Special Report: The platinum opportunity – part 1

This is Part 1 in our series focused on platinum. Part 1 serves as a primer on platinum, and in Part 2 we explore the unique supply-demand fundamentals that support our bullish outlook.

Platinum’s Multi-Year Weakness

When comparing spot prices for platinum and palladium, it’s easy to assume that vastly different story lines have shaped the performance of these two metals. Over the past six months, platinum’s price has continued its multi-year decline, falling below $800 – close to its lowest level in a decade. Palladium’s fate, by contrast, has seen far more luster, as it surpassed $1,000 in price for the first time late last year. In recent weeks, a surging U.S. dollar on the back of trade-war fears has pushed all metals lower.

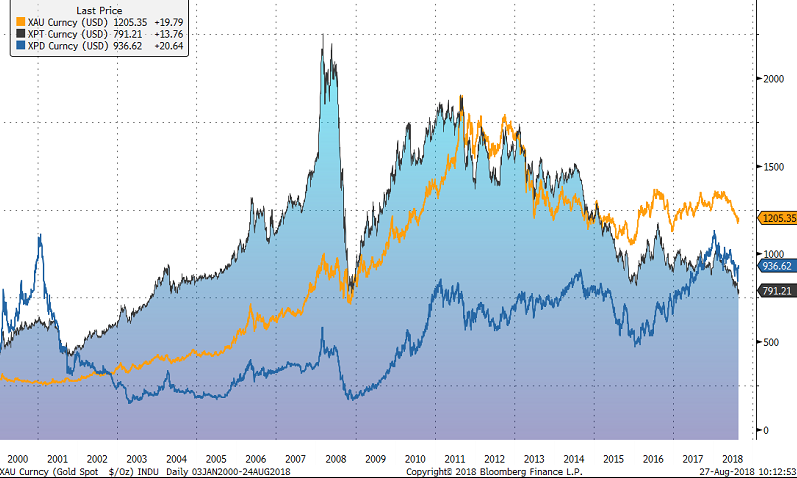

Platinum, as shown below, is trading well under the 1.0 platinum-to-gold ratio that is considered the historical norm, and which we have not seen since 2015. The current ratio of 0.66:1.0 means platinum is currently a bargain: an ounce of platinum is selling at 66% the price of an ounce of gold. Platinum is also severely undervalued relative to its white gold “cousin” palladium given that it has historically traded at 2-4 times the cost of palladium.

Figure 1: Platinum vs. Gold and Palladium Prices Since 2000 Source:

Bloomberg. XPT (black line/shaded blue) represents platinum; XAU (gold line) represents gold; XPD (dark blue line) represents palladium. 1/6 Special Report August 21, 2018

“Precious” is relative

Platinum (Pt) and palladium (Pd) are primarily used as industrial metals but also have a strong correlation to the “precious” metals gold and silver. Both are much rarer than gold and represent tinier markets. Recent world production of platinum and palladium has averaged about 175 and 200 tonnes per year, respectively, while gold production tallies approximately 3,000 tonnes per year.

Also known as “white gold” or the “bright white metals,” platinum and palladium are members of the Platinum Group Metals (PGM) and typically co-occur in ore deposits (the group also includes ruthenium, rhodium, osmium and iridium). Their shared chemical origins give platinum and palladium similar characteristics, such as being relatively inert and having high melting points – appealing features for use as catalysts in industrial and automotive applications. Platinum is denser and stronger than palladium and has historically commanded a higher premium; it’s also the preferred choice for jewelry, driving additional demand. South Africa is the world’s largest producer of both metals, with its storied Bushveld Igneous Complex (BIC) responsible for 75% of the world’s platinum output and 50% of its palladium. Russia is the second largest platinumproducing country but surpasses South Africa in palladium. Zimbabwe, Canada and the U.S. round out the top-five homes to the PGM.

The Automotive Industry is the Largest Pt-Pd Consumer: Catalytic Converters

Figure 2.

The primary driver of demand for both metals is the automotive industry. Platinum and palladium are key elements in the manufacturing of catalytic converters which help reduce toxic emissions from automotive exhaust. Rising car production (especially in emerging economies) and tightening emissions standards worldwide has fueled steady growth in the use of catalytic converters. 2/6 Special Report August 21, 2018 1 Johnson Matthey: PGM Market Report May 2018. Special Report August 21, 2018 3/6 Historically, platinum has been the much more expensive metal. However, over the past decade demand for lower cost palladium as an alternative has soared and platinum demand has fallen. Although palladium has been the bigger beneficiary of auto sector momentum and trends in recent years, our view is that this dynamic may be changing in favor of platinum.

Palladium passes platinum on the road

Auto manufacturers use precious metals in catalytic converters because PGMs catalyze these high-temperature reactions without being consumed or chemically altered. Because they do not degrade easily, the platinum and palladium within catalytic converters can often be salvaged when a car has reached the end of its road. Over the past decade, as technology has improved, auto manufacturers discovered that gas-powered vehicles didn’t require platinum’s higher temperature stability to effect this chemical change. Instead, lower cost palladium worked just as well for their needs. As a result of its price discount, palladium became the primary metal in this essential auto part, driving demand and ultimately price gains. Today the automotive sector accounts for 75% of palladium demand with its use surpassing 8.39 million oz. in 2017. With an 801k oz deficit in 2017, palladium ironically finds itself trading at a premium to platinum.

Diesel gate hurts platinum

Diesel vehicles typically use platinum-based autocatalysts since the metal performs better than palladium in this application. But due to increased restrictions on diesel vehicles in Europe and Japan, there has been a reduction in the market share of diesel vehicles in the past five years. The scandal around manipulated diesel vehicle emissions, known as dieselgate, in particular, has been strongly linked to a reduction in the purchase of new diesel vehicles in Europe. This has negatively impacted platinum’s demand from the automotive sector. The typical car contains a mere three to seven grams of palladium or platinum. Assuming the midpoint of five grams, an average car, which sells for $40,000 in the U.S., only carries a mere $160 worth of palladium or approximately $140 worth of platinum at current prices. Automakers are therefore relatively insensitive to the price of either platinum or palladium. What auto-makers genuinely care about, however, is the surety of supply of either of these metals.

Platinum’s other sectors: High-performance glass

Platinum’s future looks very promising in many of the other industries in which it’s used, including glass making, jewelry, petrochemical, fertilizer manufacturing and fuel cells. While palladium can often work interchangeably with platinum in the auto sector, it’s not always the case for other industrial uses. In the electronics, chemical and glass sectors, the needs for the metal become more complex, so these sectors are unable to substitute platinum with other metals. Platinum’s industrial demand, which is expected to rise 3% in 2018, is driven by the growth in the glass sector. Platinum has become indispensable for the manufacturing of high-performance glass used in television sets, phones and other types of smart glass as well as optical fibers. The glass sector currently accounts for 17% of platinum’s industrial use and this demand appears poised for a continued rise. Platinum is named for the Spanish word “platina” meaning “little silver.” Palladium was named by its discoverer William Wollaston in 1803, after the asteroid Pallas. Special Report August 21, 2018 4/6

India is the fastest growing market for platinum jewelry

Platinum also has a fairly robust demand within the jewelry sector. The World Platinum Investment Council evaluated this dynamic over the past 15 years, determining that platinum was trading primarily as a precious metal with an industrial premium from 2002 to 2005. Platinum was then redefined as an industrial metal with a precious floor in the eight years that followed. In 2013, another shift occurred, in which platinum began trading as a precious metal with an industrial discount, as it stands now. Platinum’s use as a precious metal in jewelry is on the rise, particularly in India. Demand in the country increased by 16% last year, albeit from a low base. Uptake of platinum for jewelry making in regions like India is helping buffer the loss of demand from traditional platinum jewelry buyers in China and Japan.

Fuel cell electric vehicles

Platinum (but not palladium) is also used to catalyze the electricity-producing conversion of hydrogen and oxygen into water in hydrogen-based fuel cells, increasingly used in electrical vehicles. While fuel-cell makers will look to reduce the amount they use in each cell over time to reduce cost, the minimum amount of platinum required in fuel cell electric vehicles (FCEV) is still multiples higher than in internal combustion engine (ICE) automobiles. The number of fuel-cell vehicles operating is expected to see rapid growth with a million FCEVs on the road in China alone by 2030. This equates to over 7 million traditional vehicles as a result of higher platinum usage in FCEV vs. ICE autos.

Platinum’s turn on the road?

Due to the largely interchangeable use of platinum or palladium in non-diesel ICE cars, palladium took over much of the auto demand. Palladium, however, could soon become a victim of its own success since it has reached a price point that far surpasses platinum. Thomson Reuters estimates that palladium could average above $1,000 for the year, for the first time.2 How dramatic of a shift is that in price? A decade ago, it wasn’t unusual to see an ounce of palladium trade at a $1,000 discount to platinum. As Andrew Hecht wrote, “Industry had become addicted to palladium because of its lower price and comparative value compared to platinum over past years.” But, as we’ve discussed, all things equal, platinum and palladium perform interchangeably within non-diesel ICE autocatalysts. Historically, palladium’s virtue was its lower price. It’s just a question of whether the price of palladium has reached a point that would encourage manufacturers to switch back to the preferred metal, platinum. There are indications that this shift has begun. Unlike the previous cycle, which was driven by thrifting platinum with palladium, this cycle will be driven by the availability of the metal as palladium deficits continue to linger.

In part 2, Portfolio Manager Shree Kargutkar takes a deeper look at the supply dynamics that support our bullish outlook.

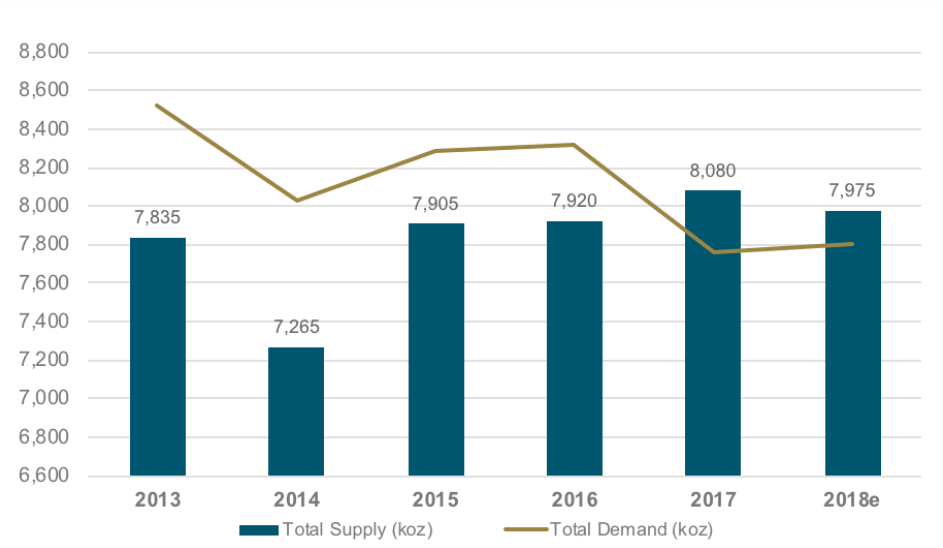

The Platinum Supply Factor Platinum is unique in that about 70% of the supply comes from South Africa alone. This leaves the supply of platinum at risk to changes in labor issues or other localized disruptions, which has hurt platinum’s supply in recent years. Palladium, on the other hand, is more evenly spread out between Russia, South Africa and the rest of the world. 2 Thomson Reuters: GFMS Platinum Group Metals Survey 2018. 5/6 Special Report August 21, 2018 Figure 3: Platinum Supply vs. Demand (2013-2018e)

Source: World Platinum Council.

(By John Ciampaglia)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments