China’s nuclear war on coal

After 13 years of rapid growth, China burns more coal than the rest of the world combined. The country was responsible for more than 80% of global growth in coal usage since the start of the century.

Even these numbers were upped in a recent study by the US Energy Information Administration (EIA) that showed energy-content-based coal consumption from 2000 to 2013 was up to 14% higher than previously reported at nearly 4.5 billion tonnes, while coal production was up to 7% higher.

But the growth stopped abruptly and started to reverse in 2014 when energy-content-based coal consumption remained flat and production declined by 2.6%. The downtrend is even more noticeable with Chinese imports which last year tanked by 30% to 204 million tonnes and has continued to shrink in 2016.

China added 138GW of new power generation capacity in 2015 – more than half of this came from increases in nuclear, hydro and renewables

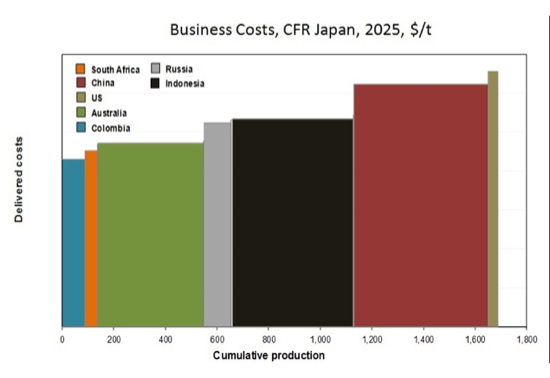

Given the slump in domestic demand, a new report by metals and mining research company CRU examines the likelihood of China becoming a net exporter of coal. The London-based firm concludes it’s unlikely to happen over the next five years – not least because China’s coal miners are not cost competitive on the seaborne market (see graph).

Source: CRU

But it’s the changes in the power generation industry in China and the speed at which the country is moving away from coal detailed in the research, that’s really startling.

China’s ambitions under COP21 is nothing if not ambitious. The country has pledged to source 20% of its energy from low-carbon sources and cut emissions per unit of GDP by 60% of 2005 levels by 2030.

CRU expects China “achieving the vast majority of its targets for thermal substitution”. China added 138GW of new power generation capacity in 2015, an increase of 10% compared to 2014 – more than half of this reflected increases in nuclear, hydro and renewable power according to the report:

“This shift is only going to be accelerated, following the pause to approvals of thermal plants in areas with an excess of capacity. And when we look at this in more detail, we find the impact of that substitution on coal market share in the South East is extreme – it falls from 64% to 49% over the next 4 years.”

According to the UN’s annual environment report China invested a total of $103 billion or 36% of the world total on renewable energy last year. The country also has 26 nuclear reactors currently under construction, another 40 in the planning stage and more than 100 being proposed which would require a five-fold increase in the country’s uranium requirements.

CRU says while 2015 saw expansion in power consumption from the residential sector of 6%, overall growth was dragged down by a 3% year-on-year decline in in heavy industries.

Chinese power demand is dominated by a few industries such as steel, non-ferrous smelting and chemicals, which account for 2.5 times as much as the entire residential sectors

That decline has implications beyond coal and coal mining because as CRU points out “the unusual aspect of Chinese power demand is the extent to which it is dominated by a few industries such as steel, non-ferrous smelting and chemicals, which account for 2.5 times as much as the entire residential sector”:

“Lower enthusiasm for new investment in housing inventory has considerably reduced demand for steel products and cement and we expect this sector to remain flat at best in the coming years.”

Falling demand is being reflected on the supply which has been contracting sharply this year – lower quality supply from Inner Mongolia has dropped nearly 20% so far this year according to the authors:

“Furthermore, large companies are enacting the Government-mandated cut to a 5-day working week, which has cut annual working days from 330 to 276.

“Longer term, the state council guidelines target a reduction of 500 Mt of coal capacity and consolidation another 500 Mt into the hands of fewer, more efficient operators in the next 3-5 years.”

Click here for CRU’s outlook for the seaborne coal market published last Friday.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments

Wally

Oil consumption will shortly follow suit.