As April 2016 concludes, the diamond industry has without question

improved relative to a year ago, however, current industry data and commentary paints a mixed picture as to whether market fundamentals have in fact stabilized enough to support a new wave of sustainable growth continuing into the near-to-medium-term.

Demand

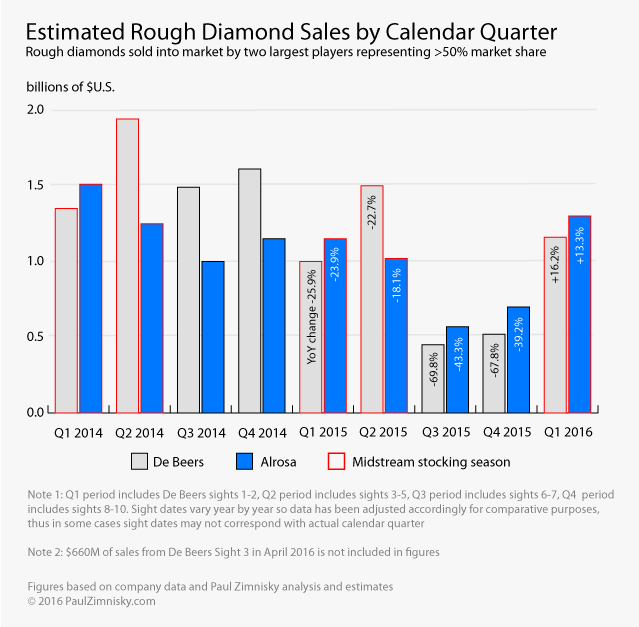

2016 rough sales through April have surprised to the upside, with De Beers and Russia’s Alrosa (RTS: ALRS) selling a combined $3.1B, which is an 18% improvement over a year ago, but still 13% below comparable 2014 figures. The demand so far this year is indicative how under-stocked the mid-stream sector was following very cautious inventory management going into holiday-season 2015.

In addition to inventory shortages, rough buyers benefited from a ~7% De Beers price cut in January which allowed for diamond manufacturer margin improvement, further supporting demand. Demand followed through in February which allowed De Beers to raise prices ~2% at its third sight of the year in April, the company’s first price raise since Q4 2014.

It appears that the midstream segment of the industry is adjusting to the new environment of reduced credit availability and is now more cognizant of the greater sensitivity the industry faces to macro market shocks. Diamond manufactures are seen buying rough stock only 3-months in advance, where as in the recent past they would buy 6-months out or more.

Canadian miner Dominion Diamond (TSX: DDC) recently noted that they have seen liquidity positions improve with a lot of their midstream clients as their stockpiles have been reduced relative to last year. In addition, while industry lending is still tighter than it has been in previous years, most cutters are comfortable with the current credit availability, and some of the more successful manufactures have actually received increased credit lines.

In March, Alrosa said they are seeing their clients work through the $2.7B of excess midstream inventory that built up through the end of 2014 as market conditions improve. They also indicated that they are seeing consolidation in the mid-stream space, noting that the midstream segment is the only segment of the industry that is not consolidated, and thus the least efficient, and the most responsible for the recent industry indigestion (more so than high rough prices). On a recent conference call Alrosa explained ‘(paraphrasing Russian translation) the midstream segment came to us and asked for a 10% price cut, and we gave it to them, but what will happen next is the retail segment will take 9.5% of that, and then the mid-stream segment will come back asking for additional cuts.’

Regarding demand specifics so far in 2016, there has been notable demand for typical bridal-quality SI1 diamonds (“slightly included 1,” or quality ranked 6th in an 11 category grading scale of clarity). On the contrary, there has been relative weak demand for very low-end diamonds, particularly low color-quality goods.

However, despite the consistent early demand for rough this year, January to April is typically the strongest season of the year for the rough market, and demand going forward will most likely depend on support from the retailers as the new incremental rough supply is polished and makes its way downstream in the coming months.

Tiffany & Co. location in downtown Manhattan. Source: Paul Zimnisky

Tiffany’s (NYSE: TIF) year-over-year same-store-sales in the U.S., the company’s largest market, were -8% in Q1 due to lower foreign tourist spending, as a stronger dollar made diamond jewelry relatively expensive for tourist’s in their domestic currency terms. Outside of U.S. the company noted primary weakness in Hong Kong, the UAE, and France, and noted strength in Mainland China, Japan, Australia, and the UK. In 2015, Tiffany opened 16 new stores, mostly in the Asia-Pacific region, and closed 4 in Europe. The company currently operates 307 stores.

Consignment internet-retailer BlueNile (Nasdaq: NILE) implied that diamond demand will be range bound in 2016 as the company expects revenue to be inline with 2015, noting any profit improvement will come from margin expansion. BlueNile primarily caters to U.S. customers.

The bifurcation of the Chinese market segmentation is becoming more apparent as Hong Kong/Macau growth continues to weaken relative to Mainland China as Hong Kong tourism declines and business-gift related jewelry purchasing in Macau decreases amidst an aggressive corruption crackdown. On the other hand, while diamond demand growth in Mainland has declined from its highs, the market is being supported by the expanding middle class consumer, offsetting declines in pure-luxury spending by the wealthiest segment of the population that has been impacted by real estate and stock market losses over the last 18 months.

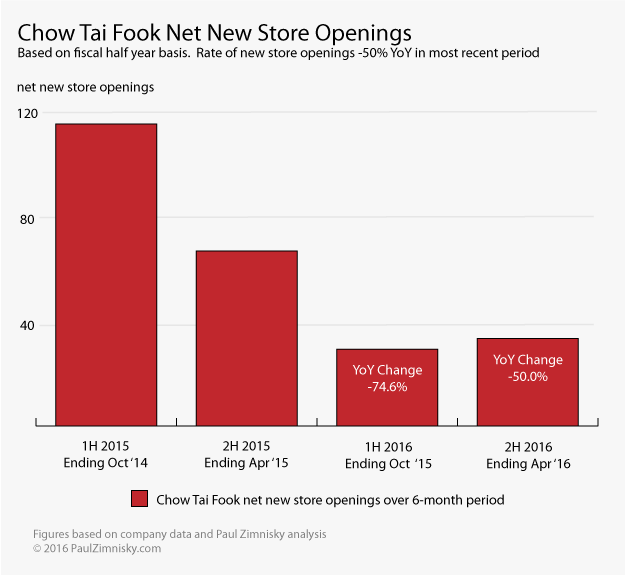

Greater-China retailer proxy, Chow Tai Fook’s (HK: 1929), year-over-year same-store-sales for the quarter ending March 31 were -25% in Mainland China, and -26% in Hong Kong/Macau, which compares to -9% and -26% in 2015, and +15%, -9% in 2014, respectively. The company attributed the dismal results to increased outbound travel in Mainland China and an overall weakening of consumer sentiment for luxury goods in the region amid the economic slowdown.

As of the end of March, the company had 2,319 point-of-sale locations, with 33 net new locations opened in the previous 6-months. This compares with 66 new locations opened over the same period last year, or a growth rate of new location openings of -50% year-over-year. 90% of the recent new openings were in Mainland China, with 80% of those specifically in Tier 3 cities. Chow Tai Fook stock is down 62% in local FX since the end of Q1 2014.

Dominion Diamond noted that the large retailers based in Hong Kong like Chow Tai Fook, others including Chow Sang Sang (HK: 116) and Luk Fook (HK: 590), probably have the industry’s largest relative inventory to work through. In comparison, the Mainland retailers are better positioned, which was indicated by their restocking appetite at the Hong Kong International Jewellery show, in March.

Also worthy of note, as of early April, the Chinese government took steps to encourage more domestic luxury spending within its boarders. According to Reuters, Chinese consumers account for 1/3 of global luxury good sales, but only 40% of those sales actually take place in Mainland China, as lower prices on like-for-like items and greater assurance of authentic goods make shopping in Europe, the U.S., and Japan, more appealing for Chinese luxury consumers. Beginning on April 6th, China raised tariffs on watches and jewelry purchased abroad from 30% to 60% and 10% to 15%, respectively. Penalties for false customs declarations were also increased.

Supply

While a strong U.S. dollar has in some cases subdued non-U.S. diamond consumer demand, the resulting weaker currency in producer nations has allowed production margins to remain stable, and in some cases increase, despite a weakening diamond price in U.S. dollar terms over the last year-and-a-half. This effect, along with lower oil prices, has encouraged increased diamond production in an environment where one might think that underlying diamond price weakness might discourage production growth.

Open-pit mining in Russia. Source: Alrosa

The U.S. dollar made multi-decade highs against major currencies in January of this year, despite since retreating through the end of March (e.g. U.S. dollar up 50% against the Canadian dollar since mid-2011, but down 10% in 2016; +25% and -7%, and +65% and -11%, for the U.S dollar versus the Euro and Yen, respectively).

For example, Dominion Diamond noted that a $0.01 movement in the average CAD/USD FX rate is expected to result in approximately a $500,000 difference in cash operating costs on a quarterly basis when converted back to U.S. dollars. 50% of the company’s costs come from labor and contractors paid in local currency. 25% of Dominion’s costs come from diesel fuel and other industrial consumables such as ammonium nitrate.

A new mine plan at Dominion’s Ekati operations could increase production upwards of 70% this year, or about 2M carats of incremental production. Production at the company’s other asset, Diavik, is also estimated to increase this year, around 10% or 0.5-1M incremental carats. Company-wide production is estimated at 12M carats this year on a 100% basis (Diavik is jointly owned by Rio Tinto).

Alrosa has released a production target of 37-39M carats for 2016, comparable to 38M carats produced in 2015, which was +6% over 2014. The company recently noted that they could increase production to over 41M carats as early as 2017.

During an investor event in March, Alrosa acknowledged that they did not strategically cut production in the second half of 2015, along with De Beers and Rio Tinto (LSE: RIO), due to the seasonal nature of mining in Siberia and the associated costs of operating in that environment, ‘(paraphrasing Russian translation) it’s so cold that you need to keep the machine engines running or you have to park them in a heated garage.’ However, undoubtedly the net positive effect of a very weak ruble over the last 2 years also incentivized the production increase.

Diavik diamond mine in Canada. Source: Rio Tinto

Despite increasing production last year in an oversupplied diamond market, Alrosa did strategically hold back supply released into the market in its own effort to support market fundamentals, thereby accumulating a stockpile of 22M carats worth $2.5B, as of the end of 2015. The company noted that its primary goal in 2016 is to not increase the stockpile any further, and that the company would instead cut production as much as 5M carats if the market warranted. Further, Alrosa noted that it is the decision of the advisory board as to whether to hold the excess stockpile, thus pressuring company working capital, or to sell into the market, thus pressuring prices to an extent that is indeterminate at this point. The company estimates that the whole industry’s current excess inventory should be exhausted by 2019 at current production rates and 1% annual growth in diamond demand.

De Beers is on pace to maintain its 2016 production guidance of 26-28M carats, which would be a 5-10% decrease over 2015. In Q1, only two De Beers mines showed year-over-year production volume increases, Jwaneng and Venetia, which increased 13% and 15%, respectively. The later, the largest diamond mine in South Africa, is currently being converted to an underground mine at a cost of $2B, with a plan of extending production 22 years to 2043 with production ramping-up to 5M carats annually, up from 2M currently.

Rio Tinto’s Argyle mine in Australia, which is currently the highest production mine in the world by volume, is on pace to exhaust resources by 2020 or 2021. Argyle is estimated to produce 12-14M carats this year. With resources like Argyle dwindling, Alrosa recently mentioned that it sees Angola, relative to Russia or Botswana, as the nation with the most upside potential for new discoveries because it has been underexplored relative to other diamond rich locations in the world.

Endiama, Angola’s state-run diamond miner, in March said that it’s new Luachi project could host as much as 350M carats with an annual production of 12M carats, which would put it on scale with Argyle. Endiama currently operates the Catoca mine, which is located in the same province as Luachi, and is one of the richest diamond mines in the world estimated to produce 6.5M carats this year worth $550M. Endiama noted that it plans to spend $300M of capex on phase-1 of the Luachi project, with the potential to spend as much as $800M over six years. Initial production could commence as early as 2018 according to Endiama, although very few official details on the project have been formally released.

Pricing

London-listed Petra Diamonds (LSE: PDL), last week said for the 6-months ended March 31, the company realized a rough diamond price increase of 3.5% on a like-for-like basis. The company noted that it plans to use this price level for its internal business modeling for the remainder of 2016.

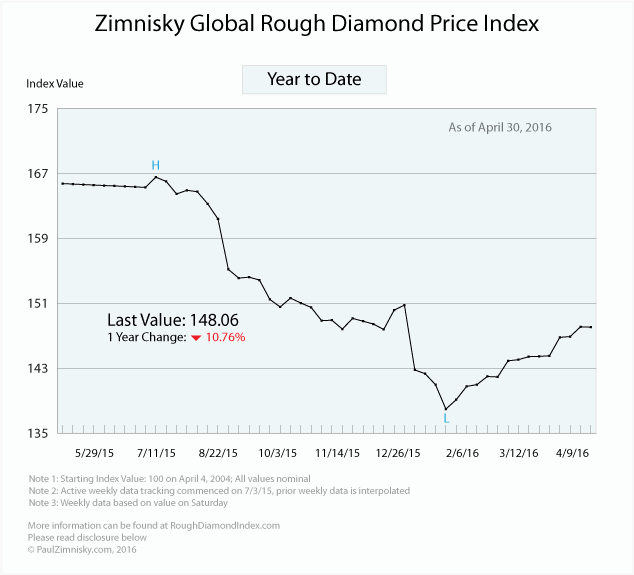

As of April 30th, the

Zimnisky Global Rough Diamond Price Index indicated that rough prices are up 2.4% over the last 30 days, down 1.7% over the last 6 months, and down 10.8% over the last 52 weeks. The Index is up 5.4% after hitting a 52-week low on Jan 23rd.

Last year the Index was down 16.2%. Alrosa recently said at an analyst presentation that it’s average realized diamond price was down 15% in 2015, but the price decline could have been as severe as down 40% if it had not had long-term contracts in place.

—

De Beers is 85% owned by Anglo American plc (LSE: AAL) and 15% owned by the Government of the Republic of Botswana.

At the time of writing Paul Zimnisky held a long covered-call position in Dominion Diamond Corp. and BlueNile Inc. Please read full disclosure here.

Comments