Copper sinks on the wrong sort of supply disruption: Andy Home

By Andy Home

Copper has fallen almost nine percent in price over the last couple of weeks.

In London three-month copper was this morning struggling to hold the $6,700 level, a chart area last breached in early April.

Copper has been caught up in the broader risk-off trade that has accompanied the steady ratcheting up of trade war rhetoric.

But the price weakness is also reflecting what is, by copper’s standards, a period of remarkable production stability.

A year of expected supply disruption, mainly from expiring labour contracts in Chile, has so far not played out that way.

Although there is still plenty of potential for disruption at the Escondida mine, where management and unions are locked in talks, and at Codelco’s Chuquicamata division, the first six months of the year have seen no major labour-related stoppages.

It’s not there hasn’t been lots of disruption to copper’s supply chain. It’s just that it has taken place at the refined metal segment of the chain, distorting trade flows but not directly removing units from the supply-demand balance.

MINE PRODUCTION BOOMS

Global mined copper production surged by seven percent in the first three months of this year, according to the International Copper Study Group (ICSG).

The Group’s most recent forecast, made at its April meeting, was for production to rise by a little over three percent this year.

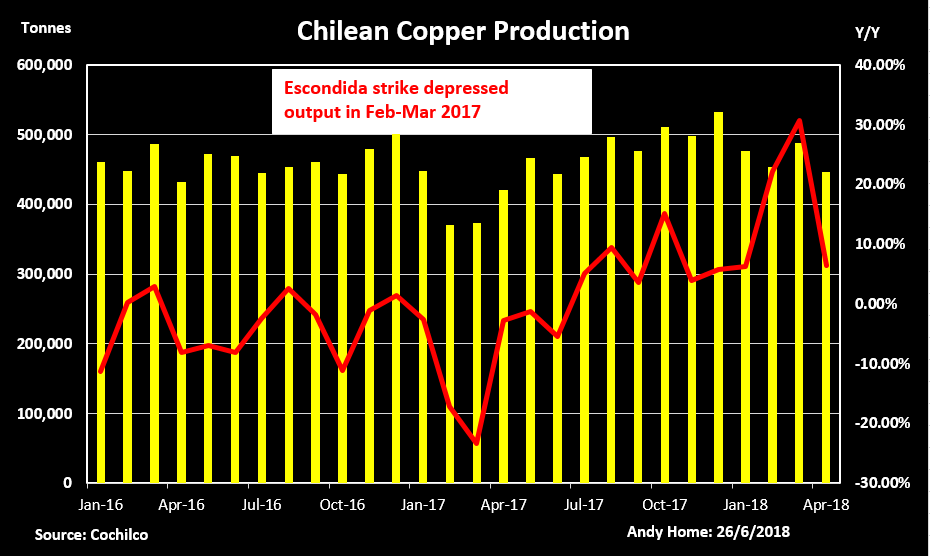

For sure, the early year-on-year comparisons are skewed because of low production in Chile and Indonesia last year.

Chilean production rose by 19 percent in the first quarter of 2018, reflecting the 44-day stoppage at the Escondida mine in February-March last year.

Similarly with Indonesia, where output last year was disrupted by a stand-off between Freeport McMoRan, operator of the Grasberg mine, and the Indonesian government, which resulted in a temporary ban on exports. The country’s mined copper production was up by 58 percent in the January-March 2018 period.

However, even excepting these numerical outliers, the simple truth is that copper production, historically prone to all sorts of disruption, has been running very smoothly to date.

Key to that performance has been the successful renegotiation of multiple labour contracts.

There are 16 major contracts still to expire, including those at Escondida, the world’s largest copper mine, and at just about all of state-owned Chilean Codelco’s operations.

Escondida is in focus right now with the current contract set to expire on July 24.

Last year’s bitter dispute was only “resolved” by rolling over the labour contract for a year after no meeting of management-union minds.

Codelco, meanwhile, is heading for a showdown at its Chuquicamata division, where tensions are running high over the company’s restructuring plans, which may entail up to 1,700 redundancies.

So far, however, analysts are struggling to fill the production disruption allowances they factor into their copper supply-demand forecasts.

REFINED PRODUCTION HIT

The biggest single disruption to copper production this year hasn’t happened at any mine but at the Tuticorin smelter in the Indian state of Tamil Nadu.

The plant has long been accused of environmental damage by local residents but in May tensions boiled over, resulting in the killing by police of 13 protesters.

The smelter has been ordered to close permanently and right now owner-operator Vedanta Resources is struggling to persuade the authorities even to allow basic access to the plant to check a leaking sulphuric acid storage unit.

Tuticorin produces around 400,000 tonnes of refined copper per year and its continuing shutdown has significant implications for the Indian copper market and regional flows of refined copper.

With Indian consumption estimated to be running at around 1.5 million tonnes annually, imports will have to increase by at least 200,000 tonnes to fill the gap, according to local consumers.

Any resulting tightening in the regional refined copper market will be exacerbated by downtime planned at another smelter, PASAR in the Philippines.

The plant, majority owned by Glencore, took typhoon damage at the start of the year and will operate at a reduced rate in the second half of the year as it replaces coolers at its sulphuric acid unit.

Neither smelter outage, however, will affect analysts’ supply-demand calculations.

The concentrates not treated at Tuticorin will be redirected for refining elsewhere, most likely in China.

As such, no copper is “lost” to the market in the way that last year’s Escondida strike removed 215,000 tonnes of mined production from the supply picture.

SCRAP FLOWS HIT

It’s a similar situation with copper scrap, which is experiencing a year of turbulence thanks to China, the world’s largest single buyer.

China’s tightening of the rules governing the purity of imported scrap saw import volumes plunge by almost 40 percent in the first quarter of the year.

A sharp jump in implied copper content largely offset the headline drop in terms of the metal impact.

One of the clear trends in the first months of 2018 was the emergence of the United States as primary supplier to China of high-purity copper scrap.

However, flows between the two countries ground to a halt in early May due to the suspension of pre-shipment inspection services in the United States.

The outlook is still highly uncertain, with U.S. scrap industry body ISRI saying it has “learned from contacts in China” that the sole previous inspection agency, AQSIQ, may have been dissolved and its functions transferred directly to China’s customs authorities.

Watch this space, but for now it’s unlikely much copper scrap is heading to China.

It’s difficult to quantify the impact of that since Beijing has suspended publication of its detailed trade figures. Those for April and May are both pending with no timeline on when, or even if, they will reappear.

Logically, reduced copper scrap availability should translate into increased Chinese import appetite for copper in other forms, either refined metal or copper concentrates.

The preliminary import figures for China, which have survived the authorities’ information cull, seem to bear out this displacement effect.

Unwrought copper imports were up 17 percent in the January-May period, while those of concentrates were up by 14 percent.

None of which, though, pushes the buttons for an investment community which remains focused only on the mine production side of the market balance ledger.

Supply-chain disruption there is aplenty. It’s just the “wrong sort” of supply disruption for the outright copper price.

(Editing by Jan Harvey)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments