Pacton Gold stacks up more acquisitions in Pilbara area play

An area best known for iron ore mining is continuing to get traction as a gold area play, as juniors rush in to stake claims, in what has become the modern-day equivalent of the Klondike Gold Rush. The Australian Pilbara is home to numerous iron ore mines, and one of the world’s largest iron shipping terminals, Port Hedland. Some of the biggest mining companies have operations there including Rio Tinto, BHP and Fortescue Metals Group.

But over the past couple of years, explorers haven’t been looking for the steelmaking ingredient found within the red soil of the Pilbara, but rather are on the hunt for gold nuggets.

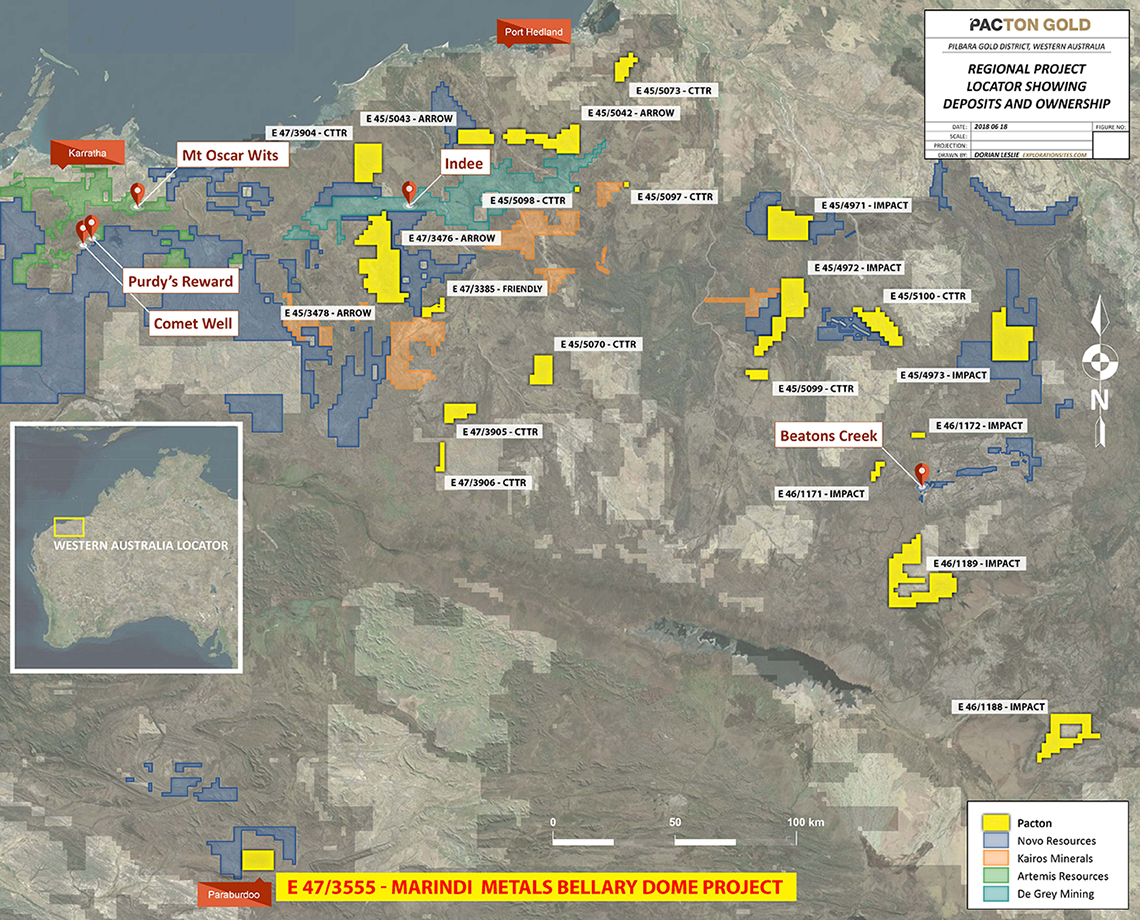

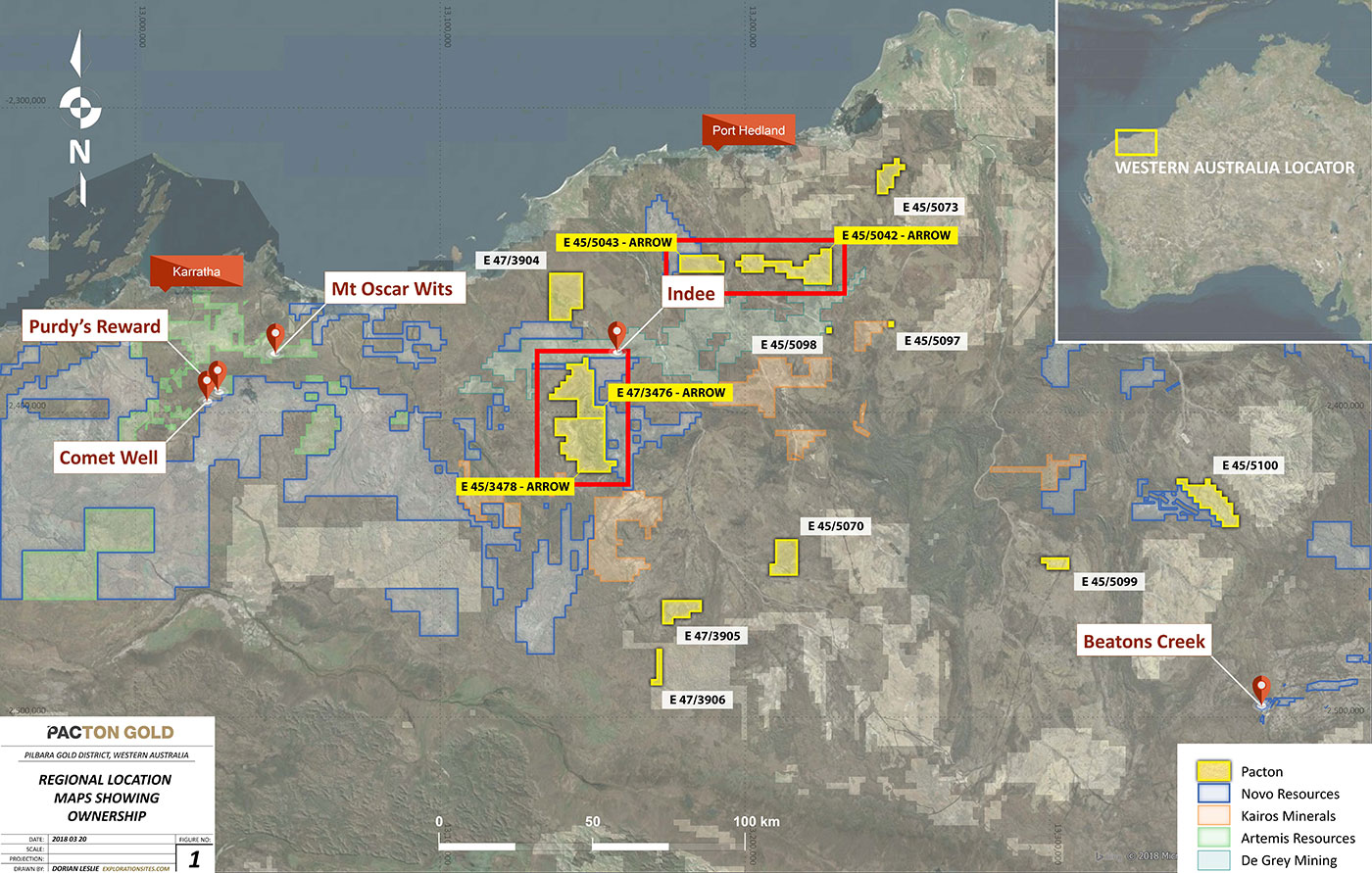

Pacton Gold (TSXV-PAC; US: PACXF)) is in the thick of the race to acquire prospective ground in this thinly populated, dry, dusty region of Western Australia. Vancouver-based Pacton recently became the third largest landowner in the Pilbara, behind Novo Resources and Artemis Resources. Pacton now controls about 2,227 km2 of terrain, having added 1,126 km2 through the acquisition of a subsidiary of Impact Minerals Limited (ASX:IPT), Drummond East Pty Ltd., announced on May 22, 2018. The company followed that up six days later with another acquisition, the Friendly Creek exploration license and mining leases from Gardner Mining. According to Pacton, Friendly Creek is “historically one of the richest known areas for alluvial nuggets within the Pilbara region,” where fine-grained to nugget-sized gold was found in the 1880s and 1890s.

“The acquisition of the Friendly Creek Project, with granted mining leases, clearly places Pacton with a strategic advantage ahead of our peers”

“The acquisition of the Friendly Creek Project, with granted mining leases, clearly places Pacton with a strategic advantage ahead of our peers in creating the opportunity to rapidly conduct large scale bulk sampling programs. The historical discovery of large gold nuggets at Friendly Creek in Western Australia, and an identified mineralised strike length of 10 km, is compelling to justify an upcoming intensive exploration program,” said Alec Pismiris, interim president and CEO of Pacton Gold.

And the hits just keep coming. On June 20 Pacton entered into a letter of intent (LOI) to acquire the Bellary Dome exploration license from Marindi Metals. The property hosts about 25 kilometres of strike length and is surrounded by Novo Resources, the dominant player in the Pilbara.

Before getting into the nitty gritty of Pacton, a little background on the Pilbara gold play is in order.

First discovery

The play was started by Novo Resources back in 2010 when the company, also based in Vancouver, started exploring around Beaton’s Creek, on the eastern side of the far-flung region. Novo was searching for gold-bearing conglomerates within the Hardey Sandstone Formation, part of the Fortescue Group, a thick sequence of ancient sedimentary and volcanic rocks. Historic mines exploited pyritic gold-bearing reefs back in the late 1800s, but little exploration had been done since.

Fast forward six years to Artemis Resources, a tiny junior with a $3 million market cap. Its managing director Ed Mead began looking around Purdy’s Reward, south of the town of Karratha, when he came across some unusual gold nuggets in the shape of watermelon seeds, as told by Perth Now. For the next two months Mead roamed the area with a metal detector, and came to the conclusion that the rock formations of the Pilbara had been misread by geologists and it contains a huge amount of gold.

Hot stocks

Penny stock Artemis tripled in value, going from 5 cents to 16 cents, after announcing it had found unique flat nuggets at Purdy’s Reward. In a 50-50 joint venture, Novo cut a deal with Artemis, offering 30 million shares in return for spending $2 million a year at the property. Investors started salivating when terms like “Witwatersrand-style” and “conglomerate-hosted” gold started finding their way onto stock bull-boards.

Last summer Novo’s stock shot up 700%, hitting an all-time high of $8.40 on Oct. 2, 2017, with the market cap leaping from less than C$100 million to over a billion – achieving the elusive “10-bagger”. Other companies did well too, including De Grey Mining (+260%), whose Pilbara Gold Project is 60 kilometres south of Port Hedland. At the height of the frenzy, last September/October, the stocks of more than a dozen Pilbara gold explorers rose at least 24% within about two weeks.

“Wits” comparison

All the excitement is being driven by the potential for the area to become a major gold-producing region on par with the Witwatersrand Basin in Africa (“Wits” for short), which has a similar geological footprint to that found in the Pilbara. The Witwatersrand contains the world’s largest known gold reserves and has produced over two billion ounces – about half of the gold ever mined on Earth.

Gold is already produced in all Australian states and the Northern Territory, with about two-thirds of the country’s entire gold output being mined from Western Australia, according to the Mineral Council of Australia.

Geologically, the Pilbara and the Witwatersrand both contain rocks dating to the same geological period, the Archean, about 2.5 billion years ago

Geologically, the Pilbara and the Witwatersrand both contain rocks dating to the same geological period, the Archean, about 2.5 billion years ago. The Earth was so old during the Archean that oxygen was yet to exist, so gold was more “mobile” than in later geological periods. The geological theory espoused by Novo Resources, led by respected geologist Dr. Quinton Hennigh, is that gold was transported into the Pilbara Basin by hot geothermal fluids, and dumped into algal “mats” where they were reworked as nuggets.

The puzzle yet to be solved in the Pilbara is the source of the nuggets. What is known is that they are dispersed over a wide area – roughly 300 by 100 kilometres – which has precipitated a staking rush as companies move in to grab of piece of the action. It’s the classic “area play” scenario that has been played out in various hot gold areas, particularly in Canada. Examples include Hemlo in Ontario, the White Gold Rush in the Yukon, and the Golden Triangle of British Columbia.

Pilbara explorers are particularly searching for zones where the older Pilbara greenstone rocks contact the Fortescue Group rocks, which is where the gold nuggets are typically found.

Key players

Novo Resources is the dominant player with “first move advantage” in the Pilbara, with the largest land package – 12,000 square kilometres – and the Karratha Gold Project, which includes Comet Well and Purdy’s Reward. It is also the best funded, with around $72 million in cash. De Grey Mining has a measured and indicated resource of 536,000 ounces, NxGold with its Mt. Roe Project is in close proximity to Novo’s Karratha Gold Project, and Kairos Minerals’s Croydon Project has 22 kilometres of strike on 115,800 hectares. Other key players in the Pilbara gold play include New Frontier Exploration, Calidus Resources, Marindi Metals, Artemis Resources which is a 50/50 JV partner with Novo at Purdy’s Reward, International Prospect Ventures, Coziron Resources, Millenium Minerals, Arrow Minerals, Impact Minerals, Kalamazoo Resources, DGO Gold, Macarthur Minerals, and Pacton Gold.

Pacton goes on a buying spree

Pacton Gold entered the Pilbara scene after renaming the company from Noka Resources and bringing on Alec Pismiris as interim president and CEO, last year. Pismiris is a well-known name “Down Under” where he was involved in several multi-million ounce discoveries including a deal with B2Gold. Pismiris was founding shareholder and director of Papillon Resources when in 2014 it was swallowed by B2Gold for its Fekola project in Mali. Pismiris was also with Cardinal Resources which plans to publish a PEA shortly on its open-pit gold project in Ghana.

In February 2018 Pacton started to put its land package together, joining up with Sprott Capital Partners who came on as advisors. Momentum was gained when legendary gold bug and investor Eric Sprott made a $2 million investment in Pacton and ended up with an 18% stake, on a fully diluted basis. Sprott is also a major shareholder with Novo and Kairos Minerals – indicating his strong belief in the potential of the Pilbara play. Mid-tier producer Kirkland Lake Gold is also a significant shareholder in Novo, having bought 4 million shares in May.

Acquiring properties in the Pilbara on prospective ground took place in three stages. The first transaction involved the acquisition of a 492-square-kilometre land package from CTTR Gold. The properties consisted of nine claims adjacent to lands controlled by Novo, Kairos Minerals and De Grey Mining.

“The CTTR transaction provided Pacton with a strategic entry into the Pilbara, with minimum dilution at the early stages of our due diligence review of the area. [$100,000 in cash and 916,666 shares]. It was our first initial step into the Pilbara, as we continued to review larger acquisitions that would assist our goal of becoming one of the largest landholders, second only Novo Resources,” said Dominic Verdejo, Chairman of Pacton Gold, in an interview with MINING.com. “With strong financial backers, our technical teams is currently reviewing additional accretive acquisitions in the area.”

“The Arrow Minerals project is directly adjacent to Novo Resources, a much larger land package, and highly prospective with nuggets from 5 to 10 millimetres in size on the property”

The second transaction took place just two days after the deal with CTTR was approved by the stock exchange. Pacton Gold signed a letter of intent (LOI) with Arrow Minerals through which Pacton could earn an 18% stake in its 609 km2 Pilbara Gold Project.

“The Arrow Minerals project is directly adjacent to Novo Resources, a much larger land package, and highly prospective with nuggets from 5 to 10 millimetres in size on the property, and multiple priority targets on the property,” according to Verdejo. “Here the earn-in agreement specifies making a cash payment of C$500,000 plus $250,000 in stock, for a 51% stake. That would be followed by issuing another 250,000 shares, and a work commitment of $500,000 to earn an 80% stake.

The third acquisition mentioned at the top of the story catapulted Pacton into position as the third largest landholder in the Pilbara gold rush. The acquisition of 1,126 km2 of licenses kicked the stock up 30% and put Pacton on the radar screens of investors who up to this point were largely unaware of the company.

Of significance once again is the properties’ proximity to Kairos and Novo tenements, but the area has also seen some historic exploration of Fortescue Group conglomerate – at least 90 kilometres close to surface with the discovery of two conglomerate zones. The zones are said to have mineralization similar to the Witwatersrand, the specialty of Dr. Mike Jones of Impact Minerals, from which Pacton purchased the properties through Impact subsidiary Drummond East.

The deal with Impact includes a C$350,000 cash payment and 2.125 million shares of Pacton. If Pacton is successful in outlining a resource over 250,000 ounces, Impact will require an additional half a million plus a 2% net smelter royalty.

“The Impact properties are very prospective with the work that Impact has completed, led by Dr. Mike Jones, CEO of Impact, who completed his PhD on the Wits. Dr. Jones knows the conglomerate-hosted gold model well, and with their support, we can continue to grow and at the same time watch closely the techniques used by Novo Resources,” said Verdejo.

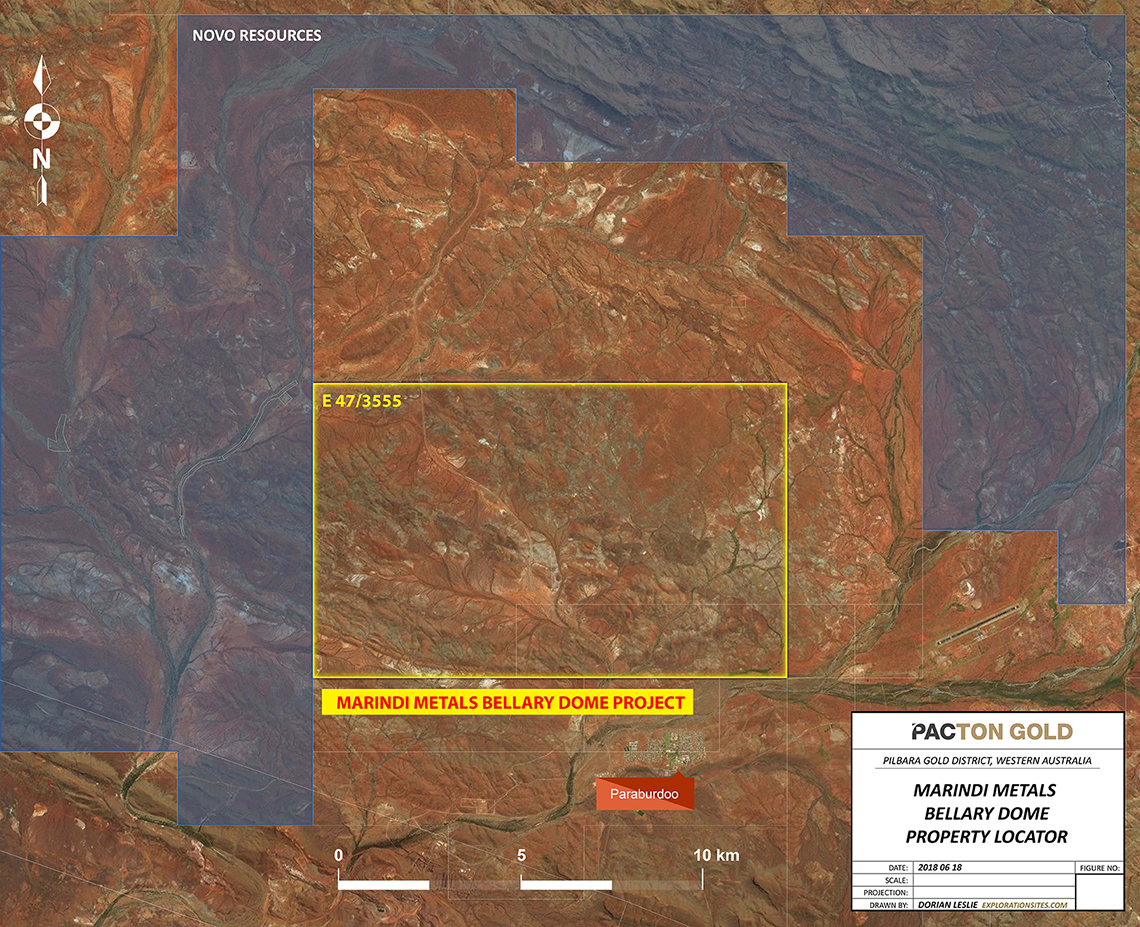

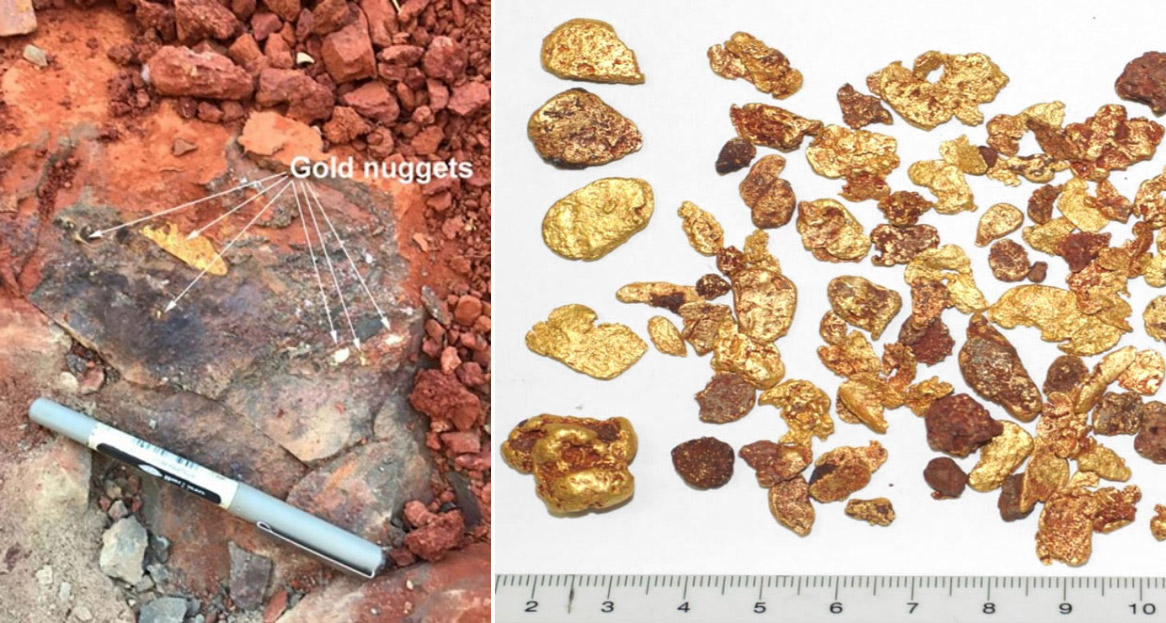

Lastly, the letter of intent (LOI) with Marindi Metals announced on June 20 gives Pacton Gold the opportunity to acquire the Bellary Dome Project. Located on the southern edge of the Hamersley Basin, Bellary Dome hosts about a 25-kilometre-long strike. Underlying the property is the Bellary Formation, which is believed to contain conglomerate gold that is similar to the watermelon-shaped nuggets found by Novo Resources at Comet Well and Purdy’s Reward. Over six ounces of coarse nuggets, described as “pitted, flattened and elongate watermelon seeds,” have been recovered downslope from the Bellary Formation. Novo owns claims surrounding the project.

Under the terms of the LOI, to acquire Bellary Dome, Pacton Gold must pay Marindi Metals C$2 million and issue 10,098,000 common shares upon the closing of the transaction. This would be followed up with a $1 million payment, or the issuance of the equivalent amount in shares, 12 months and 18 months later.

The game plan

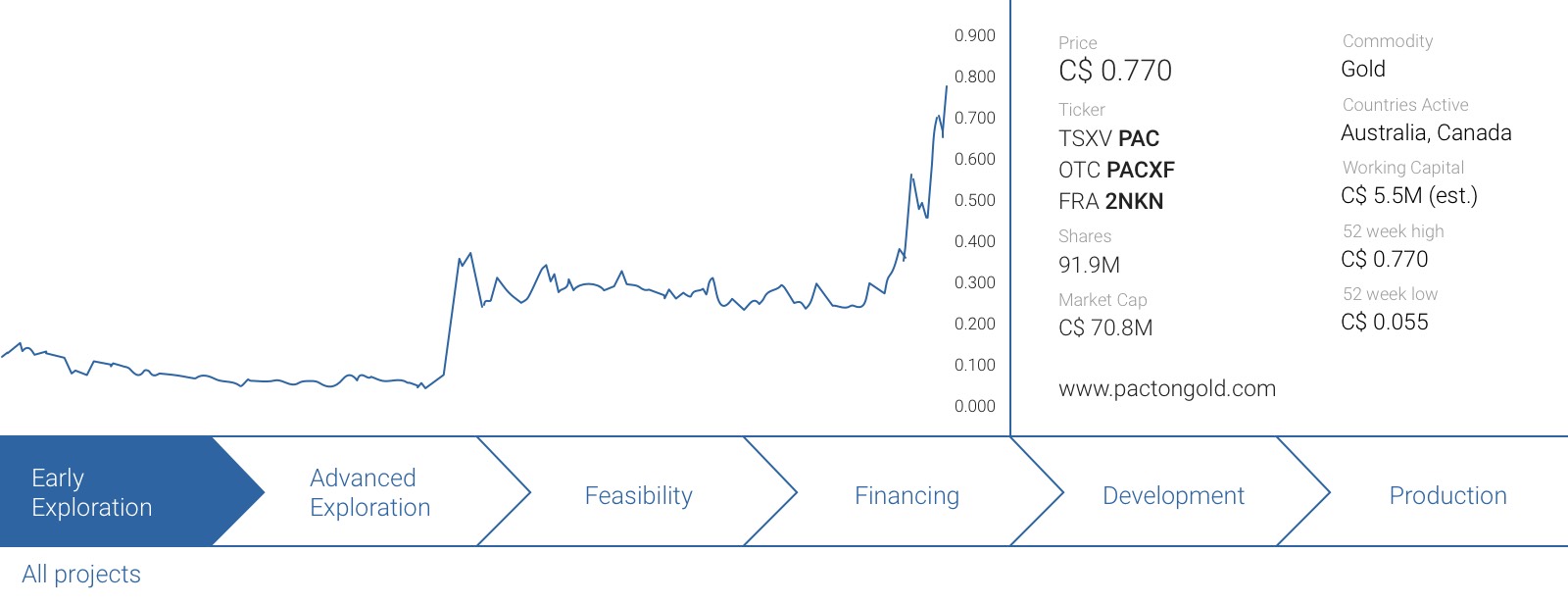

Pacton Gold is fully cashed up having recently completed a $5.5 million private placement, with Eric Sprott taking a sizeable position (up to +18%) in the Company.

Regarding the upside on Pacton and other juniors in the Pilbara, much is dependent on what happens with Novo Resources, the first mover. Novo continues to test various sample sizes, such as 5-tonne bulk samples, which would give a better indication of a potential mineable head grade. Conglomerate deposits are unconventional in that they cannot be bulk-mined in the same way as conventional open pits that are common in Canada and the rest of Australia. But Novo thinks mechanical ore sorting may be the way to mine them, having conducted a recovery test where 80% of the gold was recovered in just 2% of the total mass.

In the meantime, Pacton will continue to pursue land acquisitions. Says Verdejo:

“As a strong believer in the conglomerate-hosted gold Pilbara model, we will continue to be aggressive to add strategic land positions to our portfolio. Obviously as this area continues to gain global interest, Pacton needs to maintain its significant position within the region.”

Verdejo also noted that with most of the Pilbara explorers trading on the Australian stock exchange, Pacton, one of the few listed on the TSX Venture, offers North American investors an opportunity to participate in on the Pilbara gold rush. Pacton, with its large strategic portfolio, provides the potential for significant upside and a much lower entry price than, say, Novo Resources which closed at $4.80 a share on June 1st versus Pacton’s $0.42 a share close on the same date.

“Pacton controls an approximate land position 18% the size of Novo, but trades around 4.5% in valuation, thus providing a valuation re-rate as we continue to advance our projects,” said Verdejo.

Chasing nuggets in Australia next to Novo Resources

Western Australia has been getting quite a bit of attention in the past 18 months as a company called Novo Resources (NVO.V) claimed the region could host a new ‘Witwatersrand gold basin’ as the sedimentary and volcanic rocks appear to be the same age as the Witwatersrand reefs in South Africa. All you need is a hype and a strong desire to make a discovery, and Novo’s market capitalization increased from less than C$100M to in excess of a Billion.

Some people are still comparing the opportunity to invest in Novo to ‘buying bitcoin at 12 dollars’, but rather than ‘betting’ on an already mature company where the C$1B market cap skews the risk/reward ratio, it could make sense to look further down the chain for promising exploration companies targeting the same structures.

A number of junior exploration companies seem to be attempting to gain control of key land close to Novo, and be valued on the land position they acquire. If the geological and technical model created and being explored currently by Novo is correct, other companies in the area could be rerated based on proximity to and claim sizes to Novo. As we have seen, the “Pilbara Gold Rush Fever” has attracted many juniors but one seems to be have been particularly busy in the past few weeks.

Entering the scene: Pacton Gold (PAC.V), the reincarnation of what was previously called Noka Resources Inc. The roll-out of the newly named Company started slowly but with a big kicker, naming Mr. Alec Pismiris as Interim President & CEO. Granted, he definitely is not a household name in Canada, where Pacton’s corporate headquarters are, but “Down Under”, Pismiris is a name that is highly recognized in the mining sector as several companies he was involved with made large multi-million ounce gold discoveries. Despite announcing an Australian Big Shot as President & CEO, Pacton became quiet after this November 2017 appointment.

We spoke to the Pacton Team and it appeared they started on the acquisition trail, as they believed the opportunity in the Pilbara was still there as Novo’s exploration results could allure more companies to the region. In February 2018, Pacton started to put its land package together, Sprott Capital Partners became advisors and the company recently completed an oversubscribed financing where after gold bug Eric Sprott ended up with an 18% stake on a fully diluted basis.

Thanks to this financial backing, Pacton Gold is now well-financed to start its exploration program in Australia.

Why the Pilbara region?

The Pilbara gold rush started in 2016, when a new gold discovery was made around Karratha, a town in Western Australia. Geologists came to the conclusion the gold appeared to be coming from the conglomerates underlying parts of WA, and soon a new claim-staking rush was on its way. Novo Resources, led by respected geologist Dr. Quinton Hennigh, was probably one of the first companies figuring out the geological setting, and it provided a nice graphical overview of its theory in their corporate presentation:

And what exploration companies really are looking for are the zones where the older Pilbara greenstone rocks are in direct contact with the Fortescue Group rocks. Those are the ‘hot spots’ where gold nuggets generally occur.

Expanding the Western Australia Pilbara land position

Pacton Gold has been building its strategic land position in Western Australia in three different stages through three different acquisitions.

Transaction 1: The CTTR tenements

As a first baby step, Pacton acquired applications to a 492 square kilometer land package from CTTR Gold. CTTR was a newly-formed company with the purpose of putting a land package together in Western Australia’s Pilbara region. The acquisition consists of nine land claims, which were directly adjacent and proximal to the main properties controlled by De Grey Mining, Novo Resources and Kairos Minerals.

One of the first things Pacton would like to do on these tenements is to figure out if there’s a northern extension of the Mallina Basin gold occurrence, where DeGrey Mining discovered a nugget-bearing conglomerate zone with a thickness of 5-80 meters.

The acquisition was relatively cheap: Pacton will pay an initial C$100,000 in cash and will issue 916,666 shares (and half that number in warrants exercisable at C$0.45 for a period of 18 months). When at least six of the applications have been converted into exploration licenses, Pacton will pay an additional C$50,000, and issue an additional 416,666 shares (and 208,333 warrants, exercise price to be determined, as it will be 150% of the 5-day VWAP of the Pacton stock before the warrants are being issued). It was a first good step, but although this highlighted a new company was entering the Pilbara region, the market didn’t really care – perhaps also because ‘big brother’ Novo Resources was relatively quiet as well.

The Pilbara region has long been the world’s most prolific iron ore production district. Now, gold in Archean age conglomerates is the main exploration focus, heralded by Novo Resources dramatic new discoveries.

Transaction 2

Again under the radar, Pacton completed a second deal, which was announced just two days after receiving exchange approval for the first acquisition. Pacton Gold entered into a Letter of Intent with Arrow Minerals (ASX:AMD), whereby Pacton could earn an 80% stake in a Pilbara property with a total surface area of 609 square kilometers.

This is an even more attractive acquisition than the first transaction, as actual gold nuggets have been found on this property. Sampling outcropping conglomerates yielded several nuggets with sizes ranging from 0.5-1 centimeter. Needless to say this area is very prospective as well: not only is it directly adjacent to the Pilbara properties of the three other key players (Novo Resources, DeGrey Mining, Kairos Minerals), there’s zero doubt there actually is gold on the property. Not only did Arrow Minerals find gold nuggets, the entire land claim shows evidence of prospector activity.

Pacton could earn an initial 51% stake in the Arrow tenements by making a cash payment of C$500,000 and issuing C$250,000 worth of stock, followed by an additional C$250,000 in stock and the commitment to spend C$0.5M on exploration to earn the 80% stake.

Once Pacton has reached that 80% threshold, it will have to carry Arrow Minerals through the first C$5M in exploration expenditures made on the property. Note, Arrow Minerals retains all mineral rights on lithium, cesium and tantalum that could be mined from the property. But that’s fine, as Pacton is only interested in the gold anyway.

Now Pacton controlled in excess of 1,100 square kilometers in the Pilbara region, and the market still didn’t care about it too much. Until…

![]()

Strategic Financing

Despite a subdued market reaction on the land acquisitions, Pacton seemed to have gained the interest of the investment community, including Eric Sprott. The company quickly closed an oversubcribed strategic financing, rejecting several potential participants in the process to protect the share structure. Now the treasury has been topped up, Pacton could start to look at other accretive acquisitions to become an even larger player in the Pilbara. PAC didn’t waste any time and almost immediately announced a third acquisition in the Pilbara region.

Transaction 3

The third acquisition catapulted Pacton to the status of having the third largest land position in the Pilbara region. And the market really liked this deal as Pacton’s share price increased by 30% on the day of the announcement.

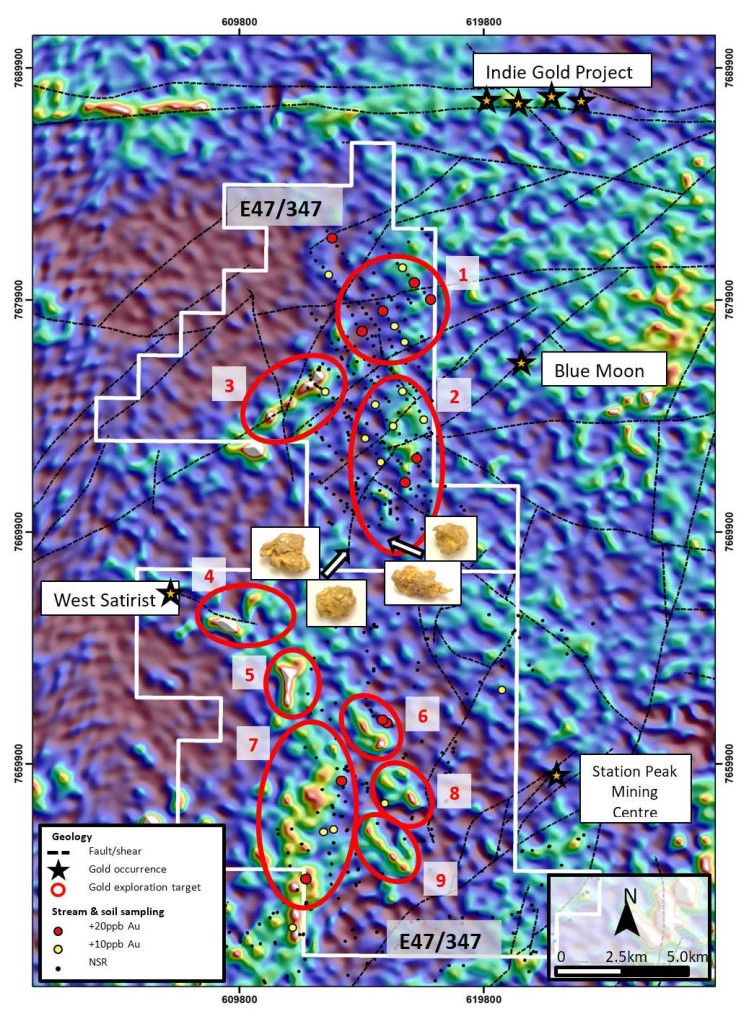

Arrow project: Radiometric map (U2/Th) with surface geochemical anomalies and gold targets

Pacton will acquire 1,126 square kilometers of licenses (which brings its total Pilbara land package to 2,227 square kilometers) from Impact Minerals (ASX:IPT). And once again, Pacton carefully selected the properties as these additional licenses are also adjacent to some of the Kairos and Novo tenements.

This also appears to be the property with the liveliest exploration history: the existence of at least 90 kilometers of Fortescue Group conglomerate close to surface or even at surface has already been confirmed whilst two conglomerates have already been discovered. These two conglomerate zones are pretty similar to the Witwatersrand type of mineralization, which is the specialty of Dr. Mike Jones, Impact Minerals’ CEO and leading geologist with decades of experience with Witwatersrand types.

At the Glen Herring prospect, a sampling program – conducted 30 years ago – discovered gold grades of up to 11.2 g/t from a conglomerate with a strike length of approximately 10 kilometers, whilst one drill hole at the Shady Camp Well prospect discovered anomalous gold values at a depth of 174 meters. 0.9 meters at 0.6 g/t isn’t exciting at all, but keep in mind these conglomerate-hosted zones can’t really be explored by conventional methods. It’s not unlikely the sniff of gold (0.6 g/t) is related to the existence of a ‘halo’ around the nugget-rich zones, and one drill hole clearly isn’t sufficient to form a decent opinion on this prospect.

The strike length of these conglomerates are already very decent, but apparently they just continue outside of the Impact Minerals license as Novo Resources sampled 15.9 g/t gold at its Contact Creek zone, which is located directly west of one of the licenses that are being acquired from Impact Minerals.

And once again, Pacton seems to have negotiated a very fair deal. The initial payment for the properties is just C$350,000 in cash and 2.125 million shares of Pacton. However, Impact Minerals also required a ‘bonus’ just in case Pacton is indeed successful in outlining a resource. Should Pacton have in excess of a quarter of a million ounces of gold in any resource category, an additional C$500,000 payment will be due, whilst Impact will also walk home with a 2% NSR. A small price to pay, should Pacton indeed be able to report a mineable resource.

And just to summarize: this is a schematic overview of the earn-in terms of all three acquisitions:

The exploration plans for 2018

Pacton Gold is now fully cashed up (see later) and will hit the ground running in 2018. On the CTTR tenements – which were acquired first), Pacton will start doing the basic things (as soon as the exploration licenses have been granted), and a substantial sampling program (consisting of rock chip sampling, soil sampling and stream sediment sampling) could hopefully point Pacton Gold in the direction of discovering a ‘nuggety’ conglomerate zone.

Having the ‘second mover advantage’ in the Pilbara region

As the gold in the Pilbara region is predominantly found in conglomerates, there was a lot of education to be done. Novo’s main issue in the past few years was how to explain to investors that any potential mining operation would be relatively unconventional (compared to Canadian and Australian standards). Exactly due to the ‘nuggety’ occurrence of the gold (gold in the Pilbara region occurs as primary nuggets, surrounded by gold haloes), it will be virtually impossible to compile a resource estimate to today’s standards.

Very few independent consultants will be willing to sign off on resources on extremely nugget deposits as the grade variations mean that mining Pilbara tenements will be a real case of ‘the proof is in the pudding’. A ‘mine as you go’ strategy will very likely be the only one that works, that’s why Novo deemed its 300-kilogram sample size to be insufficient in size. But 5 tonnes might give a much better representation of the expected average head grade. Production numbers and cash flows will be erratic, and that’s something the market had some difficulties to wrap its head around.

Another example: Novo has already conducted a recovery test, which determined mechanical ore sorting very likely will be the most efficient way to mine these types of deposits. In excess of 80% of the gold was recovered in just 2% of the total mass, providing a higher grade feed for further processing. A small detail, but it definitely will make Pacton’s life easier as it can piggyback on the preliminary findings of big brother Novo Resources (which is also being backed by Eric Sprott).

And that’s why we think being the ‘second mover’ could actually be positive for Pacton Gold. The first mover (Novo Resources) has done the tough job of preparing and educating the market for these type of deposits, and the ‘mine as you go’ concept will slowly sink in with the investor community. Pacton Gold is still years away from production, and probably won’t have to jump through the same hoops and deal with the same issues like Novo had to do.

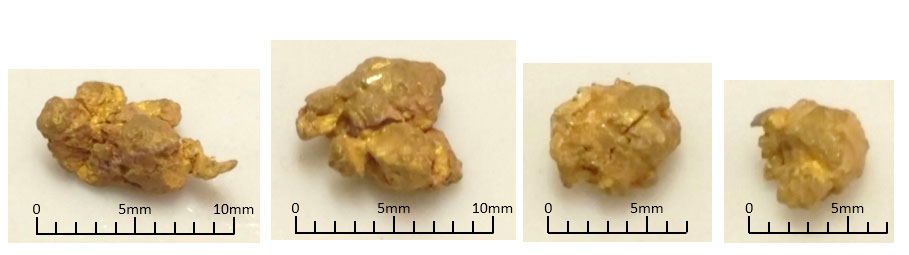

Pilbara gold nuggets

Pacton is now fully cashed up after raising C$5.5M

The Pilbara region remains very hot, and this was evidenced by Pacton Gold’s most recent capital raise. Right after announcing a deal to acquire a second set of gold properties in the Pilbara region, Pacton Gold announced a C$4M placement but immediately had to increase the size to C$5.5M due to a very strong demand.

The placement priced at C$0.23 per unit, with each unit consisting of one share and a full warrant, valid for three years, with an exercise price of C$0.35 per share. A placement ‘priced to sell’, indeed, and it attracted some heavy hitters. After closing the C$5.5M raise, Pacton Gold announced Eric Sprott purchased 8.7 million units after writing a cheque for C$2M. This results in Sprott owning just over 10% of the company’s share count, potentially increasing to just over 18% when Sprott exercises his warrants (which are already way in the money).

Hardly a surprise as Eric Sprott has been one of the most vocal backers of Novo Resources and remains a big believer in the Pilbara gold systems.

After this financing round, Pacton Gold’s share count increased to 87.9 million shares (which still is very reasonable), and the cheap full warrant also has an additional consequence. It’s not unlikely some of the warrant holders will start exercising their warrants after the initial 4-month hold period is over. And whilst we aren’t expecting a wave of sellers (the liquidity is really good, and with a weekly volume of 4-5 million shares it looks like the market should be able to absorb anything that’s being fed into it), a constant stream of warrant exercises could keep the treasury relatively filled. Should all warrants be exercised, an additional C$8.5M will hit the bank account.

A strong and experienced management team

The owners of Pacton Gold did a thorough job in converting the company from what basically was a shell to a gold exploration company. A first step was made in November last year, when the company announced Alec Pismiris as its new CEO and interim president.

Whilst a CEO announcement doesn’t usually indicate much, it was interesting to see where Pismiris was coming from. Although he didn’t occupy executive roles, he was involved with numerous successful gold exploration (and development) companies in the recent past. Pismiris was a founding shareholder of Papillon Resources (sold to B2Gold, which has started production on the Fekola gold asset in Mali) and Cardinal Resources (which will publish an updated PEA on its multi-million-ounce open pit project in Ghana in the next few weeks).

Pacton is also looking to add more experts to the management and board to assist with the ongoing development of its activities in the Pilbara.

The company recently announced Mr. Alf. Stewart joining the Board, who is currently President of BlueBird Battery Metals Inc. (BATT.V), focused on the Cobalt-Nickel-Copper battery metals. Stewart, a geologist, brings over 40 years in the technical and capital markets and actually helped finance a number of ‘Australian’ deals in his days as a broker with Canaccord and Haywood.

Management indicated they just came back from a 10-day tour of projects in Australia and are hoping to make other acquisitions when the timing is right. And considering Pacton’s recent acquisition had a positive impact on the share price and trading volumes, it looks like the market is finally waking up.

Conclusion

Gold nugget in a fossil transgressive lag gravel (Novo Resources image)

We don’t like to surf on the waves created by hypes, but Pacton Gold has been able to put a large land position together in just a few months. Of course, Pacton is and should be seen as an early stage exploration company but with proven gold (nugget) occurrences on several of the tenements it purchased/is earning in to. It is clear that there’s a lot of smoke in the Pilbara region and now it’s up to Pacton Gold to find the source of that smoke.

We think having Novo Resources as first mover could be beneficial to Pacton Gold, as Novo will do all the heavy lifting in terms of A) educating the market and B) designing the exploration programs as efficient as possible. We know the conventional exploration and processing techniques very likely won’t work on a nuggety type of deposit.

But one thing is pretty clear. With Novo Resources trading at a market cap of C$1B, Pacton Gold’s current market capitalization of approximately C$70M seems to be offering a more enticing risk/reward ratio.

For enquiries, please post a comment on the article online, contact us at caesarsreport.com/contact or email us at [email protected]

About Caesars Report

Caesars Report is an online mining portal specialized in (junior) mining companies. In the coming years securing resources will be fundamental to sustaining growth so this will remain a key area of investor interest. We provide coverage of companies that offer an attractive risk/reward ratio. Our aim is to inform our readers and to give them an incentive to do further research. We visit interesting companies ourselves and report from the source.

We are also present on numerous events all over the world, ranging from the PDAC International Convention in Toronto to smaller roadshows all over Europe. As we are not a registered investment advisor, please always do your own research.

Visit us at www.caesarsreport.com

Terms and Conditions

Please read our full terms and conditions at caesarsreport.com/discl

The CaesarsReport.com employees are not Registered as an Investment Advisor in any jurisdiction whatsoever. CaesarsReport.com employees are not analysts and in no way making any projections or target prices. Neither the information presented nor any statementor expression of opinion, or any other matter herein, directly or indirectly constitutes a representation by the publisher nor a solicitation of the purchase or sale of any securities. The information contained herein is based on sources which we believe to be reliable but is not guaranteed by us as being accurate and does not purport to be a complete statement or summary of the available data. The owner, publisher, editor and their associates are not responsible for errors and omissions. They may from time to time have a position in the securities mentioned herein and may increase or decrease. Pacton Gold is a sponsor of the website.

All images in this document are copyrighted by the concerning companies. The company data was fetched from the according stock exchange of the company or company presentations. Still, the owner, publisher, editor and their associates are not responsible for errors and omissions concerning this data. The Caesars Report logo, and the whole

of this document is copyrighted by caesarsreport.com.

This document is distributed free of charge, and may in no circumstances be sold, reproduced, retransmitted or

distributed, without written consent from caesarsreport.com.