Why gold ain’t goin’ anywhere anytime soon

The price of gold has been range-bound from the low $1200s to the upper $1000s per ounce since early February of 2015.

There is one simple reason for the low volatility and lack of significant price movement for the most precious metal over the past eight months: the strength of the US dollar. In a series of musings late last fall and winter, I discussed correlations between the dollar and hard commodities.

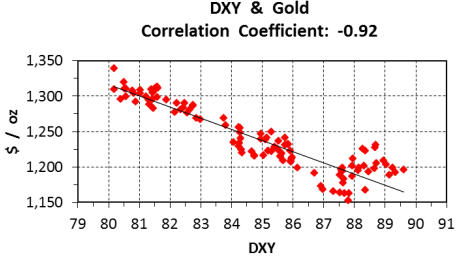

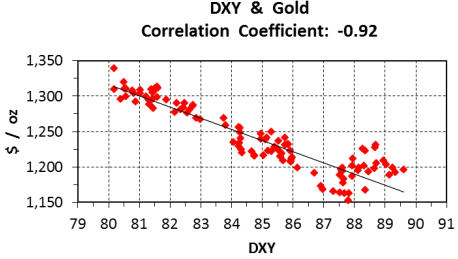

There was an extremely strong negative correlation between the US dollar index (DXY) and gold from July 11, 2014, when the dollar began its concerted march above 80.0 to December 18 when it closed at 89.6.

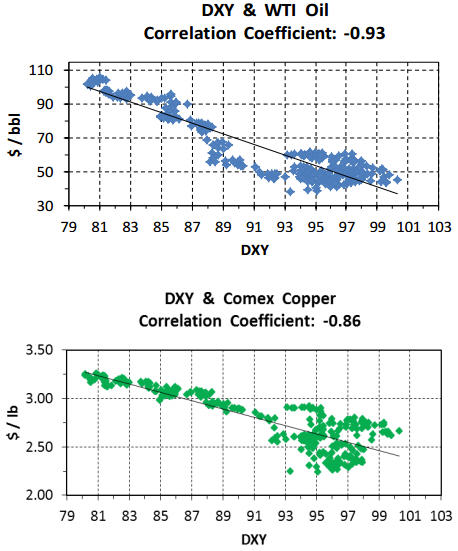

A negative correlation with DXY is the usual paradigm for gold and the other two major resource commodities traded on world exchanges, oil and copper. This is because trades are quoted and settled in US$, both as physical goods for delivery and as speculative derivatives. However, from December 19 to February 13, an unusual positive correlation existed for gold and DXY:

On the other hand, both oil and copper have continued to exhibit strong negative correlation with DXY since that pivotal day last July. This has occurred despite an increasingly range-bound dollar for the past few months:

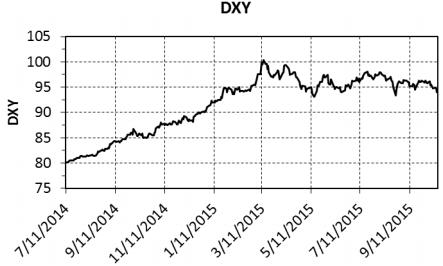

After the dollar index rose exponentially from 80 to above 100 in eight months, it quickly topped, fell back, and has been range-bound between 94 and 98 since mid-April:

After a nearly 20% rise over the past 15 months, I see little evidence for a significant upside or downside swing for the US dollar in the short term. Reasons include:

- US economic growth will continue to be tepid and the Fed seems unwilling to raise interest rates even a quarter per cent.

- The world’s economy is being fueled by fiat currency devaluations, zero interest rates, and an ever-increasing debt load, now 40% higher than during the financial crisis of 2008. Current safe

havens are the $US and its treasury bonds. - Currency weakness will continue for those whose export revenues are commodities-driven (e.g., Aussie and Canadian dollars, Chilean peso, and South African rand).

- The Euro will remain compromised as long as Germany serially props up a consistently expanding contingent of bankrupt countries.

- In China, slowing growth, a major stock market correction that remains unfinished, and recent devaluations of the yuan to stimulate exports will negatively impact that country and other

emerging markets in the Asia Pacific. - Japan’s fundamental economic flaws have no solution. They include two decades of deflation, a stagnant stock market, an aging demographic profile, and a self-imposed balance of payments

deficit incurred by idling of its nuclear energy fleet and importing more fossil fuels.

The good ol’ greenback is still the best of all currencies but, in my opinion, it had its run and will now continue to consolidate.With respect to gold, it has not reacted to significant geopolitical unrest in several regions of the world over the past year, including several new conflicts in the Middle East, the Russia-Ukraine civil war, higher incidences of radical Islamic terrorism, and most recently, a refugee crisis in Europe.

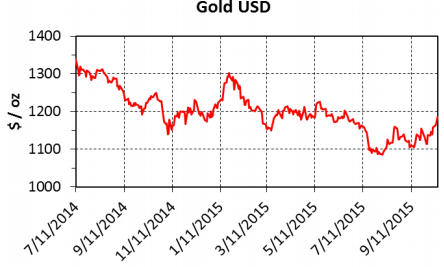

Gold has seemingly become immune to world events except when the Swiss franc was floated against the Euro in mid-January. That repricing caused gold to hit $1300 for one day and stay above $1250 for a little more than three weeks of trading. Since then, the price of gold has not approached $1250:

Widespread fear and panic in the financial markets is often a catalyst for gold buying as a safe haven and results in a rising gold price. But that will occur only if investors lose confidence in the world’s banking system as they did from late 2008 to late 2011.

Annual price inflation remains very low in developed countries despite the devaluation of major fiat currencies. The world economy is undergoing a deflationary event and that does not bode well for a significant rise in the gold price.

Lower gold prices in mid-July to early August and the recent upticks can be attributed to seasonality, i.e., the usual summer doldrums followed by the Indian festival and wedding seasons. I also expect strength in gold as the December holidays approach.

But for the short-term, I see no compelling reasons for gold to break out of its year-to-date range.

Let me sum up my position in two sentences, folks:

Gold ain’t goin’ anywhere anytime soon unless the US$ takes another exponential run-up or a great big nosedive.

And I don’t think either of those events is about to happen.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments