at the world’s largest copper mine, Escondida, reportedly planned to stage a 24-hour strike on Tuesday, in solidarity with other protests taking place across the country. A general strike including mine workers is being planned for Wednesday, Oct. 23.

Temporary production outages of course are nothing new to the copper industry, which typically sees millions of tonnes of the red metal left in the ground as workers down tools seeking higher wages and benefits, or mines declare ‘force majeure’ usually owing to poor weather.

Analysts have apparently ‘penciled in’ disruptions of 1.2 million tonnes this year that will be stripped from the copper market, likely resulting in higher prices.

That number could rise much higher, if not this year, in future, due to the location of un-developed copper orebodies. A recent study at the University of Queensland found that a majority of 600 copper, iron and bauxite orebodies examined by the Sustainable Minerals Institute, are in places vulnerable to environmental, social and governance (ESG) challenges.

Each of the orebodies was judged against eight risks: waste, water, biodiversity, land uses, indigenous peoples, social vulnerability, political fragility, and approval and permitting. The study found “The majority of the 296 copper orebodies, 324 iron orebodies and 50 bauxite orebodies we examined are in complex ESG contexts which could either prevent, delay or disrupt mining operations,” and that 65% are in regions subject to medium to extremely high risk of water scarcity.

The copper market has been especially volatile this year. On June 7 copper by the tonne blew past $7,300 for a four-year high, but 10 weeks later, prices were languishing under $6,000.

Lower prices are mostly due to the potential for demand destruction in China, which accounts for half of global copper consumption of around 24 million tonnes. Market observers are increasingly concerned that a lack of progress on trade talks will lead to less copper shipments to China and weaker industrial performance.

According to the IMF, China’s GDP will slow to 5.8% in 2020, versus 6.1% in 2019 and 6.6% in 2018. A country not growing as fast will demand fewer metals.

A lack of progress on trade talks points to a deteriorating demand picture, but the real action in the copper market is happening with respect to supply.

As we wrote in The coming copper crunch, by 2035, without major new mines up and running to replace the ore that is being depleted from existing copper mines, we are looking at a 15-million-tonne supply deficit by 2035.

Supply is getting tighter owing to events in South America, where most of the world’s copper is mined, and Indonesia. In the first half of the year, global copper output fell 1.4% to almost 10 million tonnes. A report from the International Copper Study Group shows Chile’s production dropping 2.5% due to heavy rains.

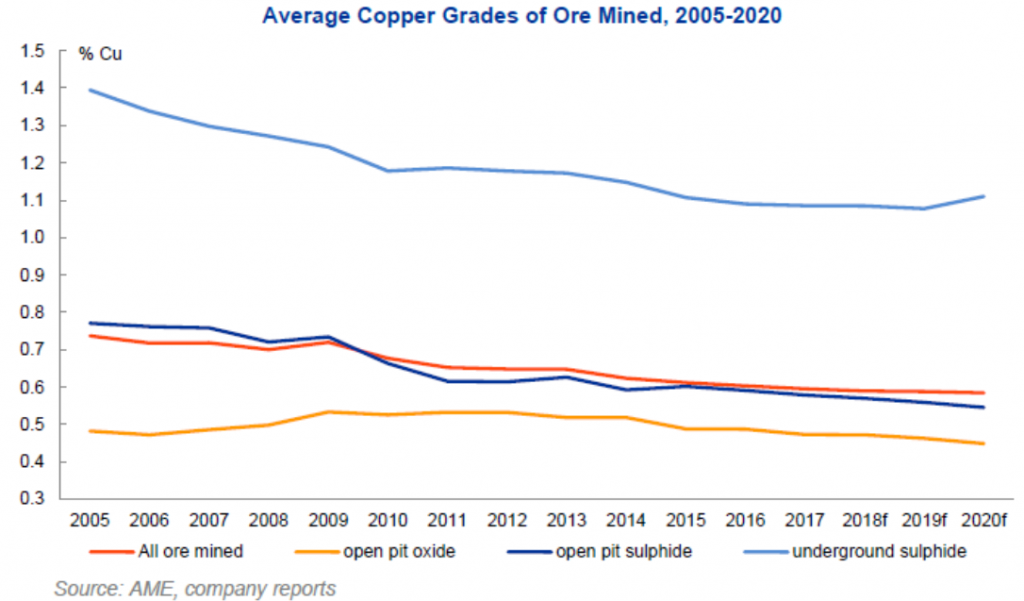

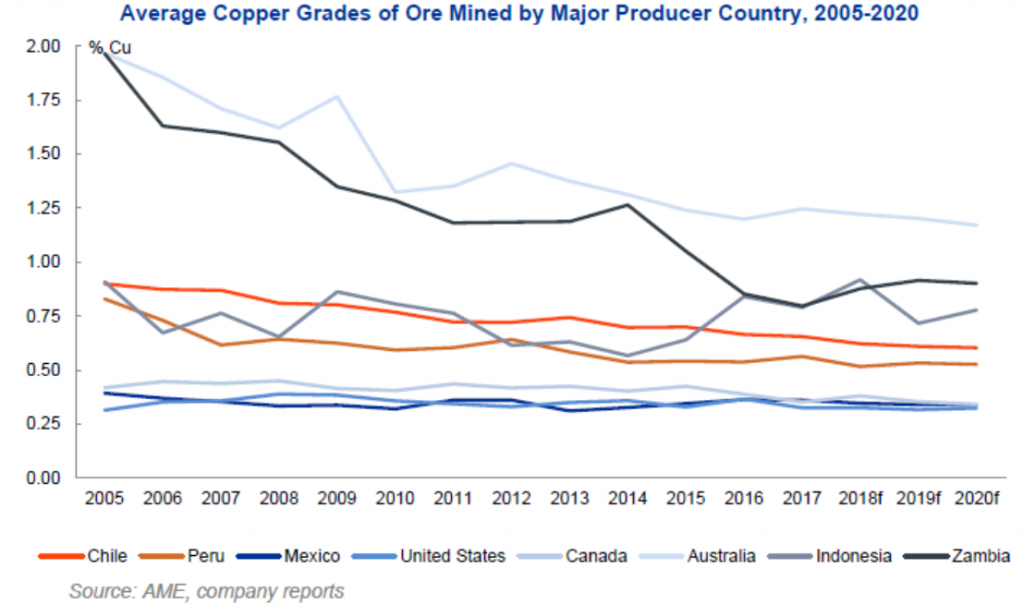

Poor grades also hampered output. Copper grades have declined about 25% in Chile in the last decade – highlighting the urgent need for grassroots exploration to arrest the trend.

Meanwhile Indonesia’s copper concentrate production crashed 55% in the first half, as the Grasberg mine transitions to underground block caving and the Batu Hijau mine moves to Phase 7, leaving an HI global refined copper deficit of around 220,000 tonnes.

We can see this deficit beginning to be reflected in the supply of stockpiled copper. As the chart below shows, stocks of copper in LME warehouses began drifting downwards in August, and now sit at about 275,000 tonnes. If the market sees more disruptions it may have to draw these stocks down even further, resulting in an upward price correction. Current ten days of warehoused Cu supply doesn’t seem like much of a safety net.

“Deficits are going to be larger than people were expecting even two months ago,” a fund manager focused on metals told Reuters, in May. “You can see it already in the physical market.”

Miners are having to go further afield and dig deeper to find copper at the grades needed to economically produce copper products for end users.

Delving deeper into what is causing this deficit in the copper market, we find a number of trends, starting with lower output from some of the world’s largest copper producers.

Chilean state-owned Codelco produced 1.678 million tonnes in 2018, 3.3% less than in 2017.

The modest production cut however wasn’t enough to prevent Codelco from splashing red ink. Experiencing lower copper grades and prices, and rising costs at its aging mines, the world’s largest copper mining company reported a pre-tax profit in 2018 of US$2.002 billion, versus $2.885 billion in 2017. Codelco also wrote off nearly $400 million in deteriorating assets, for a steep 44.3% drop in pre-tax profits.

Codelco’s large Chuquicamata mine is expected to see a 40% fall in production over the next two years. A $5 billion expansion, moving from open-pit to underground, will take five years to reach full output of 300,000 tonnes per annum. Production will fall from an expected 459,000 tonnes in 2019 to 182,000t in 2021.

Exports from BHP’s Escondida, the world’s second largest copper mine, are expected to drop this year by 85% due to operations moving from open-pit to underground. That’s a dramatic fall from 1.8 million tonnes in 2018 to just 200,000 in 2019. The Chilean mega-mine is expected to take until 2022 to re-gain full production.

BHP said last fall that it was able to maintain 2019 full-year guidance, through a combined 3% decrease in production at its copper-gold-uranium Olympic Dam mine in Australia and its Spence mine in Chile. Because of a fire at its electro-winning plant, production guidance for Spence was reduced to a range of 160,000-175,000-tonnes, compared to the earlier guidance of 185-200,000t. An outage at Olympic Dam’s acid plant cut production by 21% to 33,000t.

A two-month strike in Peru at MMG’s Las Bambas mine meant a 15% drop in second-quarter production. Anti-mining protests in Peru this summer blocked some $400 million in copper exports from the country’s four top mines – Freeport-McMoran’s Cerro Verde, Las Bambas, Glencore’s Antapaccay and HudBay Minerals’ Constancia.

Over in Indonesia, copper concentrate exports from Grasberg, the world’s second biggest copper mine, are expected to plunge dramatically while operations shift from open pit to underground. Production will likely fall from 1.2 million tonnes of copper concentrate last year to just 200,000t in 2019; concentrate exports are expected to be half. The gigantic copper-gold mine recently underwent a change of ownership, when the Indonesian government took over from Freeport McMoran’s Indonesian unit, upon closing the nearly $4 billion deal.

Glencore reported a second-quarter fall in copper production due to problems at its copper business in Africa, leading to a 1% nick in its full-year guidance. While zinc and cobalt production rose in Q2, the Anglo-Swiss trading company said it only produced 342,000 tonnes of red metal versus 350,800t in the second quarter of 2018. The lesser output was owing to issues at its Katanga mine in the DRC and the Mopani mine’s smelter in Zambia, Marketwatch said.

There have been stoppages at several smelters in Zambia, amid a dispute between the government and mining companies over taxes. Changes to the tax regime will cost Zambia about 100,000 tonnes of output this year compared to the 860,000 tonnes mined in 2018. A drought in the central African country may impact copper production, since most mines get their power from hydroelectric dams.

Resource nationalism has also reared its head in neighbouring DRC. The Chinese operator of the country’s largest copper producer, Tenke Fungurume, told employees in August that it is having a hard time making money due to low copper and cobalt prices. Bloomberg notes China Molybdenum’s warning to employees comes as Congo’s entire extractive industry is under pressure after a revised mining code was signed into law in March last year, raising taxes and canceling a clause that would have protected producing mines against fiscal changes for another decade. The government then imposed a 10% royalty tax on cobalt producers eight months later.

Another example of copper output declining is an expected delay at Mongolia’s Oyu Tolgoi mine going underground. Difficult ground conditions are cited as the reason the expansion could be delayed up to 30 months.

With so much metal staying in the ground, supply lagged demand by 155,000 tonnes in the first four months of the year, according to the International Copper Study Group, more than double the 64,000-tonne shortfall in the same period of 2018. The ICSG expects a 169,000-tonne deficit by the end of this year.

“The average grade of copper ore mined has declined by 1.8% per year over the past 12 years to 0.59% in 2017. The fall is due to declining grades at some of the largest, long-life mines and the development of new low-grade mines. The declining grade trend will continue because of the same two factors.” AME Research, ‘Declining copper ore grades.’

Copper ore grades at Chilean mines are on the decline.

Cochilco, the Chilean Copper Commission, recognized falling grades in a report, noting production from existing mines will decline 19%, but says the drop will be offset by new mines and expansions.

These include:

Critics say these expansions are unrealistic and unlikely to come to fruition anytime soon. Los Bronces and Collahuasi are already high-grading (processing higher-grade ore) from their mines and can’t do that anymore once that ore runs out because they are working highly-disseminated porphyry deposits (ie. no high-grade veins). Escondida is expected to see grades fall 15% until 2022. The Quebrada Blanca expansion won’t be online until 2024, and that’s if Teck can find a partner to kick in at least $2.5 billion.

Chile also has serious water and power issues that are likely to crimp higher production.

We have reported on the fight over water between SQM and Albemarle, and the Chilean government’s efforts to restrict water rights, in the Salar de Atacama – the center of Chile’s lithium production. With most of Chile’s mining taking place in the north, copper mines are also affected by water restrictions.

Antofagasta and BHP are among the mining companies hit by a ban on new permits to extract water from the southern portion of the salar’s watershed, which supplies BHP’s Escondida, the world’s largest copper mine, and Antofagasta’s Zaldivar Mine.

It’s not the first time the Chilean government has moved against miners with respect to challenges over water. In 2016 its environmental regulator, SMA, shut down the Maricunga gold mine operated by Kinross Gold, over environmental concerns. Kinross was ordered to stop withdrawing water from local wells used to feed the operation. Shuttering the mine meant laying off 300 workers.

Speaking of workers, employees at South American copper mines are not shy about walking picket lines in pursuit of higher pay. Frequent strikes are a common reason for copper mining companies having to slash their production guidance.

This past summer a two-week-long strike at the Chuquicamata mine in northern Chile was forecast to cost Codelco $50 million in lost output and wipe 10,000 tonnes from the copper market.

Summing up the copper market, supply-side, we know that, assuming predictions come true, this year will see a copper deficit of around 169,000 tonnes. Supply is tightening up due to continuing labor unrest in South America, output cuts from major copper miners, and higher costs resulting from lower ore grades and some of the world’s largest copper mines shifting their operations from open pit to underground. In Africa we are seeing tax grabs from Zambia and the DRC resulting in lower production from foreign-based mining companies.

There are however a few places where mining firms can find some hope in the building of new mines; diamonds in the rough of a tough copper market where retaining output goals can be a real challenge, due to all the reasons discussed.

New supply is concentrated in just five mines – Chile’s Escondida Spence and Quebrada Blanca, Cobre Panama, and Kamoto in the DRC. And while these mines are expected to account for 80% of base-case output increases between 2018 and 2022, their profitability depends on the copper price staying above $5,000 a tonne, according to analysts at Bank of America Merrill Lynch, via the Financial Times.

That means exploration for new copper deposits that are large and high-grade enough to be economically brought into production is of primary importance to the mining industry. Especially considering that the demand side of the equation, despite the current lull in China, is only going to get stronger.

Three of the world’s largest investment banks, Morgan Stanley, Citi and Goldman Sachs, have all placed bullish bets on copper this year; Morgan Stanley expects the price to rocket 14% as supply tightens. Citi is predicting a demand surge from China in the second half, as construction completions requiring copper catch up with housing starts.

A recent report from Wood Mackenzie states that copper consumption is expected to grow 250% by 2030, due to the implementation of 20 million electric vehicle charging points.

The trouble is, with all the main copper-producing countries having problems bringing their product to market, where will new supply come from to meet emerging demand?

One of the most interesting places to look for new copper deposits is in a country better known for gold and coal: Colombia. A 2016 peace agreement between the government and the largest Marxist rebel group has the South American country looking to explore for minerals in previously inaccessible areas.

The first thing to notice about Colombia’s copper potential is the fact that the Andes mountain range that hosts some of the largest porphyry copper deposits in world, runs right through Colombia. Much of the Colombian part of this immense porphyry belt is hugely underexplored.

And while there is currently just one copper mine in operation, in the northwestern department (state) of Chocó, run by Canada’s Atico Mining producing 10,000 tons a year, the government is hoping to diversify from gold, oil and coal, into the red metal.

Recent geological studies found copper mineralization in not only Chocó but Antioquia, Córdoba, Cesar, La Guajira and Nariño.

Major gold company AngloGold Ashanti (Z:AU), Cordoba Minerals, Max Resource and privately held Minera Cobre, partially owned by First Quantum Minerals (Q:FQVLF), are among the companies exploring for copper in Colombia.

Cordoba Minerals (TSX.V:CDB) for example is developing its fully-owned San Matias copper-gold project which includes the advanced-stage Alacran deposit in Córdoba. Cordoba acquired the deposit from an exploration company led by mining pioneer Robert Friedland, who now owns around 70% of the company.

Max Resource (TSX-V:MRX) has two copper targets it’s exploring in Colombia – Cesar and La Guajira. The company also holds exploration licenses in the Chocó and North Chocó areas.

Libero Copper and Gold (TSX.V:LBC) is developing Mocoa, a copper property on the border with Ecuador. Historical exploration includes geological mapping, surface sampling, ground geophysics, 31 diamond drill holes and preliminary metallurgical testwork.

“We want to move from a copper exploration stage to a country with proven reserves and to bring investors with assembly and production projects,” said Silvana Habib, president of the Colombian Mining Agency, in a July interview.

She noted the government has moved forward on mining-friendly policies that include faster licensing procedures and more transparency in awarding titles. A recent court ruling decided that popular referendums cannot ban mining and oil exploration projects, adding more investor certainty.

There are few copper exploration companies with projects that have the scale and grades to interest a major. As is the case with gold exploration, most if not all of the low-hanging copper fruit has been picked. The countries with the best deposits are either being mined out – witness what’s happening in Chile and Indonesia – or run by resource nationalists, whereby foreign companies are finding their welcome comes at a considerably higher price.

Colombia still has an unexplored copper belt and a government that seems willing to diversify into exploring/ developing it with few impediments. In my opinion, it’s definitely worth a look.

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

AOTH/Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified. AOTH/Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of AOTH/Richard Mills only and are subject to change without notice. AOTH/Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, AOTH/Richard Mills assumes no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this AOTH/Richard Mills Report.

AOTH/Richard Mills is not a registered broker/financial advisor and does not hold any licenses. These are solely personal thoughts and opinions about finance and/or investments – no information posted on this site is to be considered investment advice or a recommendation to do anything involving finance or money aside from performing your own due diligence and consulting with your personal registered broker/financial advisor. You agree that by reading AOTH/Richard Mills articles, you are acting at your OWN RISK. In no event should AOTH/Richard Mills liable for any direct or indirect trading losses caused by any information contained in AOTH/Richard Mills articles. Information in AOTH/Richard Mills articles is not an offer to sell or a solicitation of an offer to buy any security. AOTH/Richard Mills is not suggesting the transacting of any financial instruments but does suggest consulting your own registered broker/financial advisor with regards to any such transactions.

Richard owns shares of Max Resources Corp. (TSX.V:MXR) and MXR is an advertiser on his site aheadoftheherd.com

Please read the entire Disclaimer carefully before you use this website or

read the newsletter. If you do not agree to all the AOTH/Richard

Mills Disclaimer, do not access/read

this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard

Mills website/newsletter/article, and whether or not you actually

read this Disclaimer, you are deemed to have accepted it.

Comments