China’s lithium price decline is not the full picture to an industry surging

The downturn in Chinese lithium prices since the start of the year has left many questioning the future of a market which has experienced its biggest upturn in history since late-2015. It has also led to many false conclusions about what is really happening to the lithium price.

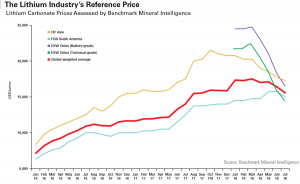

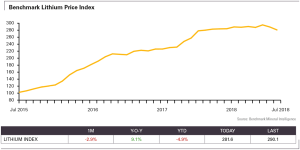

When lithium prices began to spike in H2 2015, few expected the increases to continue for another two years, let alone reach the heights of Q1 2018 when the average price of battery-grade lithium carbonate peaked at $24,750/tonne.

It’s critical to note this decline is not the case for the rest of the world or for lithium hydroxide

However, the slow supply response to what in the future will be seen as a period of relatively moderate demand growth kept prices rising long-beyond the early 2017 deadline that many had marked for a price crash.

The growing separation between China and rest of the world (ROW) lithium prices was not sustainable and slower than anticipated demand growth in H1 2018, coupled with increased domestic production (in particular from Qinghai’s lithium brines) finally brought an end to the excessive price premiums in the Chinese market by Q2 2018.

The subsequent decline in Chinese lithium carbonate prices, which slipped over 9% to $14,500/tonne for technical grade material and $16,500/tonne for battery-grade material in July 2018, is expected to continue over the coming weeks.

There are two important factors behind this: the nature of ROW contracts and the underlying market balance outside of China.

Firstly, the longer-term nature of contracts for the majority of the market outside of China has, and will continue to, insulate prices in the short-term. Just as the pricing functions built into contracts prevented ROW prices peaking to China levels in 2017, so too will they protect them from falling to China levels in 2018.

Secondly, and more important to the long-term sustainability of the market, is the fact that the market outside of China still remains relatively tight. Despite expansions in South America finally beginning to bear fruit, the incremental new volumes reaching the market are not going to create the huge oversupply problem some institutions have warned of.

Expansions are nevertheless inevitable.

What is less inevitable is the timing and type of lithium that will be entering the supply chain in the coming years

Quality over quantity

Much of the new lithium supply to enter the market this year has been technical grade lithium carbonate from China.

The subsequent price downturn for carbonate has seen buyers hold back from new orders, anticipating lower offers, and the inability to place this material has seen volumes enter international markets which have begun to put pressure on ROW pricing.

Typically, however, the majority of lithium produced in China is sold domestically and this will become increasingly the case as the credit issues the country’s battery sector faced in H1 are resolved and new battery production capacity enters the domestic market.

It is also important to differentiate between the type of material that is entering the supply chain, with only a small proportion yet meeting battery grade specifications. While many will argue this is just a matter of upgrading processing, few (even among the majors) have historically been able to resolve these issues quickly, and if they are resolved, the question becomes at what cost.

New Chinese supply from domestic feedstock sources already has a significantly higher cost base than in South America and adding additional purification and processing obstacles will only increase these costs further, making it all but impossible for prices to slump to pre-2016 levels.

What’s more, with increasing amounts of off-specification lithium carbonate being used in lithium hydroxide production, excess lithium carbonate volumes are easing with lithium units being redirected towards a hydroxide market which has a strengthening demand outlook as a result of China’s push towards nickel-rich cathode chemistries. This switch has been encouraged by the change in China’s EV subsidy programme in H1 2018, which now resolved also strengthens the outlook for H2 demand.

EV & battery demand is surging

The uncertainty sparked by China’s change in EV subsidy policy wreaked havoc in the EV supply chain and saw slower than anticipated demand growth in the first half of 2018.

Despite these challenges, H1 NEV production in China was up 94% and seasonal production patterns alongside the clarification in policy means H2 will almost certainly be another record breaking six months for output.

In addition, the ongoing ramp up at Tesla’s Nevada Gigafactory 1 and the multiple other megafactory expansions in the pipeline – all of which are being built around lithium ion technology – mean the longer-term outlook for lithium demand continues to strengthen.

China has put itself at the centre of this supply chain, and its lithium consumption will increase exponentially over the coming years.

As a result, at Benchmark we urge caution to view the price downturn in Chinese carbonate as the story for all lithium, because it is not. It is an early correction to the lithium carbonate market in China that will go through several phases of growth over the next decade. The growth of anything, let alone an industry that is increasing seven-fold in the next ten years, is not linear. There will bumps in the road as each part of the battery supply chain – from lithium mine to chemical plant to cathode and battery manufacturing – builds out.

(By Andrew Miller)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments