Mining equipment market to pick up in 2017 – report

Parker Bay’s Mining Equipment Index marked a 10-year low for large surface mining equipment shipments which are now at levels not seen since the start of the commodities Super Cycle. With the current downturn approaching the end of its fourth year, Parker Bay has just finished an in-depth analysis of the global markets for large mining excavators/loaders and haul trucks, plotting the path forward with respect to the industry’s expected equipment requirements and attendant shipments through 2020.

This extensive analysis and forecast is documented in Parker Bay’s just-released report entitled “Market Analysis and Forecast: Loading and Haulage Equipment”. The 130-page report and accompanying data file examines the impact of the commodities Super Cycle of 2003-2012 and the dramatic reversal and continuing contraction of mining industry fortunes on equipment markets and manufacturers. All historical data contained in this report are derived from Parker Bay’s ‘Mobile Mining Equipment Database’ which identifies each machine by individual mine in more than 100 countries, producing a major share of the world’s coal, copper, gold, iron, oil sands and more than 20 other minerals vital to global economies.

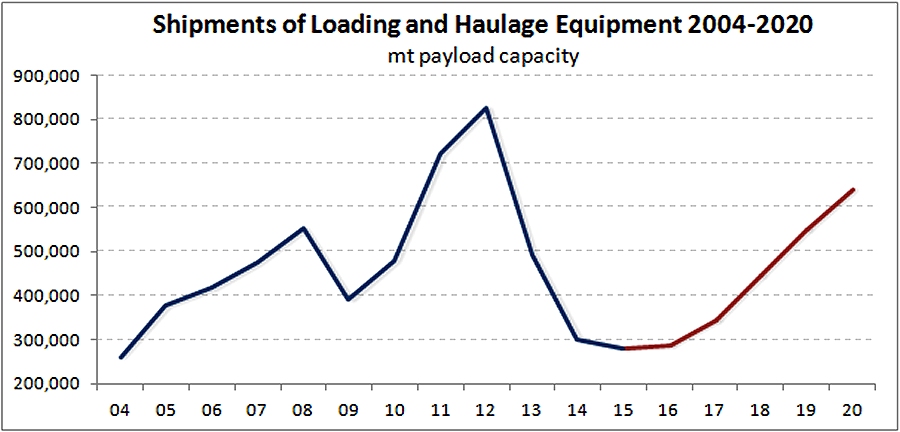

Over the ten years through 2014, global equipment manufacturers delivered 6,400 large excavators (20-mt-plus payload) and nearly 31,000 large trucks (100-mt+ payload) with an installed value of nearly US$80 billion. While most of this new capacity was required fuel the growth in mineral output, it became clear that by 2013, more mine capacity had been added than was required by underlying mineral requirements. The escalating oversupply, combined with slowing demand from China and elsewhere, initiated the downward spiral in mineral prices that continued through year-end 2015. This in turn compelled companies to close many mines, curtail output at others, and drastically cut capital expenditures including those allocated for the equipment covered by this report.

Parker Bay’s report examines the factors now impeding a recovery and those that will eventually spur a resumption of growth for these machinery markets. Chief among these factors are: the excess capacity at mines including more than 4,000 machines parked and available for resale and redeployment when demand warrants it; the eventual requirement to replace large numbers of the 9,000-plus excavators/loaders and 40,000-plus trucks now in service; continued growth in mineral demand in spite of currently depressed prices.

Among Parker Bay’s key conclusions:

- Very slow growth in mineral production through 2020 will warrant increases in installed machine capacity of less than 1.5%/year through 2020 as compared to annually increases of 7-10%/year during the past decade.

- The current ‘overhang’ of surplus machines will reduce near-term demand for new machines by as much as one-third during 2016 and will continue to reduce new machine requirements through 2018.

- Replacement requirements will be the chief driver in the recovery that will begin in 2017. Despite their best efforts to extend equipment service life and reduce the need for investment in their replacements, mines will eventually have to retire these machines as they become subjects of increasing maintenance and repair and simply uneconomical to continue working. Parker Bay estimates nearly 2,500 excavators/loaders and 12,000 trucks will reach this stage during 2015-2020. As a result, a substantial majority of all machines shipped during this time will be required to simply maintain the existing fleet.

The result of these combined factors will be an equipment market that continues at current depressed levels through 2016 and begins recovering in 2017. This recovery with escalate during 2018-2020 as these markets have in past growth cycles. But the slow growth in mineral demand will dampen this next cycle to the extent that projected 2020 shipments will still be as much as 25% below the 2012 peak.

Interested parties are encouraged to contact Parker Bay at [email protected] or by visiting the Company website www.parkerbaymining.com/services/mining-market-reports.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments